In our semiannual letter on the state of small-caps, we delve into what we believe is the next phase for the asset class.

Q2 hedge fund letters, conference, scoops etc

A Smooth Ascent Amid High Anxiety

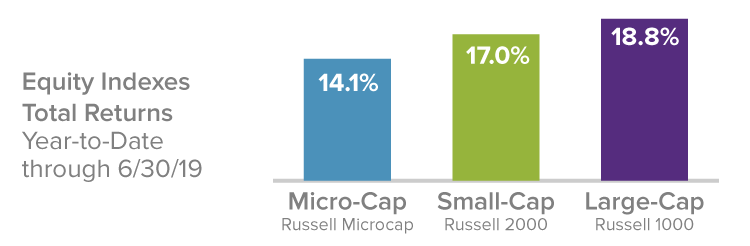

The first six months of 2019 offered equity investors almost everything they could have hoped for following the high anxiety of a recession scare and the bearish fourth quarter of 2018, when the small-cap Russell 2000 Index fell 20.2%. Stocks immediately showed great resilience, and then some, by roaring back in the first half of the year. A highly welcome double-digit rebound in the first quarter was followed by a seesawing second quarter that saw more motion than progress. This was an understandable pause that gave the market time to digest the prior advance. The upshot was a solid advance rise in the year’s first six months, a period that saw low trading volumes and little volatility, which was mostly confined to a small decline in May. During the first half, the Russell 2000 advanced 17.0% while its large-cap sibling, the Russell 1000 Index, was even better, up 18.8%. In fact, performance in the first half generally trended higher the further up the market capitalization scale you traveled.

Some questioned the substance of this rally, observing that the same risks that fueled last year’s decline were still with us. The list is long and, by now, familiar. Most of the anxiety continues to circulate around the issue of global growth—or the widely rumored imminent lack of it—and its probable negative impact on corporate profits. There wasn’t much in the way of fresh answers to these concerns at the end of June beyond the admittedly consequential Fed pivot to a more dovish stance (as well as subsequent and similar actions promised from the European Central Bank). Yet, while the Fed’s words and actions went some way to reassuring investors that it was prepared to give the markets a dose of stimulus, the effect on economic growth was pretty much nil. Moreover, the increasing tensions around trade and tariffs remain an issue at this writing. With no resolution forthcoming, many companies were lowering expectations and/or offering a more muted outlook, with predictably negative effects on the stocks of many economically sensitive businesses.

It’s not surprising, then, that equity investors showed a marked preference for safety in the form of large-cap stocks, or chose to bet on better times further down the road by vacuuming up shares of growth issues regardless of capitalization size. Some additional context is also important: large-caps, growth stocks, and defensive areas (that is, bond proxies) have historically done better in low or declining interest rate environments, an atmosphere that has characterized much of the decade following the Financial Crisis, with its record-low interest rates (and the ‘easy money’ that came with them). With rates still near historic lows, these same stocks have led the market over the last two-plus years. All of this notwithstanding, we believe that the long-term case for small-cap stocks is strong, as we will explain through the course of this letter.

Pessimists, Optimists—and Us

By periodically inverting the otherwise mostly flat yield curve, the bond market maintained its saturnine insistence that the economy was slowing and potentially, perhaps inevitably, moving toward recession. To be sure, many observers point to the inverted yield curve as iron-clad proof that the current slackening momentum in the pace of growth in the U.S., along with the advanced age of the expansion, is a prelude to a recession. More optimistic voices argue that large-cap stocks spent much of the first half making new all-time highs, that the labor market continues to strengthen, and that the economy continues to expand in spite of a raft of dismal headlines.

Our own cautiously constructive view is rooted not so much in the macro factors that dominate the headlines but in our own research into companies, their industry dynamics, and our conversations with management teams. We do, however, agree with those who think the U.S. economy is not heading toward recession; we see periodic slowdowns and accelerations in the pace of growth as historically typical. As for the yield curve, the market appears to have figured out before the Fed that persistently low inflation exerts a powerful flattening effect on the curve. To make our case, we have taken up arms—or at least data points—against this sea of troubles to argue for the long-term appeal of fundamentally sound small-cap cyclicals. We see good reasons for investors to be optimistic about the prospects for small-cap stocks, specifically those cyclical areas that populate our portfolios.

The Case for Small-Cap Leadership

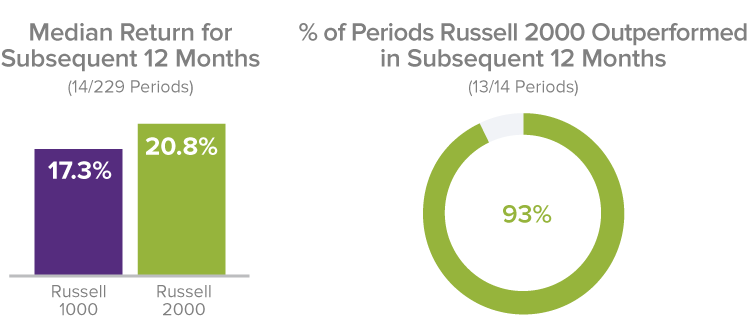

Our first argument is in favor of small-cap returning to market leadership. We make it on the grounds of reversion to the mean, one of our longest-held investment principles. Looking at first-half performance, the resilience of small-cap stocks seemed both apropos and encouraging to us given that we continue to see solid fundamentals for many companies, attractively joined with historically average, or below average, valuation levels. However, small-caps lagged large-caps not only in the first half but also for the one-year period ended June 30, 2019, when the Russell 2000 fell 3.3% versus a gain of 10.0% for the large-cap index. This performance divergence has created a historical oddity that can be seen in the spread between small- and large-cap returns. It rarely happens over the course of a 12-month period that small-caps are in the red while large-caps are in the black. In fact, it’s happened less than 7% of the time over the past 20 years—in 16 out of 229 monthly rolling 12-month periods.

What are the implications of this peculiar divergence in performance? In 93% of the following 12-month periods—only 13 of the 14 currently have subsequent periods to measure—small-caps bounced back to outpace large-caps. It’s true that small-caps have historically tended to lag their large-cap siblings when yields are falling—and have often done the same when economic growth is slowing. The resumption of small-cap leadership, then, is contingent on these conditions changing. When rates rise (or simply normalize) and/or the economy reaccelerates, and history strongly suggests that both should, we would expect small-cap to recapture leadership.

What Happened After 12-Month Periods When Large-Caps Rose and Small-Caps Fell?

16 out of 229 Trailing 1-Year Periods from 6/30/99 to 6/30/19

One additional observation on relative performance: From December 31, 1978 through June 30, 2019, the five-year monthly rolling average return was 10.6% for the Russell 2000 and 11.7% for the Russell 1000, while the five-year average annual total returns for the small- and large-cap indexes for the period ended June 30, 2019 were 7.1% and 10.5%, respectively. With small-caps well below their long-term average, we expect performance to improve to a greater degree than for large-caps, which finished June much closer to their long-term average.

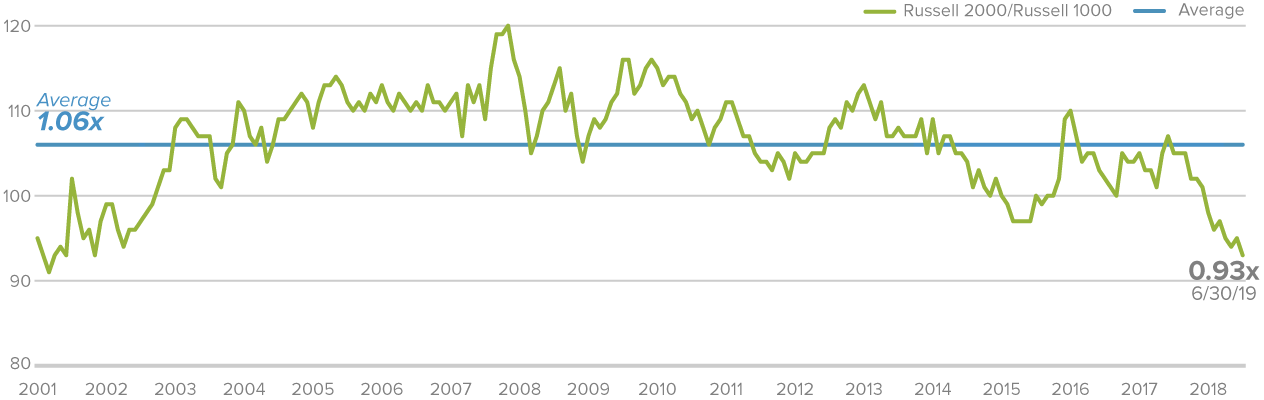

Our confidence in mean reversion is further grounded in the relative valuation spread between the Russell 2000 and the Russell 1000 at the end of June, which was significantly below its long-term average based on each index’s median last 12-months’ EV/EBIT (enterprise value over earnings before interest and taxes). In fact, small-caps have lagged large-caps for such an extended period of time that they finished June at their cheapest relative to large-caps since 2001.

Small-Cap’s Relative Valuation Is Significantly Below Its Long-Term Average

Russell 2000 vs. Russell 1000 Median LTM EV/EBIT¹ (ex. Negative EBIT Companies) from 12/31/01 to 6/30/19

Source: FactSet

1Enterprise Value/Earnings before interest and taxes.

So while no one thinks that stocks are currently bargain priced, it’s also true that the vast and diverse universe of small-cap stocks contains a considerable number of attractive risk/reward opportunities based on the combination of reasonable to attractive valuations (again measured by median EV/EBIT) and profitability.

“While no one thinks that stocks are currently bargain priced, it’s also true that the vast and diverse universe of small-cap stocks contains a considerable number of attractive risk/reward opportunities based on the combination of reasonable to attractive valuations (again measured by median EV/EBIT) and profitability.”

The Valuation Situation

When looking for investment candidates, we typically survey the small-cap market for what looks to us like excess pessimism—which is precisely what we’ve been seeing in certain cyclical areas over the last couple of years. Our practice is to then investigate how much of that negative sentiment is already reflected in the current stock price of a given company. So it was significant that at the end of June, cyclical stocks were selling at a greater discount to the Russell 2000 than they had during the fall of 2008—in the teeth of the Financial Crisis. To us, that is the very definition of excess pessimism.

Source: FactSet

2Enterprise Value/Earnings before interest and taxes.

We suspect that these relatively inexpensive valuations are in large part the result of investors placing undue emphasis on daily macro headlines when trying to understand or anticipate small-cap market movements. (The frequently missed distinction between slower economic growth and a recession is an example of the trouble this can lead to.) We think that investors often fail to fully appreciate the “reaction function,” the response of businesses, central banks, and governments to slowdowns. While we are by no means macro forecasters, it would not surprise us if the global economy grew a little faster over the next year. If history is any guide, this reacceleration could boost small-cap stocks, which have done well on both an absolute and relative basis, especially versus large-caps, when the ISM Manufacturing Index (a common proxy for economic conditions) is on the rise. As unlikely as it seems, additional growth could come from a U.S.-China trade deal that addresses tariffs and stokes even modest growth in China, which would likely spur increased activity in Europe as well.

Moreover, we expect profitable companies in select cyclical areas to do better regardless of which route the global economy takes in the short term. For example, and in spite of reports of revisions, earnings prospects for the second half of 2019 look solid for many of our small-cap cyclical holdings, especially given the relatively weaker third and fourth quarters of 2018 with which 2019’s two second-half quarters will be compared.

We often seek to identify opportunities at the intersection of quality and value—that is, companies with average or better profitability and lower-than-average valuations. There were three cyclical sectors that had higher-than-average profitability and lower-than-average valuations at the end of June—Industrials, Consumer Discretionary, and Materials.3 The relative attractiveness of these and other cyclical areas dovetails nicely with our bottom-up approaches, where the search for fundamentally sound, well-managed companies with solid growth potential has more recently led us overwhelmingly to cyclical businesses.

3Based on the relation between each sector’s average return on equity (ROE) for the five years ended 6/30/19 (excluding companies with negative ROE) and median EV/EBIT (excluding companies with negative earnings).

Small-Cap Stocks and the Urge to Merge

The appeal of small-cap stocks can also be seen in recent merger & acquisition (M&A) activity. The number of small-cap M&A deals in the U.S. hit a 10-year high in June, with 503 transactions announced for the trailing four quarters through the end of that month, according to Bloomberg data. This is the largest number of deals in the asset class since before the Financial Crisis. We anticipate that this trend will continue for a variety of reasons. CEO’s are under relentless pressure to grow profits. If they believe organic growth opportunities are limited, then inorganic paths such as acquisitions begin to make sense. Along similar lines, the CEO of a small-cap company might look more favorably on a buyout offer at a significant stock price premium if he or she sees limited opportunities for their own organic growth. However paradoxical, we can see how a further deceleration in economic growth could lead to an acceleration in M&A deals. With their attractive relative valuations, many small-cap companies should continue to be attractive takeover targets. We also think that many better-managed small-cap businesses will continue to be active as acquirers. We meet with many management teams that run companies with strong balance sheets and are eager to find ways to grow. With interest rates so low, many acquisitions are likely to be accretive, which increases their attraction to a potential buyer.

The Next Leg of the Journey

Disagreements about the condition of the market and state of the economy have created opportunities for active managers and other discerning stock pickers because there’s so little consensus about what constitutes value or quality. Somewhat counterintuitively, this has made us generally quite comfortable with what we’re holding in each of our strategies.

Of course, our overall cyclical tilt would not immunize any of our portfolios from a recession. However, the market has provided opportunities to build portfolios that we think are not only inexpensive, but that we think should also provide healthy returns going forward in our most valuation-sensitive strategies. We also expect that many of our high-quality holdings (specifically those in Industrials and Information Technology) could outperform cyclicals in general in the event of a recession thanks to their status as market leaders in global niches as opposed to being one of many players in a highly fragmented commodity business.

Across all of our strategies, we’ve been adding or holding positions in areas such as technology, industrials, and many other areas that we think should do well under present or improved conditions. Equally important, many of these holdings already have valuations that seem to reflect a high probability of an imminent recession. Any economic news that shows improvement—or simply the absence of worsening conditions—may lift these stocks.

In framing this promising picture of the long-term possibilities for small-cap cyclicals, we also recognize that the lengthy list of current risks is creating an even higher level of uncertainty than usual. However, having done this for as long as we have—four decades and counting—we are also highly aware that the markets seldom do what’s most expected. Given today’s widespread concerns about slowing growth, increasing trade tensions, and the extended economic cycle, the most surprising outcome—as we’ve suggested—might be a rally catalyzed by improved growth.

“We also see four favorable factors in the current market environment—low inflation, modest valuations, moderate growth, and increased access to capital—that we think support solid-to-strong small-cap performance in the intermediate term regardless of current anxieties.”

When looking forward, we believe it’s appropriate to be humble about our own forecasts and respectful of those that differ from ours. With what seems like ever increasing tariff and trade tensions, there is a plausible negative scenario of slowing Chinese growth that tips languishing European economies into recession and pushes global yields even lower. This would in all likelihood lead to greater instability in global financial markets as well as breeding heightened risk aversion. While we think this outcome is less likely than others, we also believe that investors should remain mindful of the reaction function we mentioned earlier. Additionally, environments that feature increased uncertainty, turbulence, and market volatility often provide opportunities for companies with leading market positions and strong balance sheets to solidify or expand market share. Volatile environments have also been historically favorable for active small-cap managers. We also see four favorable factors in the current market environment—low inflation, modest valuations, moderate growth, and increased access to capital—that we think support solid-to-strong small-cap performance in the intermediate term regardless of current anxieties. These four factors paint an attractive picture in our view, one that small-cap investors might be at risk of missing if they pay more attention to the macro picture than to company fundamentals, where we think the real action is.

Article by Royce Funds