Gotham City Research argues Carvana’s (NYSE:CVNA) “turnaround” depends on opaque related-party economics tied to DriveTime/Bridgecrest leverage and loan-sale gains.

Gotham City Research’s Opinions

- CVNA 2023-2024 earnings are overstated by $1 billion+, and far more dependent on related parties than disclosed.

- DriveTime’s leverage fuels CVNA Adj EBITDA. Without DriveTime credit, CVNA earnings collapse, and CVNA Adjusted EBITDA doesn’t cover its interest expense.

- CVNA 2025 10K will be delayed, 2023/2024 10Ks restated, BLAST ABS restated, & Grant Thornton will resign as auditor.

- CVNA and DriveTime creditors’ ability and willingness to fund this scheme will change once they realize that the ecosystem is more levered than publicly disclosed.

The following reverse pyramid depicts what we believe, along with the complex interplay between CVNA’s earnings and its related parties:

Summary Of The Bases Of Opinions

- DriveTime burned over $1 billion in cash flow from operating activities, and Free cash flow, from 2023-2024.

- DT generated over $1 billion in cash flow from financing activities via debt issuance, from 2023-2024.

- DriveTime leverage in 2023/2024 sits at 20x-40x, far higher than historical levels (capped at 10.3x before 2023).

- DriveTime’s ratio of adj EBITDA to interest expense = 0.5x-1.0x , for 2023-2024. Far lower than previous years.

- DriveTime marked down its loan portfolio by $900m while CVNA recognized gain on Loan sales of $755m in 2024.

- CNVA 10K ’24 claims it has and may sell loans to DriveTime, but the DriveTime AR does not confirm this claim. Neither CVNA nor DriveTime disclose when nor how much.

- We have uncovered dozens of loans tied to cars that CVNA sold, that appear on Bridgecrest balance sheet and VinAudit reports.

- Bridgecrest is listed as the originator yet both DriveTime and Carvana filings don’t disclose Bridgecrest as originator.

- CVNA claims Bridgecrest is a third party servicer, but BAC is fully owned by Ernie Garcia II.

- We estimate Bridgecrest earns a very low servicing fee of 0.117% per year on loans sold by CVNA to “Third parties”

- We believe CVNA sells loans to “third parties” at inflated rates (booking Gain on Sales). in exchange BridgeCrest charges these “third parties” with very low servicing fees.

- GoFi LLC is fully owned by Garcia II. Like DT, GoFi burned cash in 2023 and 2024. GoFi revenues are GoS from DriveTime, and its expenses are payments to DriveTime.

- GoFi and Carvana share the same mailing address.

- We have detected accounting irregularities in sales commissions and servicing reported figures.

- Carvana, DriveTime/Bridgecrest, GoFi all share the same auditor, Grant Thornton. Same auditor as Tricolor.

Introduction

Carvana (“CVNA”) appears to show signs of an unquestionable turnaround story. Sentiment on the street has shifted from fear to greed. For example, Morgan Stanley, who had a $1 stock price target in 2022, upgraded its CVNA bull case to $750 on “robotaxi optionality thesis” just a few weeks ago.1 Yet Gain on loan sales + related party income drive 75% of 2025YTD adj EBITDA:

Although Carvana’s revenue growth has been impressive, the resulting scale in its business has not diminished CVNA’s reliance on these sources for profit. Many skeptics have claimed that CVNA uses DriveTime (“DT”) to artificially boosts its reported results, and that Ernie Garcia II funds DT’s losses, but the market consensus is that everything is disclosed.

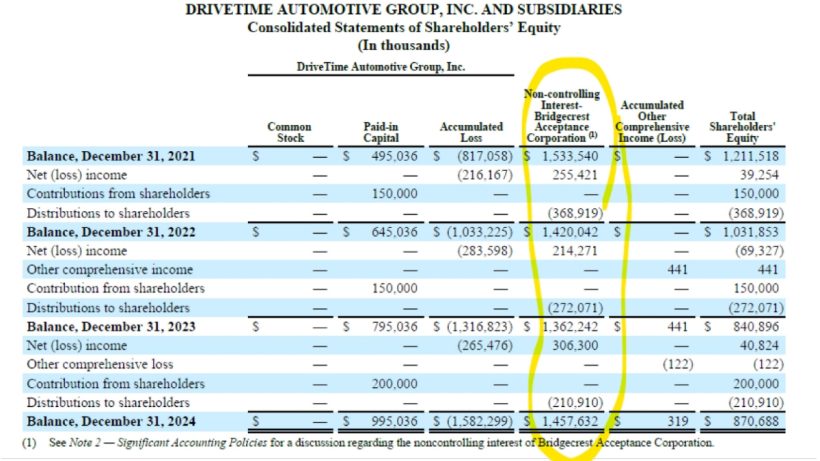

Actually, we found this is not the case at all. We obtained the DriveTime’s 2024 Annual Report through a Freedom of Information Act request, and we believe it is a smoking gun that reveals many undisclosed facts about related party DriveTime. A cursory glance of the financials shows:

- DriveTime burned over $1 billion in cash from 2022-2024. 2022-2024 net margins are 0%.

- To fund this $1 billion hole, DriveTime issued more than $1 billion in debt, levering up 20x-40x in 2023-2024, after years of leverage far lower, and never exceeding 10.3x.

- DT Profits don’t cover interest expense, as coverage ratio fell to 0.5-1.0x, from over 2x.

Last Friday, in an ongoing class action litigation against Carvana, it was revealed that CVNA is trying to keep DriveTime’s financial statements sealed from public view.4 From the above facts, we can see why, but that just begins to scratch the surface of something far more dangerous:

- DriveTime marked down $5.9 billion of loans by -15%, and its loans historically lose -30%. These toxic loans are what backs DriveTime’s debt issuance, at 20x-40x leverage.

- GoFi sells loans to Bridgecrest at prices above fair value, then GoFi pays back Bridgecrest with these Gain on Sales. This helps GoFi book revenue, and Bridgecrest boost profits.

- We believe Carvana uses Bridgecrest to book artificial Gain on Sales in a similar way as GoFi does with Bridgecrest.

- In Bridgecrest securitization filings, Bridgecrest and GoFi appear as originators of loans tied to cars sold by CVNA. Yet the CVNA 10K, DriveTime 2024 annual report and GoFi 2024 AR do not mention that Bridgecrest or GoFi originates loans for Carvana.

- We see accounting and disclosure discrepancies between CVNA and DriveTime. Meanwhile, Grant Thornton, who was Tricolor’s auditor, audits all three Garcia entities.

Gotham City Research believes CVNA’s earnings are more dependent on its related parties than disclosed; and more levered indirectly than assumed, as DriveTime’s leverage drives CVNA earnings. We see problems with accounting, disclosure, and business practices that will lead to regulatory trouble. At best, we believe CVNA is far less profitable than believed, as a standalone business. At worst, CVNA is more like Tricolor5, rather than Amazon6. Either way, shares face massive downside risk to the share price.

Gotham City Research Carvana Full Report: Download

DriveTime 2024 Annual Report - obtained via Freedom of Information Act: Download

GoFi LLC 2024 Annual Report - obtained via Freedom of Information Act: Download