What an amazing three days. I’ve said to some of my clients that moves of this magnitude are highly unusual. How unusual?

Q4 2019 hedge fund letters, conferences and more

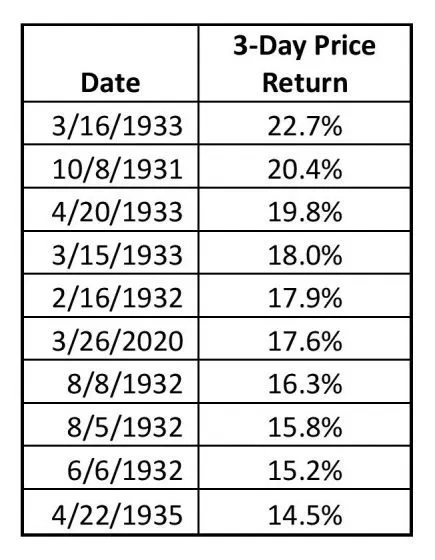

The returns of the last three days would rank sixth in the top ten three-day moves upward for the S&P 500 since 1928. When did the rest of the top ten take place? During the Great Depression — four in 1932, three in 1933, and one each in 1931 and 1935.

Given the overall difficulties of the stock market in the Great Depression, one could say that the 2020 stock market should find being peers with which to keep company.

One more note about March 26th, 2020, that sets it apart: It’s the only one of the dates that may be a bounce up from a bear market low. The fastest bear market may become the fastest bull market if the S&P 500 closes above 2685 soon.

Image Credit: Aleph Blog

It Doesn’t Get Much Worse Than This?

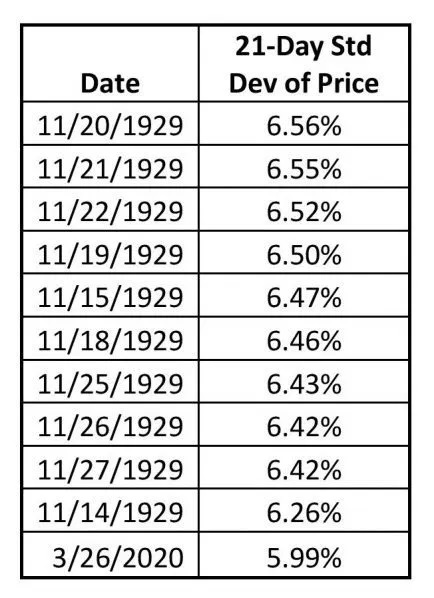

Image Credit: Aleph Blog

Consider monthly price volatility. Using 21 days to represent a month, the standard deviations of price movements for March 26th would be the eleventh highest. When did the other ten take place. One day after another for ten trading days starting on November 14th, and ending on the 27th of the same month.

Do you feel like the current market action has slugged you hard? I do. That would be a normal feeling, as we haven’t been through anything quite like this in our lifetimes.

Even if you look at implied volatility, for which we only have data since 1986 (if you are looking at the old VIX, 21-day average volatility would have ranked 54th. 39 trading days starting on October 27th, 2008, and 14 trading days starting on November 3rd, 1987 ranked higher. Still it been fascinating to not see the VIX move down much over the last three days. Perhaps there are a lot of investors still aggressively buying puts and calls.

Four Interesting Periods in the Stock Market

So think about:

- The Great Depression

- Black Monday and related problems in 1987

- The Great Financial Crisis in 2008, and

- Now

The two “Greats” had collapses in asset prices and corresponding impairments of banks, and some other financial institutions. They were for practical purposes universal panics.

1987 was shocking, but it came back fast, and it didn’t have much collateral damage. The current time period? Well, banks are lending to creditworthy borrowers, and March is a record for US dollar denominated investment grade corporate bonds, Jon Lonski reported at Moody’s in his report released tonight. There’s no lack of liquidity to the big guys with normal balance sheets.

For CLOs, MLPs, repos and Mortgage REITs, that’s different. They are highly dependent on capital market conditions to do well. They are “fair weather” vehicles. In this situation, the Fed is extending itself in ways that it doesn’t need to, and for areas that should be left alone. Nonbanks should not be an interest of the Fed. If you’re going to take all systematic risk away from business, they’re going to behave in even more aggressive ways, and create an even bigger crisis. This one would have been small enough for the private sector to handle, once the initial wave furor over COVID-19 dies away in a couple of weeks.

Same for the Treasury. We don’t need the stimulus, and recessions help to clear out bad allocations of capital. This is a waste of the declining creditworthiness of the US Treasury, which will find itself challenged by a bigger crisis in 10-15 years, with no flexibility to deal with it.

Two Final Notes

I have a series of four articles called, “Goes down double-speed.” The market going down rapidly is less unusual than it going up rapidly. Typically the speed of down moves is twice as fast as up moves. For the current up moves to be so fast is astounding. I would say that it shouldn’t persist, but I think the market will be higher because the first wave of COVID-19 will fade.

And so I go back to one of my sayings: “Weird begets weird.” Weird things happen in clumps, in bunches. Much of it is driven by bad monetary and fiscal policies, including policies the encourage people and institutions to take on too much debt. Unusual factors include COVID-19 and the policy response to it. Part of it is cultural — we take too much risk as a culture, which works fabulously in the bull phase of the cycle, and horribly in the bear phase.

And thus I would say… prepare for more weird. Like COVID-19, it’s contagious.

Article by David Merkel, The Aleph Blog