February letter from Stanphyl Capital. The hedge fund was profiled in our second edition and returned 31% in 2016. Check out the post and especially the end of the PDF for more on their small cap stocks.

For February 2017 the fund was up approximately 3.9% net of all fees and expenses. By way of comparison, the S&P 500 was up approximately 4.0% while the Russell 2000 was up approximately 1.9%. Year to date the fund is down approximately 0.1% net while the S&P 500 is up approximately 5.9% and the Russell 2000 is up approximately 2.3%. Since inception on June 1, 2011 the fund is up approximately 127.8% net while the S&P 500 is up approximately 98.8% and the Russell 2000 is up approximately 77.2%. (The S&P and Russell performances are based on their “Total Returns” indices which include reinvested dividends.) As always, investors will receive the fund’s exact performance figures from its outside administrator within a week or two.

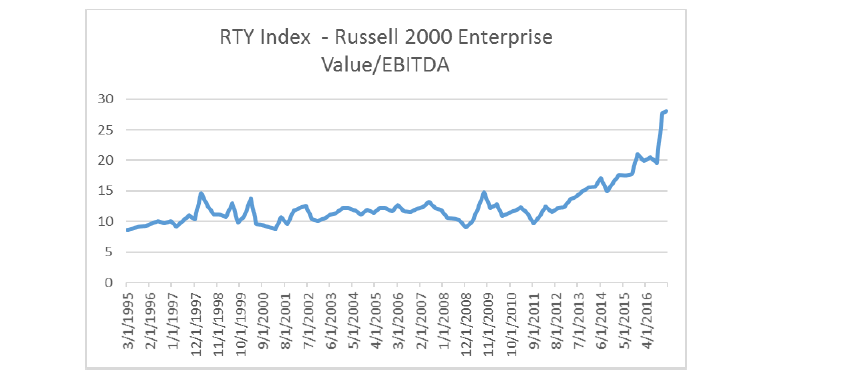

We continue to hold a large short position in the Russell 2000 (via the IWM ETF). I think this is a good hedge for our microcap long positions in what I perceive to be a dangerously expensive market, and as the companies in the index collectively have no earnings a potential Trump corporate tax cut can’t help them, while valuation (as measured by EV to EBITDA) is far above historical norms:

stanphyl capital

(Keep in mind that the last spike in that chart comes from Bloomberg [the source] using only partial numbers from Q4 2016, and thus the correct multiple is probably “only” around 22x… which is still almost double the long-term historical mean!)

We continue to hold a large short position in the Vanguard Total International Bond ETF (ticker: BNDX), comprised of dollar-hedged non-US investment grade debt (over 80% government) with a ridiculously low “SEC yield” of 0.75% at an average duration of 7.7 years. As I’ve written since putting on this position in July 2016, I believe this ETF is a great way to short what may be the biggest asset bubble in history, considering that Europe and Japan (which comprise most of its holdings) are printing approximately $144 billion a month (¥67 trillion + €80 billion, “tapering” to €60 billion in April), yet are long-term insolvent due to their retiree liabilities. What will force the bond buying to stop? For Europe I suspect it will either be intense political pressure from the north or inflation; either way, the end appears increasingly near. Japan I think can never stop printing (its ratio of debt to GDP is too huge and growing too quickly) but will eventually crash the yen into oblivion (we’ve been short yen since 2012) and with that its bonds will crash too. (I discuss Japan more extensively in the last paragraph of this letter.) The borrow cost for BNDX is just 2% a year (plus the yield) and as I see around 5% potential downside to this position (vs. our basis, plus the cost of carry) vs. at least 30% (unlevered) upside, I think it’s a terrific place to sit and wait for the inevitable denouement.

This content is exclusively for paying members of HiddenValueStocks

Exclusive Quarterly Newsletter with top emerging fund managers highlighting their favorite small cap stocks.

Jacob Wolinsky is the founder of HedgeFundAlpha (formerly ValueWalk Premium), a popular value investing and hedge fund focused intelligence service. Prior to founding the company, Jacob worked as an equity analyst focused on small caps. Jacob lives with his wife and five kids in Passaic NJ. - Email: jacob(at)hedgefundalpha.com

FD: I do not purchase any equities to avoid conflict of interest and any insider information. I only purchase broad-based ETFs and mutual funds.