“Cycles are inevitable. Every once in a while, an up- or down-leg goes on for a long time and/or to a great extreme, and people start to say ‘this time it’s different.'” – Howard Marks

Q3 2019 hedge fund letters, conferences and more

The Federal Reserve cut rates a quarter percent on Wednesday. Chairman Jerome Powell assured us there will be further cuts should conditions get worse. Despite the latest cut—the third this year—President Donald J. Trump expressed dissatisfaction with the current 1.50% to 1.75% target. The president pointed to the weak manufacturing report produced by the Commerce Department on Thursday and claimed the strong dollar is hurting American exports. Let’s dig into this a little deeper.

With U.S. interest rates at higher levels relative to the rest of the world, the primary beneficiary of global money flows remains the U.S. capital markets. Better to get a yield of 1.74% in the U.S. than -0.36% in Germany or -0.12% in Japan. Can you see how the large difference might attract capital into the U.S. and thus keep the dollar propped up compared to everyone else? By the same token, however, that makes American goods more expensive to the rest of the world, and slow economies don’t help presidents get reelected.

When foreign buyers convert their local currencies into American dollars to buy our soybeans, wheat, or anything else, it costs them more (#StrongDollar = #WeakExports). If the price point is too high, the buyer will simply look elsewhere. On the flipside, a stronger dollar means a U.S. buyer can get more goods per dollar from an overseas seller. President Trump would like U.S. interest rates to be lower than other countries, and specifically mentioned Germany and Japan. Lower U.S. interest rates would change the global capital flow dynamics, resulting in a weaker dollar, which would help U.S. exporters (#WeakDollar = #StrongExports). Better growth, recession avoided, four more years. Thus the impetus for this particular tweet storm (and the hashtags above).

Interest rate policy decisions play out globally. Setting rates, such as what the Fed did on Wednesday, is one of the levers governments can pull to speed up or slow down their economies. To give you some current footing, yields around the world look like this:

Governments everywhere are seeking to grow out of current high debt predicaments (you’ll see exactly what that looks like below). Everywhere, rates are low and even negative in some places. Is it normal? Is it healthy? That’s a resounding “No!” This is not good.

To give you a sense of the insanity, ask yourself the following question: Would you park your money in U.S. Treasury bonds at 1.74%, or Italian bonds yielding 1.06%, or Greek bonds yielding 1.21%? We sit in a dysfunctional period in time. My two cents: A sovereign debt crisis awaits. The ECB now owns 40% of the Eurozone’s government bonds. Can they avert a crisis? Depends on whether Italy exits—or Portugal or Spain… But when and to what magnitude, I have no idea. Risk? Elevated.

So, the hope is that interest rate manipulation will depress currencies to boost trade, and that the growth it creates will lift the economy. That’s the idea anyway. However, lower-to-negative rates have not helped Germany or Japan lift their economies so far. As Ray Dalio argues, the central bankers are “pushing on a string.” In other words: the tradition of lowering interest rates to improve the economy just won’t work anymore.

Take a look at this from Armstrong Economics:

The European Central Bank’s QE policy has failed to stimulate inflation and has begun to have a negative impact on EU members’ balance sheets. Despite failing to stimulate the European economy, the ECB announced that they will implement their bond-buying program yet again in September at a rate of 20 billion euros per month. Former Greek finance chief described it best during an interview with CNBC, ‘QE the way it has been restructured resembles an antibiotic that has stopped working because the bacteria have grown adapted to it.’

Instead of restructuring worsening policies, the ECB is searching for a scapegoat. Christine Lagarde blamed EU member states for not spending more to stimulate the European economy. ‘Why not use that budget surplus and invest in infrastructure? Why not invest in education and why not invest in innovation?’ Lagarde questioned. Lagarde will be appointed as ECB president this Friday and seems poised to carry out much of the same policies as Mario Draghi.

Which brings us back to the root cause of the global economic illness: debt. If your brother accumulates too much debt, he has less income to spend on new things. More of his money must go toward paying back what he borrowed. His personal economy slows and his stress level rises. He’s desperate to figure out how to escape his mess. For countries, creditable academic research says stress begins when the debt- to-income ratio exceeds 90%.

Today the global landscape looks like this:

If 90% is that stress threshold, what on God’s green earth does 325.8% in the U.S.; 457.7% in the Eurozone; or 595.8% in Japan do to us?

Harry Truman, Doris Day, Red China, Johnnie Ray

South Pacific, Walter Winchell, Joe DiMaggio

Joe McCarthy, Richard Nixon, Studebaker, television

North Korea, South Korea, Marilyn Monroe

Rosenbergs, H-bomb, Sugar Ray, Panmunjom

Brando, “The King and I” and “The Catcher in the Rye”

We didn’t start the fire

It was always burning

Since the world’s been turning

We didn’t start the fire

No we didn’t light it

But we tried to fight it

“We Didn’t Start the Fire,” by Billy Joel

You didn’t start the fire; I didn’t start the fire. It was always burning, since the world’s been turning. We sit late in a long-term debt-accumulation cycle. It’s the root problem in virtually all of the developed world’s economies, and it is further compounded by aging demographics. The stresses we see are being played out on the stage before us.

We all want growth and prosperity. To achieve it, you and I will need to figure this out. It’s complicated, but we’ll get through it. It will take some time, political will, and collaboration. We’ll need to come together to determine how to burn the debt. We’ll need to recognize, too, that along the way, it’s going to get hot.

End Game

The risk of all of this global financial misbehavior is inflation. As Bill White, the former chairman of the Economic and Development Review Committee at the Bank for International Settlements (BIS)—the central banker’s central bank—stated in his presentation at the Mauldin Strategic Investment Conference last May, the Fed’s “crisis-resolution tools are inadequate [this time around]…”

He advised you (and me) to think through the implications of the outcome he sees: deflation first, then inflation. He concluded, “In the end, the only way out of this mess is inflation.”

White added that we should put a lot more emphasis on what’s happening geopolitically, since that’s where the action is going to be taking place. His sign-off? “Good luck. You’re probably going to need it.” With an eye toward geopolitics, let’s look at China.

No Deal with China

Adding to the world’s slow-growth challenges is the burgeoning realization that China may not be a good partner, due to intellectual property theft and global ambitions that clash with a free world’s ideology. I’ve been writing since August about these challenges. My lights turned on during a two-hour car ride from the Bangor, Maine airport to Grand Lake Stream and the annual Camp Kotok gathering of economists, investment professionals, and former Fed officials. Two hours with Jonathan D. T. Ward and I was numb. How didn’t I see this? I wondered. I told Jonathan that this is the seminal issue of our day, and I’ve been rooting him on since.

China’s Vision of Victory (the title of Jonathan’s excellent book) is not a vision of a free world. It is of a world under authoritarian rule. Jonathan’s done an excellent job at getting his message out.

U.S. Secretary of State Mike Pompeo said China’s communist policies are incompatible with U.S. democracy. “We accommodated and encouraged China’s rise for decades—even at the expense of American values, and security, and good sense. We did everything we could to accommodate China’s rise, in the hope that Communist China would become more free, market-driven, and ultimately, hopefully, more democratic,” Pompeo stated. “It is no longer realistic to ignore the fundamental differences between our two systems.”

Bottom line: While optimistic China trade tweets fill the ether, there will be no deal of substance. Global supply chains are shifting—and will continue to do so—as the U.S. and its free-world allies stop ignoring the differences between true democracy and authoritarian-dictatorship rule. It takes time for businesses to move away from a revenue stream and it takes time to reroute supply chains. Add this to the slowing global growth pressures.

After all this, you may feel like you need a drink. Me too, my friend. I see a cold IPA in my near future. But before you crack one open, just put this data into your macro calculus. The point of this global weekly musing is to simply take a step back and do our best to identify where we sit in the economic cycle and the market cycle. Are the odds stacked in our favor, or not?

Keep an Eye on the Trend

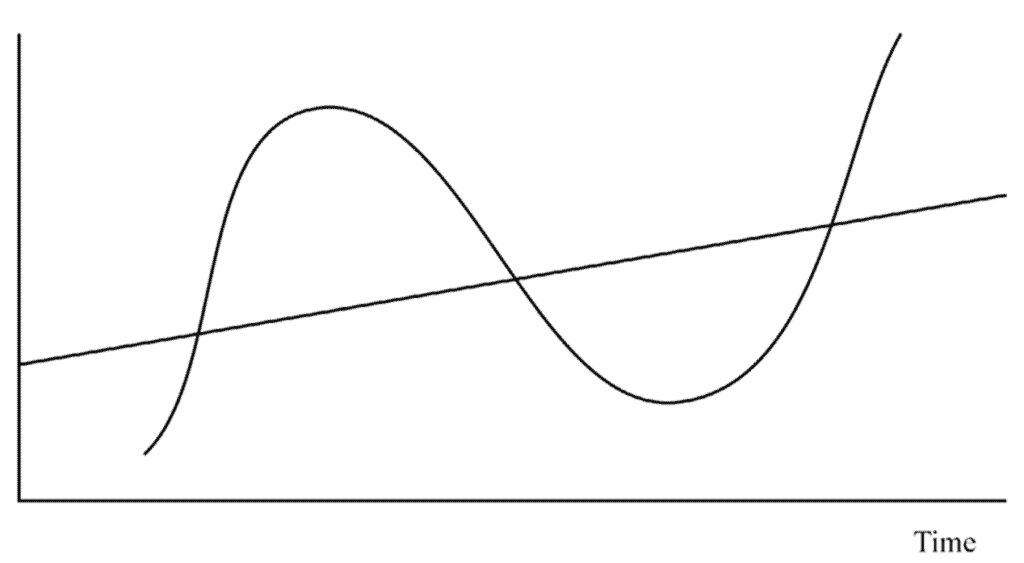

In his must-read book, Mastering the Market Cycles, Howard Marks shares this simple chart:

While there are peaks and valleys along the way, that line is moving up. I’m convinced that businesses will experience consistent growth over time. The problem is that, at times, investors push prices above that trend growth. This creates “market risk,” which is different from “business risk.” Better portfolio diversification can help you deal with business risks. You’ve got to find ways to deal with market risks. That steady line across the middle follows a growth rate of approximately 5% per year above the cost of debt. That’s about how much gain per year you can expect from the stock market. If AAA-rated companies can borrow at 5%, expect your large-cap index fund or ETF to grow at 10%. That’s the predictable return you will get. But depending on where we sit in the cycle, investors may find themselves facing some real issues. If prices are bid up way above that long-term trend, your market risk is high (like today). But prices will always revert back to trend and almost always drop down below the trend (the straight line in the middle of the above chart). This is due to investor psychology. It’s just the way it is, and 36 years of working with investors tells me it won’t ever change.

Knowing where we are in the cycle helps you shape your investment odds. The timing of all dislocations remains largely elusive, but you can measure the probability of your return and the degree of risk you are taking. Simple rule: Play offense when you are at or below trend. Play defense when far above it. And don’t let it stress you out.

Grab that coffee and click on the orange OMR link below. You’ll find the latest Trade Signals commentary and a link to Wednesday’s post. The weight of trend evidence remains strong, so we have that going for us. I also share with you a few charts suggesting that value is a better play than growth. Finally, I share a fun Halloween story from the great Art Cashin in the personal section.

In your favorite chair? Read on…

If a friend forwarded this email to you and you’d like to be on the weekly list, you can sign up to receive my free On My Radar letter here.

Follow me on Twitter @SBlumenthalCMG

Included in this week’s On My Radar:

- High and Growing Dividend Payers

- U.S. Budget Deficit

- Trade Signals – Short-term Investor Sentiment Reading Suggests Caution, Trend Signals Remain Bullish

- Personal Note – A Halloween Encore Presentation

High and Growing Dividend Payers

In the battle of growth versus value, growth has been the winner since 2009. But it may be time to consider value plays. The next chart shows just how overvalued “growth” stocks are today. In the Trade Signals section below, you’ll find a chart that looks at value versus growth and suggests value is where we should position ourselves today.

I’ve written several times that the current period feels eerily similar to 1999. While tech and other growth plays crashed, value went on to do quite well. The problem lay in the overconcentration of related risk (everyone was loaded up on tech), and due to cap-weighting methodology, it was an almost-everywhere problem. But not for value stocks. Today, unloved and unnoticed high-dividend payers are yielding north of 4%. Give me European debt for -0.36% or Greece for 1.21%? No, thank you. I sense opportunity elsewhere.

Source: Ned Davis Research; CMG Investment Research

I have a few ideas in regards to high and growing dividend stocks (email me at blumenthal@cmgwealth.com, if you’d like to learn more).

U.S. Budget Deficit

What a mess! I tweeted this out earlier in the week. I titled it, “Nothing to see here…”

My good friend Mike G. in Chicago sent this awesome reply. Do you remember Leslie Nielsen in The Naked Gun? Nothing to see here… Click on the photo below and enjoy your trip back in time. Mike, you put a big smile on my face (thank you).

Trade Signals – Short-term Investor Sentiment Reading Suggests Caution, Trend Signals Remain Bullish

October 30, 2019

S&P 500 Index — 3,045

Notable this week:

There are no meaningful changes in the indicators this week. The Federal Reserve cut interest rates by 25 bps on Wednesday and stands ready to provide further support if needed. China trade deal hopes are fading and the outlook on the geopolitical front is messy.

Howard Marks said, “In business, financial and market cycles, most excesses are on the upside – and the inevitable reactions to the downside, which also tend to overshoot – are the result of exaggerated swings of the pendulum of psychology. Thus, understanding and being alert to excessive swings is an entry-level requirement for avoiding harm from cyclical extremes, and hopefully for profiting from them.”

On the back of a napkin cycles look like this:

And in real life they look like the chart below. Focus on the middle section of the chart. The dotted red line is the equivalent to the growth line in the above chart. I’ve shared this chart with you before. The important take-away is that we sit well above the long-term growth trend. We will at some point revisit the long-term trend line (red dotted line) and we’ll likely drop below that trend line. This is the “entry level requirement for avoiding harm from cyclical extremes.”

Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Click here for this week’s Trade Signals.

Personal Note – A Halloween Encore Presentation

I wrote about Art Cashin last week and want to share one more note from him with you today. It’s about Halloween, and its very, well, practical origins. And by the way, if you are not reading Art’s daily blog and would like to be added to his distribution list (it’s free, winsome, and full of fun), please email me at blumenthal@cmgwealth.com and I’ll forward your email address to his team. Here you go… I hope you enjoy.

On this day in (approx.) 823 B.C., the most inventive, charming and clever people ever to grace God’s green earth came up with yet another ingenious idea. They were, of course, the Irish (at this time A/K/A the Celts). Being bright, they did not labor upon the obvious. So they let somebody else invent fire, the wheel, iron, astronomy, writing, calendars, etc. These they figured they could copy—and boy did they. These clever folks…. well…..they tended to save their strength for what was really important. By this stratagem, even 1,000 years earlier, while pagan types were grappling with such mediocrity as pyramids, irrigation and geometry, the Celts had learned to distill grain. This miracle medicinal cure (which would maintain mankind for over 3,000 years) they called Usquebah. The amazed and very indebted rest of the world mistranslated the name as “whiskey”.

So for a millennia these wise and whiskey-witty folk enjoyed good health and good fellowship. Then as this particular day approached (circa 823 B.C.), gender problems arose. The women began expecting the men to hang out close to the cave as the evening came earlier each fall. If civilization were to progress, this would never do! So the Celtic elders came up with the second great invention. They called it “Samhain” or end of summer. They explained to the women that as the season changed, ghosts, goblins and evil spirits came forth to threaten all humans. In order to protect the women and children, the men folk selflessly would have to put on old clothes, take some jugs of the magic Usquebah (possible snake bite you know) and go into the hills and light fires.

For nearly 1,500 years the tradition held. Then came the good St. Patrick who was wise enough to keep the Usquebah but drove out the snakes. Conveniently, his Christian teaching did say that November 1st was the Feast of All Saints (or “All Hallows”). So it only seemed logical that if the saints were coming out, the devils would have one last fling. So, snakes or not, we would still need those reliable old clothes, bonfires and protective booze on the eve of “All Hallows” or Hallow’s Evening or Halloween.

To celebrate stop by “The Bog on the Moor” and fortify yourself against snakebite, but quit before ye begin to see the little people. For to go beyond, will surround ye with all kinds of devilment like – banshees and ghoulies and Mother-in-laws.

By Art Cashin

I’m racing to a playoff soccer game today. The Malvern Prep Friars have won three of their last four games and the team has taken shape. Susan coaches and stepson Kieran plays the holding midfield position. The game is two-and-a-half hours away. I’ve loaded up a few podcasts and have a number of calls to make so the drive should go fast. And I’m hoping for some golf this weekend. It looks to be sunny and the late fall colors remain.

Thanks for reading. Hope you had a happy Halloween. Wishing you a fun weekend and great week ahead.

Warm regards,

Stephen B. Blumenthal

Executive Chairman & CIO