Prescience Point has discovered numerous additional red flags and believes shares of Enphase Energy remain grossly overvalued.

[timeless]

Q2 hedge fund letters, conference, scoops etc

Since the release of its initial report on Enphase, Prescience Point has identified numerous additional red flags which further call into question the reliability of the company’s financial statements. Prescience Point continues to believe that Enphase shares are currently worth about $1.00 on a fundamental basis.

- Following Q2 2018 earnings and other recent developments, Prescience Point continues to believe that Enphase Energy’s purported turnaround under its new CEO is a sham.

- Our analysis of ENPH’s Q2’18 results indicates a continued increase in the severity of accounting shenanigans that inflate financial performance.

- Management tried to explain away some of the red flags highlighted in our Initiation Report; however, management’s explanations in some cases conflict with statements previously made on the record and in other cases defy logic.

- Despite the use of aggressive and potentially improper accounting practices to inflate financial performance, ENPH still missed Q2 consensus estimates and whiffed on guidance. The 12.9% and 8.9% YoY decline in ENPH’s Q2’18 inverter volume and adjusted revenue, respectively, indicate that its business is deteriorating at a faster pace than we initially thought.

- According to sources, former SunEdison CEO Ahmad Chatila is currently working for ENPH. ENPH appears to have adopted many of the same practices which ultimately led to SUNE’s downfall.

- Prescience Point reiterates our estimate that Enphase stock is worth ~$1/share on a fundamental basis, implying 80% downside.

Prescience Point Reiterates Strong Sell Recommendation On Additional Red Flags Of Accounting Impropriety

On July 25, 2018, Prescience Point published a research paper (the “Initiation Report”) on Enphase Energy (“ENPH” or “the company”). In our Initiation Report, we concluded that ENPH's financial results since Q3 2017 have been materially inflated by manipulative, and potentially improper, accounting practices that have become increasingly severe with each passing quarter.

ENPH continues to hold our interest for the following reasons, each of which we thoroughly discuss in our Follow-Up Report:

- Our analysis of ENPH's Q2'18 results shows a continued increase in the severity of manipulative accounting practices to inflate financial performance

- Management tried to explain away some of the anomalies and discrepancies in ENPH's financial results we had pointed out in our Initiation Report. As we show, management's explanations in some cases conflict with statements previously made on the record and in other cases lack in credibility

- Despite the use of aggressive and potentially improper accounting practices to inflate financial performance, ENPH still missed Q2 consensus estimates and whiffed on guidance. The 12.9% and 8.9% YoY decline in ENPH’s Q2’18 inverter volume and adjusted revenue, respectively, indicate that its business is deteriorating at a faster pace than we initially thought

- According to sources, disgraced former SunEdison CEO Ahmad Chatila is currently working for ENPH. ENPH appears to have adopted many of the same questionable practices which ultimately led to SUNE's downfall

We hope that current and future investors and creditors familiarize themselves with the risks we have addressed and take immediate action to preserve the value of their holdings.

Prescience Point Reiterates Strong Sell On ENPH, Recent Developments Further Indicate That Its Reported Financials Cannot Be Relied Upon

In this report, we present seven additional red flags which have emerged since the release of our Initiation Report on July 25th

- Q2 Results Appear To Have Been Significantly Inflated Yet Again By Improper Deferred Revenue Accounting Practices

- ENPH Reported Another Anomalous YoY Increase In Revenue Per Inverter In Q2 2018, In Our View, Confirming That Revenue Was Significantly Inflated

- Management Has Provided Three Different Explanations For ENPH’s Anomalous Revenue Per Inverter Increase, None Of Which We Find Credible

- Q2 Revenue Was Further Inflated By A Questionable Milestone Payment, Which Was Suspiciously Booked At A 100% Gross Margin

- Management Could Not Credibly Explain The $6.3M Shortfall In Its Beginning Q1 2018 Deferred Revenue Balance; A Forensic Accounting Firm Agreed With Our Assessment

- According To Sources, Disgraced Former SunEdison CEO Ahmad Chatila Is Currently Working For ENPH

- Q2 Results Indicate That ENPH’s Business Is Deteriorating At A Faster Rate Than We Initially Thought

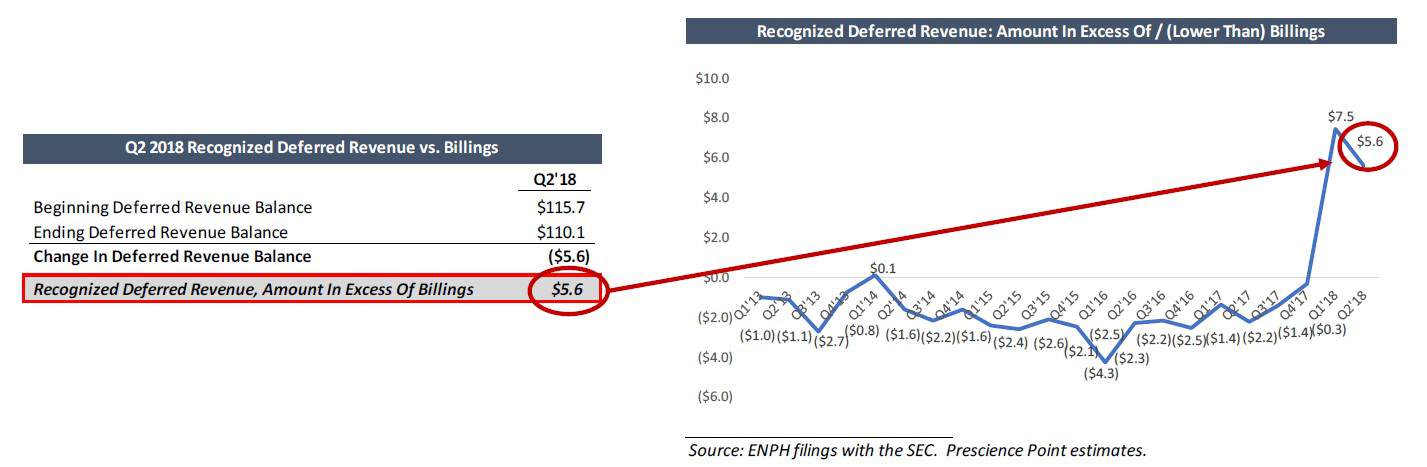

Red Flag #1: Q2 Results Appear To Have Been Significantly Inflated Yet Again By Improper Deferred Revenue Accounting Practices

- Our research indicates that ENPH’s Q2 2018 results, just as in Q1 2018, were significantly inflated by deferred revenue accou nting shenanigans

- Clear evidence of this can be seen in the large decline in its deferred revenue balance – In Q2 2018, the company’s deferred revenue balance declined by $5.6m, meaning that ENPH recognized $5.6m more deferred Envoy revenue than what it actually billed in the quarter

- As shown in the graph below, Q1 2018 and Q2 2018 are the only quarters over the past 5 ½ years in which recognized deferred r evenue has significantly exceeded billings. We do not believe this is a coincidence. Instead, we believe that the company’s seemingly improper deferred revenue accounting practices initiated in Q1 2018 continued in Q2 2018

Read the full article here by Prescience Point.