Summary

The largest Slovenian bank, with dividend yield of 12.5% and RoE of 14% is trading just at 0.7 Price to Book ratio.

Q2 hedge fund letters, conference, scoops etc

New to the market and not fully known outside Central and Eastern Europe focused investors.

Since the IPO 6 months ago, the shares are up 25%.

The major drag on the share prices just disappeared.

Summary

Nova Ljubljanska Banka (NLB) is the largest financial Group in Slovenia with presence in 6 other Balkan countries with a market cap of 1.3 billion EUR and total assets of 13 billion EUR. The bank has an investment grade rating from both S&P and Moody's with a positive outlook. The shares are up 25% since the IPO in November 2018. With Total Capital Ratio of 17%, RoE above 14%, and a dividend yield of 12.5%, the bank still trades at 0.7 P/B vs. 1.2-1.6 P/B of regional peers with similar profitability. The drag has been the further disposal of an additional 10% stake by the Slovenian government, which took place right after the dividend record date of 17.6.2019. JPMorgan target price is 93 Euro, which represents a 55% upside.

Introduction

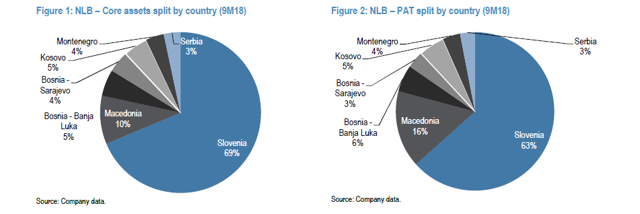

Nova Ljubljanska Banka is the largest international financial group in Slovenia, operating in the other six countries of formal Yugoslavia. Its geographical business can be summarized as follows:

Source: JPMorgan research on NLB

NLB operates with commercial banking licenses and offers retail and business banking services as well as ancillary financial services such as asset management and insurance. The loan book is broadly half-half retail versus corporate, whereas 75% of deposits are retail.

The group segments its business into its core operations of Slovenian Retail, Slovenian Corporate, Slovenian Financial Markets and Strategic Foreign Markets, and into a non-core unit. Corporate generated 22% of pre-tax profit in 9M18; Retail, 16%; Financial Markets, 12%; Foreign Strategic Markets, 46%; and the non-core activities, 5%.

History

NLB was established in 1994. The bank had been 100% state-owned since 2013 when the Slovenian government stepped in to recapitalize the bank in 260 million Euro bailout. The European Commission forced the Slovenian Government to sell 65% stake bank on state aid grounds. The IPO was placed in November 2018. The government committed to selling an additional 10% by the end of 2019. The Slovenian state wants to retain the remaining 25% as a long-term strategic holding.

Slovenian Economy

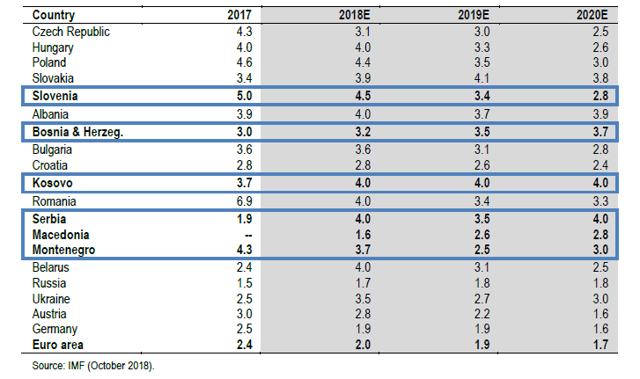

Banks are proxy for the economy in which they operate. The Slovenian economy is performing quite well. According to the IMF, Slovenia was one of the fastest growing economies in Europe. IMF predicts that the economy will remain one of the best performing economies. The table below indicates IMF growth rate forecasts for countries where NLB operates.

Source: JPM Research on NLB

Investment Grade Rating

In May 2019, rating agency Standard & Poor's raised NLB's credit rating by one notch to BBB- from BB+ (outlook stable), a move that takes it to the investment grade territory. Justifying the move, S&P said that industry risks in Slovenia's banking system have decreased because of the state's reduced ownership of banks, and stronger banking supervision. In addition, the agency pointed out that NLB's financial profile remained sound, and the key performance indicators in 2018 were largely in line with their expectations, while asset quality metrics improved faster than expected. That now means NLB is rated investment grade with a positive outlook by the major rating agencies Standard & Poor's and Moody's.

Dual Listing

The shares are now listed both in the local market on the Ljubljana Stock Exchange and as GDRs in London. The GDRs can be traded on Interactive Brokers (ticker NLB) as well as on other online platforms. Both markets are fully fungible – investors can convert from shares to GDRs and back at relatively minor costs.

New Bond Issues Reconfirm The Bank's Strength

NLB just announced that it had placed SID Bank bond issue of 200 million Euros. The maturity of the bond is seven years, the coupon interest rate 0.125 percent, and the yield to maturity 0.18 percent. This is the lowest premium so far over the comparable government bond and the lowest coupon interest rate for the longest maturity period of any bond issued by the SID Bank so far.

Reasons For The Opportunity

The IPO was launched in November 2018. Since then, the share has advanced by 25% (local shares were placed at 51.5 Euro and increased to 65 Euro on the ex-dividend date 6/14/2019 (current share price (after EURO 7.1 dividend) is 59.6 Euro). Despite that, the shares trade just at 0.7 P/B while its CEE peers trade between 1.2 and 1.6 P/B. We believe that the below reasons will drive the share price higher:

- Recovery of the initially depressed local market – While the GDR tranche was heavily oversubscribed, the local tranche had a little demand. The reason is simple – local investors still remember the state bailout of the bank. This is a typical phenomenon in countries with less developed capital markets. As the share price has been increasing, the local investors are warming up on the story.

- Profit from the state bailout - In our experience, state bank bailout offers a unique opportunity. The ideal example was the Czech Republic: the state provided a bailout to two leading banks (Komercni Banka and Ceska sporitelna) in the early '90s. Both banks, 20 years on, still have significant capital surpluses, and the shareholders that got in early after the bailouts were strongly rewarded.

- Resolution of the share overhang - After the IPO, the government retained a 35% stake. Under the agreement with the European Commission, they need to dispose of an additional 10% by the end of 2019. The potential share overhang has been a drag on faster share price growth. Institutional investors were waiting on the sidelines as they believe that they should be able to buy the shares at the SPO at 5-7% below market price. The SPO was executed on 6/19/2019 and will close on 6/21/2019. The SPO was significantly oversubscribed and the allocations were around 20% of subscribed shares. The major share overhang risk was therefore resolved, and the share price is up by 5% in the last four days. We believe this will continue.

- Increase in liquidity – at the current share price, the institutional investors are not willing to sell. That results in lower liquidity. Lower trading volumes discourages further buyers. As the price is increasing, liquidity is expected to increase as well.

- Share Buyback – the shareholder meeting on 10 June 2019 approved a share buyback. The shares will be distributed to employees as a part of their variable remuneration. The size of the buyback is approximately 2 million Euro. The buyback should support the share price and should further align the interests of the management with those of shareholders.

- Index inclusion - NLB is the second largest stock in Slovenia by market capitalization. NLB stock was added to the FTSE Frontier index as of 27 November 2018. Now, we believe that NLB may be a potential candidate to be added to the MSCI Slovenia and MSCI Frontier Markets indices.

Valuation

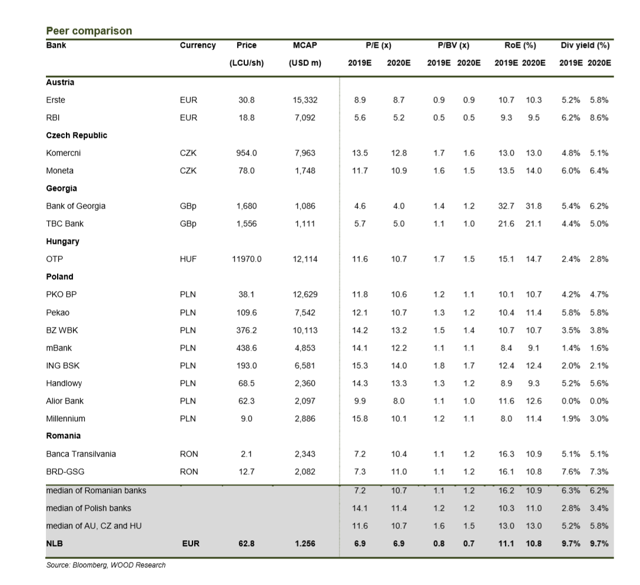

Despite the highest dividend yield in the region, the bank still trades significantly below its regional peers. The bank trades at 0.7 P/BV while its local peers trade at 1.2–1.6.

The below table from WOOD & Company research, a leading broker in the CEE region, provides peer valuation of NLB. Based on WOOD's assumed future profitability, the table illustrates that a bank with NLB's RoE should trade around 1.1-1.2 P/B multiple. Based on this and other supported valuation techniques, WOOD & Company calculated their price target of 80 Euro, 35% upside from the current price.

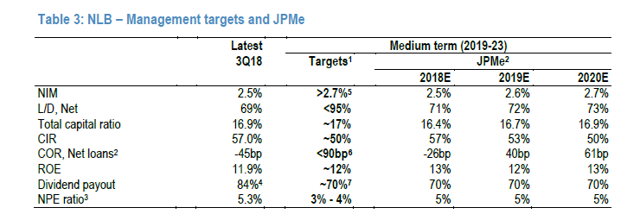

In the table above, WOOD & Company forecasts RoE of around 11%. JPMorgan, in their research, predicts that the RoE should be around 12-13% (see the table below). Under such a scenario, the applicable target P/BV ratio should increase above 1.3. Based on this and other valuation techniques, JPMorgan arrived at a price target of 93 Euro, 56% upside from current share price.

Source: JPMorgan

Both JPMorgan and WOOD & Company forecasts are well below the 14% RoE that NLB achieved in 2018 and 1Q19. If NLB would be able to sustain its RoE at this level, the bank should be trading at P/B ratio of 1.4-1.6. Based on this, the bank should trade around 118-134 Euro per share.

In summary, the target price based on P/B multiple can be calculated as follows (based on estimated 2Q2019 book value per share of 80 Euro and share price of 60 Euro):

| P/B ratio | Target price | Upside |

| 1,1 | 88 | 47% |

| 1,2 | 96 | 60% |

| 1,3 | 104 | 73% |

| 1,4 | 112 | 87% |

| 1,5 | 120 | 100% |

| 1,6 | 128 | 113% |

Based on the table above, my near-term target of 90 Euro per share seems to be quite an achievable target in the short term. That represents 50% upside.

The Catalyst

The near-term catalysts should be the sale of 10% by the government in the SPO that should complete the bank's privatization. As stated above, the SPO was placed on 6/19/2019 and was five times oversubscribed. That should resolve the share overhang risk and increase liquidity.

Conclusion

NLB is the cheapest prime bank in the CEE region while having one of the highest returns and dividend yield among its peers. The recent 7-year bond issue launched with a yield of 0.18% yield reconfirms the bank's strength is understood by bond investors. It is now up to equity investors to catch up to the story. In my experience, this should not take long.