Introduction

John Deere (DE) and Caterpillar (CAT) are both well-known companies that have been around for decades. John Deere was founded in 1837 while Caterpillar was founded in 1925, just two years shy of its 100-year in existence. These two companies have been through the Great Depression of the 1920s, the second world war, the Korean War, Vietnam War, the high inflationary period in the 1970s, the Gulf War, the dotcom bubble, the Great Financial Crisis, and more recently the Covid-19 pandemic. And the key takeaway is this: they both survived all these, and continue to thrive, and they are likely to continue to thrive in future.

Both companies have rewarded their long-time shareholders (more on this later) so these are definitely companies investors should have in their portfolio – purchased at the right price of course.

Q1 2023 hedge fund letters, conferences and more

FAST Graphs Analyze Out Loud Video on John Deere & Caterpillar

Introduction to John Deere: More Than A Tractor Company

At the CES 2023, John Deere CEO John May shared the following,

Today, John Deere leverages a vast tech to give our machines superhuman capabilities. This begin with our equipment. Over 500,000 connected machines run across more than a third of the earth’s land surface. You might want to think of them as robots that precisely execute jobs in the land, on roads, and at construction sites. Within these machines, we have integrated displays with embedded software, GPS hardware with precisely signal correction; machine learning, cloud computing and one of the leading digital platforms in the agricultural industry, the John Deere Operations Center. Each one of these technologies brings unique and specific benefits to our customers.

If anyone still thinks that John Deere (DE) is only about boring farm tractors and farm equipment, that excerpt from John May’s keynote speech at CES 2023 would sound totally unbelievable. It may be difficult to visualize this company that started in 1837 as a technology company today but that is how investors should view John Deere. It will not be too overboard to think of John Deere as an AI company. Its most recent acquisitions include SparkAI (“provides contextual cues that the autonomous tractor is sometimes missing in order to make confident decisions in real-time), Light (“which specializes in depth sensing and camera-based perception for autonomous vehicles“), Bear Flag Robotics (its “technology enables tractors to run autonomously, human supervisors use software to monitor and command the fleet from a remote mission control room or personal device“), and not to forget Blue River Technologies which was acquired as early as 2017 before the AI buzz and fad took off (its “See & Spray and Sense & Decide devices to analyze every plant in a field and apply herbicides only to weeds and overly crowded plants needing thinning“).

It is therefore no coincidence that after consecutive years of falling sales from 2013 to 2016 that Deere managed to improve sales again, with its 2022 sales almost doubling that of 2016.

Daniel Theobald, the founder and Chief Innovation Officer at Vecna, a provider of mobile robots, platforms, and remote presence devices, shared the following perspective about John Deere,

It’s a smart move by Deere. They realize the time window in which ag industry execs will continue to buy dumb equipment is rapidly coming to a close. The race to automate is on and traditional equipment manufacturers who don’t embrace automation will face extinction. Agriculture is ripe for the benefits that robotics has to offer. Automation allows farmers to decrease water use, reduce the use of pesticides and other methods that are no longer sustainable, and helps solve ever worsening labor shortages.

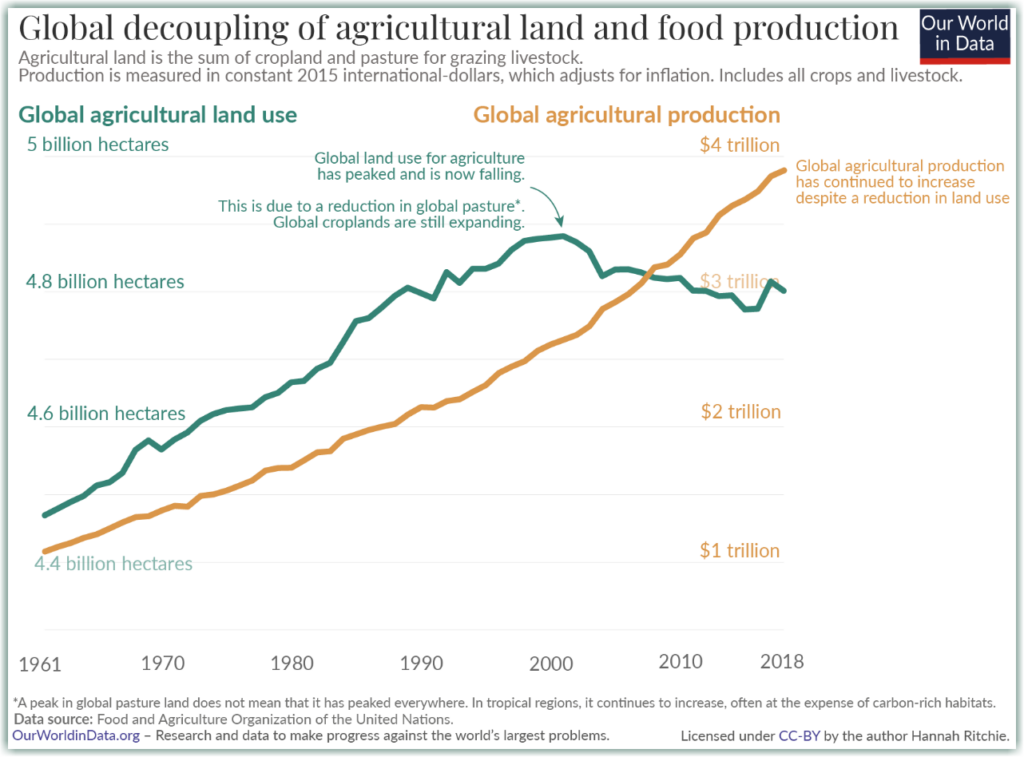

This is a strange world that we are living in. The United Nations predicts that the world’s population will increase from the current 8 billion to 9.7 billion in another 27 years. The increasing human population naturally results in an increase in demand for land for housing and of course for food. Yet, the amount of agricultural land for food production has been on the decline for the past twenty years.

John Deere’s CEO said as much in his CES 2023 speech,

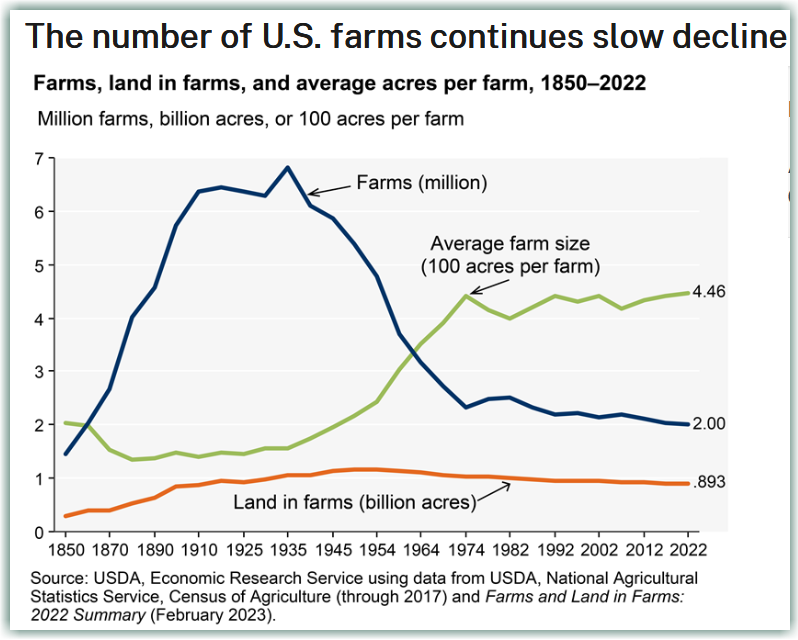

Over the next 25 years, the global population is expected to grow from 8 billion people to nearly 10 billion people. This requires us to produce 50% more food as both population grows and diets change around the world. But it is not just about growing more. The amount of US farmland has been declining over the past 40 years and this trend will likely continue as the population continues to increases. More people, less land, the math doesn’t work.

That is confirmed by the United States Department of Agriculture (USDA).

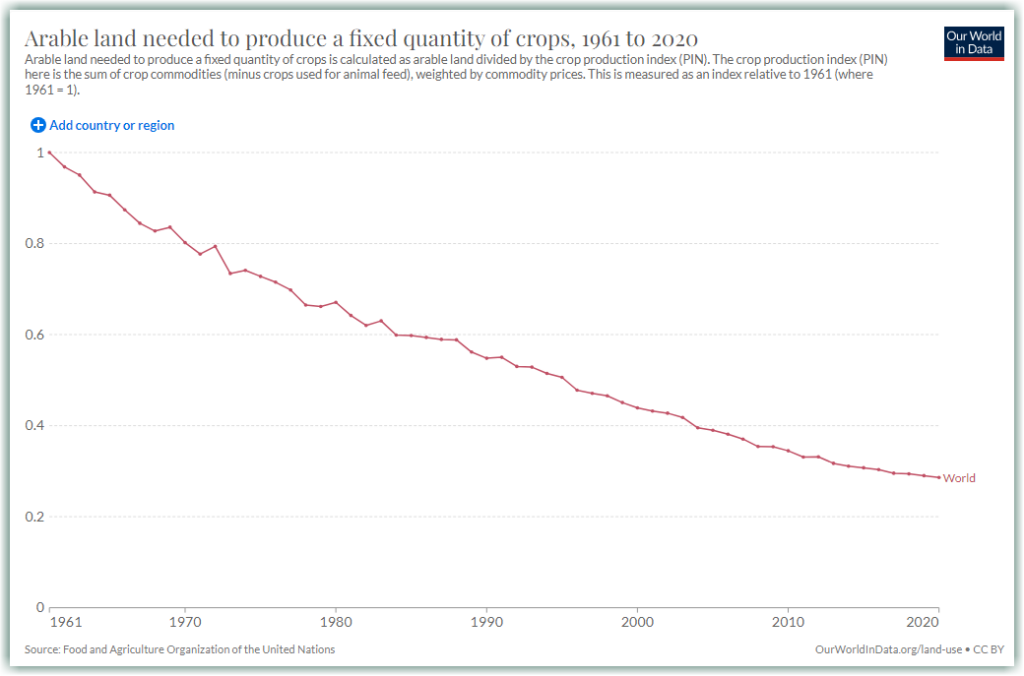

How is it possible, or tenable, to have more food produced on less land?

Thanks to the power of technology and technological advancement, be it farming techniques, more productive seeds that need less water, better fertilizers, and of course with technology-enabled machines and smarter use of cloud computing and analytics, more can be done with less – less land, less water, fewer farmers. In short, more food can be produced on less arable land.

These two tailwinds – the increasing demand for food and the increasing automation of equipment – will keep John Deere at the forefront for a long time. People can reduce spending on clothes, bags, watches, sports equipment, cars, boats, etc, but they have to keep eating.

What are the revenue segments?

John Deere does more than just sell farm-related equipment. They provide machinery for different industries beyond agriculture, into construction, forestry, military, and equipment rental.

According to the 2022 10K, John Deere has four business segments.

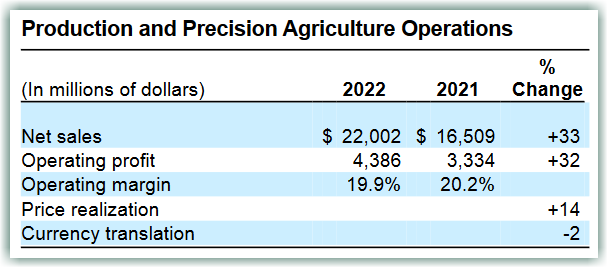

Segment One: Production and Precision Agriculture (PPA)

The segment’s main products include large and certain mid-size tractors, combines, cotton pickers, sugarcane harvesters and loaders, and soil preparation, seeding, application, and crop care equipment.

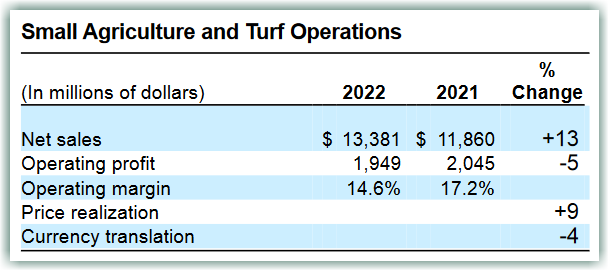

Segment Two: Small Agriculture and Turf segment (SAT)

The segment’s primary products include certain mid-size and small tractors, as well as hay and forage equipment, riding and commercial lawn equipment, golf course equipment, and utility vehicles.

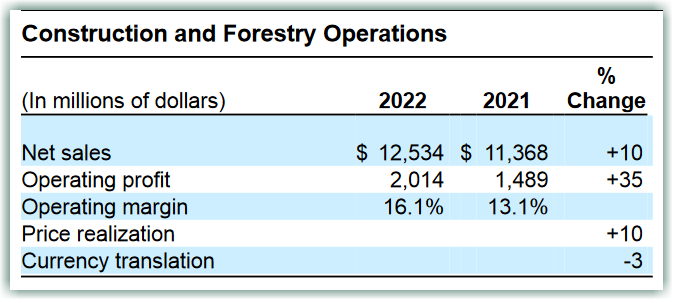

Segment Three: Construction and Forestry segment (CF)

The segment’s primary products include crawler dozers and loaders, four-wheel-drive loaders, excavators, skid-steer loaders, milling machines, and log harvesters.

Read the full article here by James Long, FastGraphs.