The Following Is an Investment Opinion On DraftKings Inc (NASDAQ:DKNG) Issued by Spruce Point Capital Management

NEW YORK, October 3, 2025: Spruce Point Capital Management, LLC (“Spruce Point” or “we” or “us”), a New York-based investment management firm that focuses on forensic research and short-selling, today issued a detailed report entitled “Predicting More Downside Risk” that outlines why we believe and estimate that shares of DraftKings Inc (NASDAQ:DKNG) (“DKNG” or the “Company”) face up to 35% – 60% potential long-term downside to approximately $14.00 - $22.00 per share, representing material risk of market underperformance. Download and view the report, disclaimers, additional information, and exclusive updates by visiting www.sprucepointcap.com.

Spruce Point Report Overview:

After conducting a forensic review of DraftKings Inc. (Nasdaq: DKNG) (“DKNG” or the “Company”), we have serious concerns regarding the impact to DKNG’s sportsbook market share given the significant volume, or handle, being generated by emerging prediction markets for sports betting such as Kalshi and Polymarket. Spruce Point has been following the DKNG story closely, and despite the recent share price movement and other prescient short-seller critiques, we believe there is still significantly more downside risk because investors and sell-side analysts are not fully understanding the gravity of the situation and long-term disruptive impact on the Company’s business. Our report details why we believe that the prediction exchanges will take more market share than predicted and that legal challenges to the exchange model are unlikely to be resolved quickly. Based on our evaluation, we estimate 35% - 60% potential downside and market underperformance risk. The report highlights several key concerns with the Company, including:

- We believe Kalshi and other sports prediction markets will continue to operate while state litigation drags on. We believe the U.S. Supreme Court will have to ultimately decide on their legality which may not happen until summer 2027.

- It appears DKNG will have to sit on the sidelines while the litigation continues. State gaming commissions have warned online sportsbooks such as DKNG not to enter the prediction markets.

- Kalshi appears to offer better odds than DKNG which we believe is driving Kalshi’s rapid handle growth and potential market share capture.

- We believe the market has misinterpreted Kalshi’s handle and hold rate and sell-side analysts have been reluctant to lower DKNG’s consensus revenue estimates.

Executive Summary

We acknowledge there is still a lot of uncertainty when it comes to prediction exchanges for sports. The central conflict is whether event contracts are financial derivatives regulated by the federal government or a form of gambling regulated by the states. In other words, does the CEA give the CFTC exclusive jurisdiction over event contracts, or do states have the authority to regulate or ban them as a form of gambling? There exists a litany of articles and debate around this topic, but our concern is not the outcome of the litigation, although we believe it is a major risk for all the online sportsbook betting (OSB) operators. Rather our concern is the amount of time it will take to get to a final decision on whether sports prediction exchanges will be allowed to operate freely in all 50 states.

Spruce Point Believes Kalshi Will Continue To Operate While Litigation Continues

Regulators in states such as Nevada, New Jersey, and Maryland issued cease-and-desist orders to Kalshi, arguing its contracts constitute unlicensed sports gambling. In response, Kalshi sued the state gaming regulators in federal court, arguing that as a DCM regulated by the CFTC, federal law preempts state gaming laws. Kalshi won preliminary injunction in Nevada and New Jersey but was denied in Maryland. Spruce Point engaged a sports gambling attorney to help us assess both the likely outcomes of all the litigation and more importantly the timelines. Ultimately, we believe the market is mispricing the risk of DKNG losing market share during its peak Q4 earnings season given MLB playoffs, start of the NBA season, and the NFL and NCAA football seasons. Furthermore, we believe the markets should be pricing in some Trump risk. With Donald Trump Jr. being an advisor to both Kalshi and Polymarket it is not inconceivable that a simple one sentence amendment to the CEA is put into a larger bill which passes through Congress, instantly codifying federal jurisdiction and rendering all state-level challenges irrelevant. Spruce Point believes there are two more likely scenarios which represent very significant risk to all the OSB operators: 1) The ability for the CFTC to implement a new federal rule making it clear they have jurisdiction and oversight of the sports prediction exchanges. With a Trump-nominated Chair, we believe this risk is real. We acknowledge this will be disputed by the states but we believe this litigation could take minimum of a year but more likely two to be resolved. 2) The oral argument for the NJ case before the U.S. Court of Appeals for the Third Circuit occurred on 9/10/25. Spruce Point believes the non-prevailing party will file a petition by Feb. ‘26 for a hearing with the U.S. Supreme Court (SCOTUS). We believe SCOTUS has until June ‘26 to decide if they will hear the case, then oral arguments would happen between Oct. ‘26 and Apr. ’27 with a decision in June ’27. Finally, Massachusetts filed a lawsuit against Kalshi and its partner Robinhood on 9/12/25. In response, Kalshi filed a Notice of Removal, in an attempt to shift the lawsuit from state court to federal court but MA responded with a motion to remand its lawsuit against Kalshi back to state court. Spruce Point believes the MA case will end up in the federal court and a petition to SCOTUS.

It is very important to note, when considering injunctions, federal judges are required to apply two key tests: irreparable harm and public interest. We believe Kalshi’s sportsbook-level handle on its exchange speaks directly to both. Shutting it down would disrupt a functioning, federally regulated market (irreparable harm), and courts are reluctant to dismantle platforms serving thousands of participants without incident (public interest). Together, these factors make it far more likely that Kalshi continues operating while litigation drags on.

We Believe Prediction Markets Are Unlikely To Expand TAM For OSBs In The Near Future

We believe DKNG and the other OSB operators are stuck between a rock and a hard place. From our understanding, the Ohio Casino Control Commission is one of the more prominent gaming regulators across the country. The commission has warned licensed sportsbooks in the state that offering or associating with prediction exchanges could put their licenses at risk. We also believe that Flutter appeared before the Nevada gaming commission where they addressed questions regarding a potential arrangement with Kalshi. Finally, we believe the nail in the coffin on this topic is the fact that the Arizona Department of Gaming recently warned OSBs that offering prediction markets inside or outside of AZ may jeopardize their licenses.

Our debate is not about what ultimately happens with sports prediction exchanges in the next year or two and who wins/loses the litigation. Our position is we do not believe DKNG or any other OSB operator would risk their gaming licenses by launching sports prediction exchanges in the next 3-6 months or in the next year or two while the CFTC and the states are potentially embroiled in further litigation or a pending SCOTUS decision. Flutter/FanDuel’s partnership with CME was very clear to exclude sports. Even if DKNG decides to launch a sports prediction exchange on their own or acquire Railbird, our research indicates it could take 6-18 months for final CFTC approval and launch. With DKNG and the other OSB operators on the sidelines, Kalshi, Polymarket and others can continue to take market share. Individuals in CA, TX, GA, and the other 21 states where DKNG does not operate likely have never heard of Kalshi, Polymarket, etc. as most may assume all betting is prohibited. We believe the individuals who do know the prediction exchanges are those already in online sportsbook states, familiar with betting platforms, and often active across multiple operators to chase promotions or better odds. We do acknowledge Kalshi’s partnership with Webull and Robinhood which has 26.5 million funded accounts across the U.S. Spruce Point also believes the impact to DKNG could be more severe given in 2024, 61% of its revenue came from its U.S. sportsbook vs. only 29% for Flutter.

Kalshi Appears to Offer Better Odds Than DKNG

While investors and sell-side analysts continue to debate the long-term TAM question, Spruce Point has been closely monitoring Kalshi’s odds and reported handle. There seems to be a lot of debate around the odds offered on prediction exchanges vs. OSBs. While we acknowledge there are going to be variances, we believe the economics favor Kalshi. We believe on average Kalshi charges just 1–2% per trade, while DKNG builds in an 8–10% vig and further adjusts its odds to protect its book. We believe sportsbook customers consistently shop for better odds. We do not think it will take long for the market to recognize this opportunity and in fact we believe it is already happening.

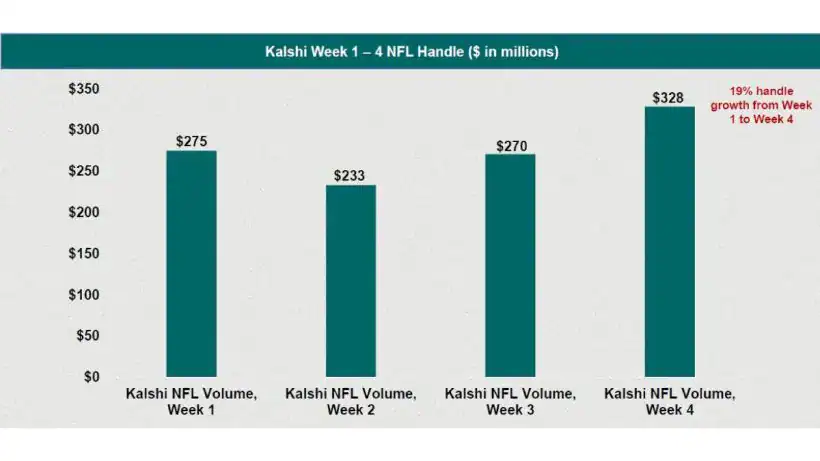

Kalshi Handle For NFL And NCAA Football Should Be Setting Off the Fire Alarm

In 2024, the total handle from the licensed online sportsbooks across 33 reporting markets combined to generate ~$150 billion (DKNG operates in 26 of the 33 states). The state of NY Gaming Commission reports weekly sports wagering by operator and reports the total combined figure. In 2024, NY generated a total of $22.7 billion in sports wagering and from Sept.-Dec. 2024, total weekly sports wagering averaged $513 million per week. We grossed up NY’s $513 million per week by 6.6x ($150 billion / $22.7 billion) to get to an estimate for the weekly sports wagering for all 33 reporting markets. During Sept.-Dec. 2024, we estimate $3.4 billion of weekly sports wagers in the 33 reporting markets. The state of CO publishes the monthly amount of sport wagering by sport. From Sept.-Dec. 2024, the NFL and NCAA football games represented on average 27% and 7% of total sport wagering, respectively (excluding parlays). Based on these figures we estimate the 2024 total weekly NFL and NCAA football handle to be ~$914 million and ~$237 million, respectively.

We believe the scale of the disruption is already evident. During the first four weeks of the NFL season, Kalshi generated on average $277 million of handle per week. This represents ~30% of the weekly NFL handle that the OSB operators generated during Sept.-Dec. ‘24. During the first five weeks of the NCAA football season, Kalshi generated on average $187 million of handle per week. This represents ~79% of the weekly NCAA football handle that the OSB operators generated during Sept.-Dec. ‘24. In five weeks, Kalshi grew its NCAA football handle by 80% and in four weeks grew its NFL handle by 19%. Spruce Point believes the disruption is clear given DKNG’s NY sportsbook handle declined 8.9% from Week 3 to Week 4 of the NFL season in ‘25 vs 8.1% growth in ’24. Kalshi grew its NFL and NCAA football handle by 31% in the same week, a widening divergence that highlights Kalshi’s potential share capture at DKNG’s expense.

We see more alarm bells from Kalshi filing to self certify for parlays. In fact, Kalshi launched a parlay product during Monday night football on Sept. 29th. We believe parlays are DKNG’s most lucrative revenue stream. Kalshi did run an advertisement during the NBA finals but according to our research no ads have been run since. Spruce Point believes the fire alarms should be ringing as DKNG’s 2025 consensus revenue estimates seem to be at risk. Furthermore, if the CFTC does step in and implements a new federal rule or the state cases go before SCOTUS, we believe DKNG’s 2026 consensus estimates are at risk as well.

We Believe The Market Has Misinterpreted Kalshi’s Handle And Hold Rate

We believe the market has attempted to dismiss Kalshi’s handle as inflated. Two misconceptions recur. First, some claim each contract is counted as $2 of handle on Kalshi when only $1 is staked since a contract involves both a buyer and a seller. Upon review of Kalshi’s disclosures and through email confirmation from the company, a buyer at 30 cents and a seller at 70 cents are matched and reported as $1 of volume, not $2.

Second, critics argue that resales exaggerate handle. Making this argument conveniently leaves out that the contract is trading hands but it’s a separate market participant buying the contract. Kalshi’s handle isn’t inflated, it reflects real capital allocation decisions. Each trade is a customer transacting with Kalshi. The contract is the same, but each trade is a separate economic decision by a different buyer or seller. The individual buying the “re-sold” contract is brand-new money that could have gone to DKNG or others but didn’t. Kalshi’s handle is not an artificial inflation, it reflects real competitive diversion of wallet share away from OSB operators. Put another way, every dollar of handle on Kalshi is a dollar decision to use Kalshi over DKNG.

Typically, OSB operators keep $8–$10 of revenue on every $100 wagered through their 8–10% vig or margin. The 8-10% is the built-in margin if bets were perfectly balanced. DKNGs actual sportsbook hold is ~6-8%. Spruce Point believes there is some perception by the market recently that the exchanges hold rate is ~4%. Spruce Point’s research indicates the hold rate is closer to ~1.5%. In other words, if DKNG pivots into exchanges in the coming years, the TAM expansion opportunity touted by sell-side equity analysts and others might not live up to expectations. In addition, once all the litigation settles, we believe sports prediction exchanges will either operate in all 50 states or none unless the exchanges pivot to gambling licenses and paying taxes. We believe there is a TAM expansion opportunity for DKNG if the sports exchanges are free to operate in the 50 states but we believe it is also a very significant TAM and EBITDA detractor for DKNG’s business in its current 26 state sportsbook presence as a large portion of DKNG’s hold rate could fall from 6-8% to the 1.5% to 3% range.

Read the full report here by Spruce Point Capital Management

About Spruce Point

Spruce Point Capital Management, LLC is a forensic fundamentally-oriented investment manager that focuses on short-selling, value and special situation investment opportunities.