>50% pullback in the stock over an earnings miss creates an absurd mispricing. $500M buyback announced, supported by very healthy FCF, fortress balance sheet, and open-ended growth story

- Expected Return: 163.8%

- Timeframe: 6 Months To 1 Year

After 50% Pullback, Eyeing 163% Upside 1")

Thesis

Stride Inc (NYSE:LRN) is an education services/ technology company that operates tuition-free public schools on behalf of charter schools and local school districts. On October 28, 2025, Stride reported its fiscal first-quarter earnings. The stock closed before the call at $153 and ended the week down ~55% to $68. The primary reason for the dramatic sell-off was Stride’s weak enrollment guidance, which was affected by technical challenges during the implementation of a new Learning Management System (LMS).

Despite the technical challenges, Stride still managed to grow enrollment by 11% in the quarter and guided to 5% revenue growth for the whole year. Stride now trades at a Price/Sales of 1.2x, a P/E of 8.5x, and a TTM FCF/EV of 13%. We believe several technical factors exacerbated the sell-off, creating a spectacular setup in the stock. Perhaps most importantly, Stride’s business is inflecting with unprecedented demand from parents and students. Absent the IT mishap in Q126, they were headed for another year of record enrollments, revenue, and cash flow. After the sell-off, the company announced a $500mm buyback (its first buyback ever), which should provide a decent floor for the stock. As Stride recovers from this episode, it’s not unreasonable to expect the stock to return to its all-time highs, making the current entry price highly asymmetric.

The Set Up Going into Q126

To understand why the market so overreacted to the Q126 earnings miss, it’s important to provide some context from Stride’s recent history. Of course, when it comes to trying to figure out the drivers behind a big stock move, the only thing that is known with certainty is that there were more sellers than buyers. However, the sell-off was so bizarre relative to the bad news that it’s worth analyzing what might have made it worse:

- On August 5th, 2025, Stride reported record earnings for their fiscal year 2025 (their fiscal year ends in June). Because Stride’s revenue is dependent on its student count for the upcoming school year (set on the “count date” at the end of September), the company never provides forward guidance. Instead, they wait for their FYQ1 call, which they usually report in late October. However, back in August, the CEO felt that the inbound funnel was so strong that he was willing to give soft guidance: “that we will once again achieve double-digit enrollment growth this fall.” For those who have been following the company for years, this was highly unusual, given the precedent of not giving guidance. On the heels of these remarks, the stock reached an all-time high and traded >$170/share in the weeks following the call. This strength going into the Q1 earnings, fueled by momentum investors, quickly reversed when earnings disappointed, providing fuel to the fire.

After 50% Pullback, Eyeing 163% Upside 2")

- Stride has been the target of repeated short sellers over the years. Betting against for-profit education companies has been a decent trade, but shorts continually miss the nuance around compulsory K-12 education versus post-secondary for-profit schools. The most significant difference concerns funding: >90% of K-12 funding is allocated at the state and district levels. In other words, there’s limited “stroke of the pen” risk that funding will be canceled through a legislative change, which has been the Achilles heel of post-secondary for-profit education companies. Each Stride school has a contract, usually 3-5 years in length, with a district or charter school, and an independent board oversees the school. This dramatically mitigates funding risk because each school is independent.

- As relates to the setup going into Q126, in April of 2025, news broke that a school in New Mexico (4,000 students out of a total of 247,000) had cancelled its contract and filed a lawsuit claiming, among other things, that Stride had failed to provide sufficient student-to-teacher ratios. Stride counter-sued, given that the plaintiff in the case applied to Stride for a job and was rejected. Within months of the cancellation, Stride started a new school in the state and migrated most of the students from the previous school. This context is crucial because the missed guidance was undoubtedly interpreted as proof of broader/existential issues with the business model. However, the transition to the new LMS was never even discussed by management, let alone the focus of short sellers.

- The negative surprise came after market hours on October 28th, leaving mutual funds three days to harvest tax losses by their October 31st deadline (everyone else has until Dec. 31st).

- The topline guidance they gave was confusing and poorly contextualized. Stride reported Q126 revenue growth of 13% but only guided for full-year revenue growth of 5%. Management also said that they did not anticipate growing their enrollments during the 25/26 school year. In the context of the IT challenges and the swoon in the stock price, the market assumed that Stride was still hemorrhaging students and guiding for continued losses through the year. However, this is not the correct interpretation of the guidance. To understand why, we need to analyze their results from last year. Last year, Stride grew in-year enrollments from FYQ1-Q3: In fact, last year was so strong that Stride was able to increase its enrollments throughout the school year, even though there is only one “count date” in September. This year, however, even if enrollments stay flat, the rate of revenue growth will decrease as they anniversary the strong comps from last year. This might sound like hair splitting, but it’s critical for understanding why the market went into full panic mode. Enrollments are the most important leading indicator for this business. Even if the company guided for declining enrollments, the >50% sell-off would be extreme. But the reality is that enrollments are stable and likely to start growing again next year.

After 50% Pullback, Eyeing 163% Upside 3")

What’s the basis for optimism that they can recover from this?

As mentioned above, the main reason for the disappointment was the company’s decision to install a new learning and technology platform. The new platform was glitchy, resulting in approximately 10,000 -15,000 fewer enrollments. James Rhyu, the CEO, provided the following overview:

“We indicated in August that we believe we would grow enrollment between 10% to 15%. And while we achieved enrollment growth in that range, we still fell short of our internal expectations...we invested in upgrading our learning and technology platforms with third-party industry-leading platforms... However, the implementations did not go as smoothly as we anticipated...this poor customer experience has resulted in some higher withdrawal rates and lower conversion rates than we expected... that is to limit enrollment growth while we improve our execution. We estimate that the combination of these factors resulted in approximately 10,000 to 15,000 fewer enrollments than we otherwise could have achieved...”

In the long run, this was the right upgrade, but clearly poorly executed. In addition, management was cautious on the call and clearly didn't go far enough to convince the investor community that all of the technical issues had been resolved.

If we’re setting odds on how long it will take to fix the issues, we feel good about taking the “under.” The LMS they chose is called Canvas, which is the leading LMS in North America (6,000 schools and 30 mm users). They’ll figure this out, and it sounds like they have made a lot of progress. On November 5th, BMO Capital Markets held a virtual NDR with management to discuss what is going on:

After 50% Pullback, Eyeing 163% Upside 4")

This isn’t existential. It’s not binary. It’s really just an execution story with off-the-shelf technology and an already proven business model.

What makes this a good business and challenging for Competitors?

Running virtual public schools is not easy (remember how bad COVID was!). The only other national competitor is Connections, which is owned by Pearson (Stride is >2x the size). There are non-trivial regulatory challenges (tracking attendance, providing services for disabled students, etc.), technical considerations (Stride spends $80mm in CapEx/year), and staffing issues (persistent teacher shortages). On the other hand, the business is stable, recession-resistant, and customers (the states) always pay. Lastly, this is a gigantic market that is inflecting with only ~750,000 out of 50 mm K-12 students in the US enrolled in virtual programs. Pre Covid this was barely a mid-singledigit grower, but now there is very strong demand, which increases every year, as seen by survey data from parents:

After 50% Pullback, Eyeing 163% Upside 5")

Until this misstep in Q126, Stride had been executing flawlessly on this business plan. In fact, they gave 5-year guidance in 2023, which they already achieved in FY2025:

After 50% Pullback, Eyeing 163% Upside 6")

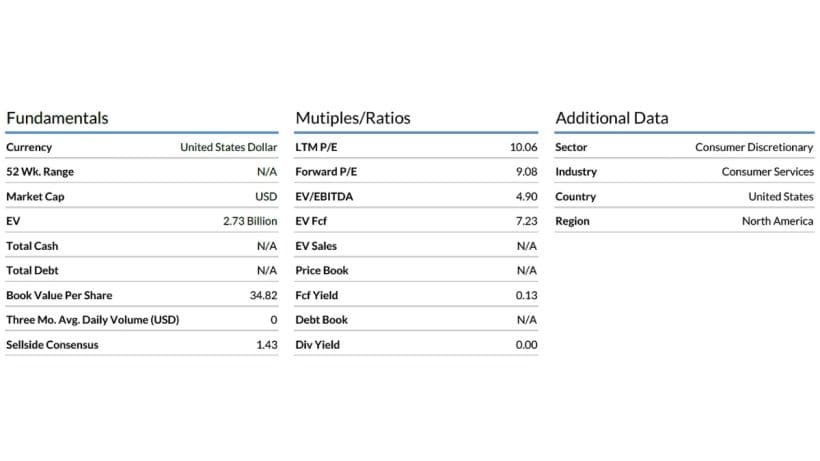

After the big sell-off, the valuation is not demanding:

After 50% Pullback, Eyeing 163% Upside 7")

Stride is trading like a business that has serious questions about its viability and future. But the reality is that the company has never been in a better position. The current trading multiple is a gift for anyone that can see through the fear and appreciate the inevitability of the growth.

Conclusion

It doesn’t take a massive leap of faith to expect Stride to return to its previous growth trajectory. They’ll likely start showing green shoots as the year progresses. The panic selling following an epic self-goal has severely mispriced the equity. It’s a value investor's dream. How often can you find a cheap stock, fortress balance sheet, recession resistant business, spectacular free cash flow, and an open-ended growth story. It really doesn’t get better than this. Don’t take our word for it: Management has already announced that they will be repurchasing their shares in size for the first time in the history of the company.

Disclaimer: The author's fund had a position in this security at the time of posting and may trade in and out of this position without informing the SumZero community.

About Adam Buckstein

I've been working on the buy side for 18 years. I launched ASB Partners in 2022. I try to find those rare companies that are cheap, have growing earnings, and are durable.