Don’t call it a comeback

I’ve been here for years

I’m rocking my peers

Puttin’ suckers in fear

Makin’ the tears rain down like a monsoon

Listen to the bass go boom

Explosions, overpowerin’

Over the competition I’m towerin’

LL Cool J, Mama Said Knock You Out, 1990

Q1 hedge fund letters, conference, scoops etc, Also read Lear Capital: Financial Products You Should Avoid?

After a little hiatus of 227 days, many of you have been asking when I’d be writing these Musings again. Well, I’m back, with a ton of charts and new views on the markets. Hopefully you’ll find them as interesting and useful as before. In case you don’t recall, I wrote last time that I was tired of writing the same things over and over, and needed to just sit and wait for markets to get more rational. Since then, markets went through an epic run up to nearly 2850 on the S&P 500 (SPX), only to fall 12% to touch exactly where it was the day I signed off (SPX 2550). The roundtrip was painful for those cautious on the way up, but very, very profitable on the way back down. For the first time in years, active traders and long-short managers are making money, as volatility has picked up and intra-market correlations have fallen. This is a great market for those with the flexibility to play both sides of the moves. We spent a good part of the hiatus refining our investment process, trying to get smarter in how we manage risk, size positions, and implement ideas. So far it’s paying off. Just don’t call it a comeback.

So what did we miss while we were out? Well, quite a lot actually. After the short-vol implosion (Finally! See ya later XIV) in February, the SPX has been chopping up and down from roughly 2550 to 2750. This is about an 8% range, which is nice for those who are nimble enough to trade it. The full decline of 12% from the highs to the recent lows was enough to take the air out of the SPX bubble a bit, but, as you’ll see from some charts below, margin debt is climbing and lots of folks remain all in on equities. While bonds have had their worst start to a year a long time, they are still expensive. But don’t forget, there is a third alternative, cash, and with 3-month T-bills and money market funds finally offering some yield, it’s not a bad place to hide these days. We’re leaning a little long, but have a portfolio of longs and shorts that are well positioned to produce some profits we think.

We’re cautious on equities and bonds longer term (some things don’t change), mainly due to stretched valuations, but shorter-term we think both are setting up for a rally. The difference in yields between U.S. treasuries and German Bunds is nearing all-time wide levels, but there is zero credit risk in the U.S. (recall, since we print our own money, we can’t default unless by choice), while there is credit risk in the Eurozone. With the Fed still raising rates, we think the yield curve in the U.S. will continue to flatten, with longer-term yields coming down while Fed Funds, LIBOR and T-bill yields continue to rise. Bank stocks are trading off the 10-year treasury yield these days, but with deposit pricing pressures continuing unabated, we think that further gains from here will be hard to come by. Instead, we’re looking at some really beaten down sectors to catch a bounce, with the group we hated the most for years, Consumer Staples (XLP), starting to look oversold for a trade. We also like some select REITs, but you need to be careful buying the ETFs, as some are chock full of struggling mall REITs. Homebuilders (XHB) are sitting on their recent lows and are off 15% from their highs reached in January, but are facing some significant cost pressures for both labor and materials (check out lumber prices at your local Home Depot – $4.42 for a single 8 foot 2×4 yesterday!) We would like to note however that in the last cycle, homebuilders took a dive about a year before the rest of the market, so any chirping from that group gets my attention.

Don’t you call this a regular jam

I’m gonna rock this land

I’m gonna take this itty-bitty world by storm

And I’m just gettin’ warm

LL Cool J, Mama Said Knock You Out, 1990

Below you’ll find a new feature, links to interesting reading, as well as tons of charts and all the old favorites, like the trading rules and the SPY trading range. Will we be writing this on the old every other week schedule? That’s the plan, but we’ll see how it goes. Let’s not call this a regular jam just yet.

Also, one big announcement: I recently launched FocusPoint Research, a research service focused on U.S. Banks. If you are interested, shoot me an email. More information can be found here. It’s limited to 75 clients, so the research won’t be widely disseminated. So far, the picks are working out well. But wait, I thought you were launching a different newsletter service last time you wrote a Musings you say? Well, I was – but then we got the opportunity to partner with a great firm that handles all the sales and distribution, leaving us free to focus on research and writing, and it was too good too pass up. So FocusPoint was born.

Here’s the short story: I started my career at Keefe, Bruyette & Woods, working with a great group of people who were hyper focused on producing high quality research on banks. In the 24 years since then, a lot has changed on Wall Street, including MiFID in Europe and the commission structure in equity markets. This led to the demise of truly independent research on Wall Street, as it’s not profitable for investment banks to rely on trading commissions to support research departments. Instead, all their money is made from capital markets, specifically M&A advisory and IPOs. And one quick way to lose M&A advisory work is to be openly critical of your clients. I’ve been told from my friends on the Street about many instances of firms losing business within MINUTES of a critical report being released, and of angry CEO calls to the firm’s management to berate them over the research. In an environment where research analyst pay has been slashed and many positions eliminated, do you think an analyst with a sense of self-preservation is going to want to anger management and cost his firm business? Me neither. But the result is bland, unactionable research that is uniformly bullish or neutral. One firm that shall remain nameless covers 242 companies and has one Underperform rating issued. One. Do they really think the other 241 are all going to meet or exceed the industry average performance? Or are they hoping to do business with the vast majority of companies under coverage? I’ll let you decide. We’ve stepped in the fill the void, and so far, the reception has been better than hoped for. So yeah, I guess you could call FocusPoint a comeback…and we’re hoping to take this itty-bitty bank stock world by storm.

Since we have been out for a bit, it’s probably worth a reminder that all past articles can be found at www.millersmusings.com. But to save you all some time, here are links to the three most popular and recommended articles of the past few years.

September 5th, 2017 – The Sun Also Rises

January 23rd, 2017 – Snow Crash

December 27, 2016 – Being Deeply Superficial

And one that is a not-so-humble brag: Are We There Yet, January 20th, 2016, where I said a turn was at hand in the markets, small caps were oversold, and with oil at $28 and energy companies in the tank, they were a buy. That worked out pretty well… See, I’m not always bearish – it just seemed that way in the fall.

The charts start below, with the Interesting Reading, Rules and Ranges at the end. Enjoy!

Italy’s problems are causing a flight to quality in Europe. Where does the US-Germany spread differential stop?

Italy’s stocks are taking a hit, but it’s the NPLs in the system that should really be worrisome.

Italy’s issues are bleeding into Portugal and Spain again.

More foreigners are buying US Corporate Credit. Flight to Quality? Or rate grab?

The ECB is supposed to wind-down QE in 2019, but earnings have been slow to recover.

Europe also has to watch DB. We’ve been harping on this canary for awhile now at FocusPoint.

Germany’s absolute levels of economic activity are still low, and they are the main driver of the EU.

This looks normal. Switzerland’s central bank is printing money and buying FANG stocks.

Meanwhile in Japan, that famous savings habit has just disappeared. Savings rate now negative as population ages.

10 Year Treasury Spread to 1 year and LIBOR

2-10 Year Treasuries tightened a bit last week.

While 2 year auction demand was down. Lowest indirect as a % of auction since December 2016.

Housing: Purchase demand keeps creeping up, but mortgage rates are increasing fast. Lots of signs are pointing to the U.S. being in a late stage blowoff, including M&A volumes, net worth readings, and Fed overconfidence in its estimates. Each prior cycle these have peaked before a recession. Will this time be different?

Real estate stocks were the canary in the coal mine last cycle. Will it repeat again this time? 30 year inverted vs IYR.

U.S. households don’t have a lot of wiggle room on payments. Debt to disposable income making new highs.

Cash out refis are back in vogue.

So is Margin Debt.

That isn’t helping credit card lenders though.

Global M&A Peaks. Notice anything?

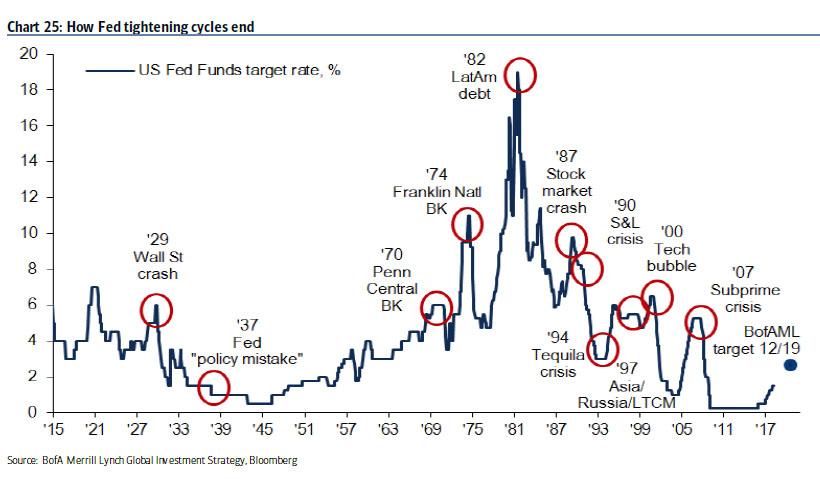

Late cycle on rates and markets.

US Corporate Debt to GDP back to levels where it has peaked in the past. Will this time be different?

Where are the problems going to originate this time? Here’s looking at you Emerging Markets…

Good thing the US corporate bond market is pricing in credit risk, right?

The Fed is seeing higher inflation domestically, so it’s going to keep raising rates, albeit maybe not as much as the market expected. However, the FOMC has a bad track record of getting bullish at the end of a cycle. Shipping and trucking costs are skyrocketing, while commodities are breaking out of a multi-year slump. The big question is, can the international markets handle higher US rates without emerging markets imploding? We’ll see…but my vote is no.

The FOMC is more confident in a strong economy. Fading FOMC economic predictions is usually the right call.

The Fed’s view of Equilibrium Rates now matches the market for the first time in years.

But 5 year, 5 year forward inflation expecations are back down to 2.13% and remained very contained.

Good thing commodity price increases remain contained, right?

Shadow boxing when I heard you on the radio, UH

I just don’t know

What made you forget that I was raw

But now I gotta new tour

I’m going insane

Startin’ the hurricane

Releasin’ pain

Lettin’ you know

You can’t gain or maintain

Unless you say my name

Rippin’

Killin’

Diggin’ and drillin’ a hole

Pass the Old Gold

LL Cool J, Mama Said Knock You Out, 1990

Trading Rules:

- I learned early that there is nothing new in Wall Street. There can’t be because speculation is as old as the hills. Whatever happens in the stock market today has happened before and will happen again. I’ve never forgotten that. – Jesse Livermore

- Markets can remain irrational longer than you can remain solvent. – John Maynard Keynes

- Why don’t you just buy the stocks that are going up and sell the ones that are going down? – Sophia Miller, age 13

Trading Range

We’re set up to keep chopping in this range, with odds on a break up towards the old highs this summer. All the gloom and doom in the news hasn’t been able to keep the market down for long. Pay attention. We may get a flight to safety bid in US stocks and bonds if the Italian situation devolves further.

Resistance: 2740 is big resistance, then 2800/2810. Then big top at 2835.

Support: A little at 2700, tons in the 2680 area, then 2615/2620, followed by weak support at 2590.

Positions in stocks mentioned: Long and short US stocks, long XLP, long TLT, long SPY call options.

Further Reading:

New York housing market weakest in 6 years as global real estate markets increasingly correlate. (FT)

New York and California look to tax carried-interest as income not capital gains. (FT)

Neel Kashkari warns on raising rates too fast again. (FT)

Fed isn’t raising its estimates for equilibrium rates despite the fiscal stimulus. (FT).

Investment Grade bonds have worst start to a year in decades. (FT)

Interesting article on the ways the new Saudi leadership made its money. (WSJ).

Italy in turmoil on Sunday as new government fails to form. (WSJ)

The fine print in the banking bill signed last week. (WSJ)

Very interesting article on the extremely long-term history of banking regulation. Laws of Eshnunna anyone? (WSJ)

Canada’s real estate market is in a seriously big bubble. (Bloomberg)

This podcast from Meb Faber with James Montier from GMO was worth listening to. (Meb Faber Research).

We finally got around to watching Three Billboards Outside Ebbing, Missouri. Much better than expected from the trailer. It’s on the recommended list. Also of note, apparently Rose’ wine should be $15 a bottle and not too dark. (WSJ).

That’s it for this week’s Musings. Please reach out with any comments or questions, and follow us on Twitter for many more articles and thoughts @millermusing.

Miller’s Market Musings is a free market commentary written by Jeffrey Miller, who has been managing money through various market environments for over 20 years. You can subscribe here. If you no longer wish to receive this letter, simply hit reply and put “Remove” in the subject line. Prior posts can be found at www.millersmusings.com.

Mr. Miller has been quoted in financial publications including the Wall Street Journal, Barron’s, American Banker, and New York Times, and he has appeared on Fox Business News, PBS and CNBC. More information and past articles can be found at www.StockResearch.net. Sharing and quoting from this letter is permitted with attribution and a link to www.millersmusings.com.

Miller’s Market Musings, Miller’s Market Matrix and StockResearch.net are not making an offering for any investment or providing any financial advice. It represents only the opinions of Jeffrey Miller and those that he interviews. Any views expressed are provided for informational and entertainment purposes only and should not be construed in any way as an offer, an endorsement, or inducement to invest and is not in any way a testimony for Miller’s other firms. Jeffrey Miller is a Partner at Eight Bridges Capital Management and a Member of Eight Bridges Partners, LLC. Eight Bridges Capital Management, LLC is an exempt reporting advisor with the SEC. Eight Bridges Capital Management solely manages the Eight Bridges Partners, LP investment fund and does not provide any advice to individual investors in any capacity. This message is intended only for informational purposes, and does not constitute an offer for or advice about any alternative investment product. Past performance is not indicative of future performance.

Article by Jeffrey Miller, Partner, Eight Bridges Capital Management