Kerrisdale Capital is long shares of Buzzi SpA (BIT:BZU), an €8.9 billion market capitalization cement company headquartered in Italy.

Buzzi is the best managed cement company in the world. Over the past 30 years, the company has grown EPS at a CAGR of 15%, transforming a sleepy little Italian cement company into a global stalwart generating more than half its EBITDA in the United States. Management works for shareholders and focuses on the long term: twenty years ago, the Buzzi family owned 44% of shares, and today they own 56%, paying themselves zero stock options. Buzzi’s profit margins are higher than every other major cement company we could find, and within spitting distance of vaunted aggregates players Martin Marietta (MLM) and Vulcan Materials (VMC), which trade at ~33x and ~35x P/E on 2025E consensus. Buzzi’s M&A track record has been stellar, its revenue growth steady, its capex budget savvy, its investor disclosure supple, and its stock compensation expense zero. Yet despite boasting the best operating metrics in cement, by the most aligned management in the industry, Buzzi has been awarded one of the lowest valuation multiples among Western cement players – at 11x P/E – for one, simple reason: racism. Buzzi is Italian. Long-ingrained prejudices against a wine-guzzling people known more for hours-long aperitivos than capital allocation has burdened the best cement company in the world with an offensively putrid valuation. Buzzi shouldn’t be trading at the lowest multiple in the global cement comp set. It should be trading at the highest. Make Italy Great Again!

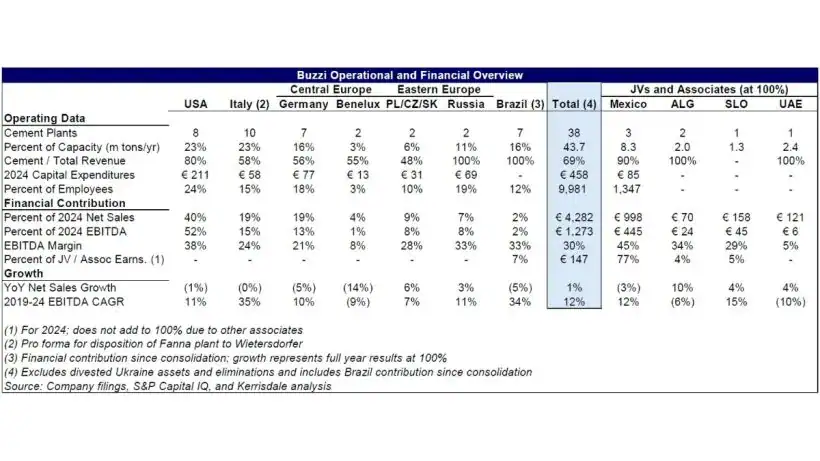

The math is simple. Buzzi generated 40% of its revenue and 52% of its EBITDA in the United States in 2024. The company has doubled its U.S. revenue organically over the past 10 years, and its American assets generate margins consistently above other U.S. players. Yet Buzzi’s U.S. peers trade at 12x 2025E EBITDA. In Europe, Heidelberg and Holcim trade at 9x-11x 2025E EBITDA. By contrast, Buzzi trades at just 6.8x 2025E EBITDA, and that excludes €1.2 billion of value from its high-margin Mexican business and other minority-owned assets. If Buzzi was valued in line with its comps, the stock would be worth twice as much.

It's not as if Buzzi is an illiquid small cap; the stock trades more than €50 million per day and the equity is worth €9 billion. The only explanation we’ve come up with is prejudice. If the company was named Bennett instead of Buzzi and headquartered in Alabama instead of Casale Monferrato, shares would probably double overnight. Non è giusto! That’s not fair! European cement players with significant U.S. assets have seen valuations expand over the past year, whether catalyzed by corporate action as in the case of Holcim and Titan, or by growing investor awareness, as with Heidelberg. We believe Buzzi is the next player to benefit, as the company cements its reputation as a top operator in the world’s most ubiquitous construction material.

I. Investment Highlights

Buzzi is grossly undervalued. Buzzi is far too cheap, both relative to comparable companies and based on any reasonable cash flow-based analysis. Half of Buzzi’s EBITDA comes from a structurally superior U.S. business, and the other half comes from EU markets where the company has strong competitive positions. Simply applying U.S. comparable company or recent M&A multiples to Buzzi’s U.S. EBITDA yields well over €8 billion of enterprise value, almost Buzzi’s current market cap. In Europe, as the implications of the EU’s cap-and-trade regime have come into focus − constrained cement supply growth, leading to increased pricing power and improved margins for the cement players with scale – Buzzi’s peers have seen 57% NTM EBITDA multiple expansion. Over the same period, Buzzi’s multiple has expanded just 18%, and the company inexplicably trades at a 36% discount to peers CRH, Holcim, and Heidelberg. Moreover, Buzzi’s asset portfolio contains several underappreciated sources of value. Now fully consolidated, Buzzi’s highly profitable Brazil operation should be valued at minimum in-line with other emerging market peers. And Buzzi’s largest international asset, the company’s 33% stake in Mexico’s Corporacion Moctezuma, is easy to value since it is publicly traded with a €3.5 billion market cap. Our sum-of-the-parts valuation suggests 73% upside from current levels.

Buzzi is a leading player in an attractive industry. Across its portfolio, Buzzi is generally a top 5 player in markets that have undergone significant consolidation. The cement industry is more attractive than most other capital-intensive sectors given its high barriers to entry, rational capacity planning practices, and typical local oligopolies that result in decent pricing power and stable margins. Given the lack of substitutes for cement, we are confident that cement makers can pass along the coming costs of decarbonization, and the recent experience in Europe bodes well for the future.

Buzzi’s management is world-class. Over decades, the company’s operating and capital allocation practices have produced superior long-term performance while maintaining a conservative financial posture.

The Buzzi family controls 56% of outstanding shares, having maintained this large ownership over decades. Focused on long-term value creation, they pursue M&A and capital investments with the intent to maximize returns over decades as opposed to years. Management has executed a series of accretive and well-timed transactions, including the consolidation of Dyckerhoff, expansion in the United States, and, most recently, the opportunistic buyout of its Brazilian joint venture in 2024. Buzzi purchased a stake in Corporacion Moctezuma when its profit was less than €3 million; today, it’s over €300 million. Just this year, the company made a small but shrewd acquisition in the United Arab Emirates, taking advantage of Gulf Cement’s discounted share price to buy a controlling stake in a healthy and attractive emerging market asset.

Operationally, the company consistently achieves industry-leading EBITDA margins through disciplined cost control, continuous modernization of its asset base, and a focus on high-return markets. These outcomes reflect a culture that blends technical expertise with rigorous capital discipline. Management’s attention to detail, down to optimizing barge routes along the Mississippi, is the difference between good and industry-best. At the same time, the company has maintained one of the strongest balance sheets in the sector, moving from 2.5x net debt/EBITDA to a net cash position of more than €750 million. And it warrants mention one more time that 2024 stock-based compensation expense was zero. Buzzi management isn’t merely good, they’re among the best we’ve invested alongside.

European cement market structure is becoming increasingly attractive. Exiting 2023, investor anxiety about decarbonization, weakness in the content’s major economies, and the siren song of a booming U.S. market made investors wary of European cement exposure. Fast forward to today, European cement valuation multiples have seen a stark resurgence. Heidelberg and Vicat shares have almost doubled over the past twelve months. Holcim trades at a materially higher multiple today than before it spun off its U.S. operations. The reason is straightforward: Europe’s drive to decarbonize its cement industry has constrained supply growth and is spurring consolidation, yet demand continues to grow because cement has no real substitute. Decarbonization costs are being passed to customers, and European players, especially the larger publicly traded cement companies, are seeing firmer pricing and expanding margins due to the improving market structure.

Buzzi’s attractive international assets are underappreciated. In addition to its leading positions in the United States and Europe, Buzzi owns a collection of high-quality assets across several attractive emerging markets that provide meaningful diversification and long-term growth potential. In Brazil, Buzzi recently consolidated full ownership of Cimento Nacional, acquiring the remaining 50% stake from its joint venture partner in 2024. The transaction expanded Buzzi’s footprint to seven integrated cement plants, two grinding centers, and six terminals with more than seven million tons of capacity. The business operates in a market with favorable structural dynamics — low per-capita cement consumption, robust infrastructure needs, and a growing middle class — and has achieved EBITDA margins in the low 30% range. In Mexico, Buzzi owns a 33% stake in Corporación Moctezuma, a publicly-listed Mexican cement producer with three modern integrated plants and industry-leading margins exceeding 40%. The stake is currently worth €1.2 billion and dates back four decades. Moctezuma operates within a highly consolidated four-player market that has demonstrated rational pricing and consistent profitability. The company’s stakes in two Algerian plants provide profitable exposure to a concentrated North African market, while its recent acquisition of a 58% stake in Gulf Cement in the UAE offers an enviable platform in a region with strong long-term construction demand. Finally, Buzzi owns two highly attractive plants in Russia. While the company has lost managerial control of its Russian operations since the onset of hostilities in Ukraine, a risk that has led most investors to heavily discount its financial contribution, any geopolitical normalization could unlock at least a half billion Euro of value overnight.

Buzzi benefits from industry tailwinds. Despite a strong recent run, we believe the cement market will remain healthy. Underlying fundamentals point to a volume recovery in the United States. Undersupply combined with a stronger U.S. residential sector in 2026 given likely interest rate declines will likely support prices. In Europe, 1H 2025 metrics have demonstrated growth in most of its markets, as healthy pricing continues to lift margins as decarbonization regulations stymie capacity additions across the continent. Notably, Buzzi stands to gain disproportionately relative to its peers as the German market (~16% of revenue) finally shows signs of recovery in 2H 2025.

We see numerous paths to value creation. We believe Buzzi can generate over €2.2 billion of excess cash through 2030, providing the company significant flexibility to pursue a number of value-enhancing alternatives, including accelerating decarbonization investment when the time is right, issuing a special dividend to appease investor desires for increased capital returns, and pursuing opportunistic asset acquisitions.

Read the full report here by Kerrisdale Capital