Dynamo Software’s 4th Annual Limited Partner Research reveals insights that will shape LP strategies and GP priorities for the year ahead.

Critical Market Intelligence Inside:

- Regional Capital Migration: Europe and Asia now command investment flows previously concentrated in North America—a seismic shift with immediate strategic implications.

- Direct Investment Surge: LPs are bypassing traditional structures at unprecedented rates, creating new competitive dynamics.

- Cryptocurrency Allocations: Institutional adoption accelerates beyond early predictions, demanding immediate attention from sophisticated managers.

- Financial Workflow Analysis: First-ever satisfaction benchmarks reveal operational inefficiencies costing firms significant LP confidence.

Why This Report Matters Now

Over 90 LPs provided candid insights into their priorities, pain points, and allocation strategies. The year-over-year analysis exposes trends that separate market leaders from those falling behind.

General Partners who understand these shifts first will secure the strongest LP relationships. Those who don't risk being left out of the next funding cycle.

Executive Summary

Dynamo Software maintains a commitment to delivering valuable insights to the alternative investment community by publishing quarterly primary research reports. These reports draw on proprietary surveys broadly distributed to Dynamo clients, non-clients, thought leaders, and industry stakeholders. Now in its fourth year, the 2025 Limited Partner (LP) survey findings are in, and reveal a market teetering between steadfast strategies and budding trends.

Are LPs and Asset Allocators sticking with tradition, or are they forging new paths?

This year’s insights show direct investments making a strong increase to 48% (up from 32% in 2024), underscoring a renewed appeal, while secondaries saw a slight dip to 30%, (down from 36% in 2024). hinting at shifting preferences. Meanwhile, cryptocurrencies are capturing growing interest, climbing to 9% from 8% last year—a subtle, yet noteworthy, rebound. This comes after a dramatic slump, where crypto interest plunged from 13% in 2022 to just 3% in 2023, Investor curiosity seems to be renewing. AI remains a key focus for ongoing exploration and analysis, paired with a strong emphasis on tech priorities and budget planning.

This report explores these trends and more, presenting a dynamic snapshot of the investment landscape. From the stability seen in traditional pathways to the cautious, yet growing, experimentation in emerging asset classes, the data tells a story of evolution and resilience.

The 2025 findings are, as always, compared to data from previous years where applicable, and include a deeper analysis of each firm’s performance across five key areas of their investment workflow. The potential implications of each trend are profound, and will be explored on the following pages.

A Four-Year Retrospect | What’s Changed & What Hasn’t

Here are the year-over-year comparisons from the 2025 findings compared to previous years’ primary research data:

Investment Allocations

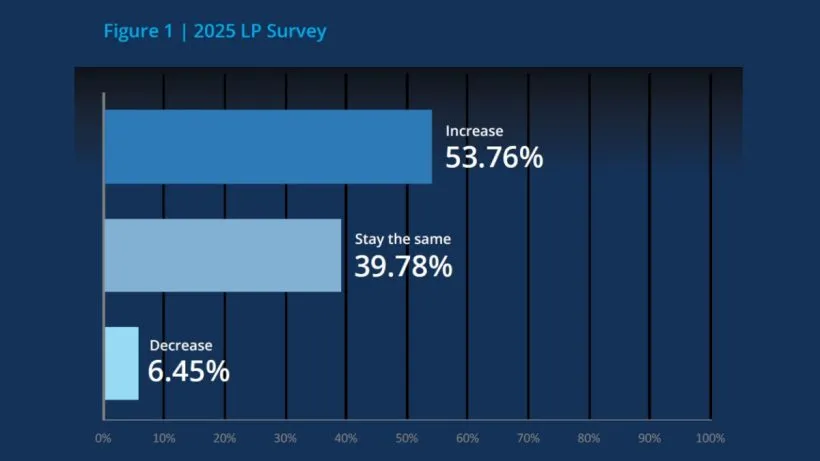

- LPs increasing allocations to alternatives edged up to 54%, a modest rise from 52% in 2024, although slightly lower than the 56% seen in 2023. Consistently since 2022, approximately half of LPs each year have indicated plans to increase Alts allocations.

- Co-investments climbed to 56% from last year’s 51%, underscoring a growing appetite for more direct engagement, even if still trailing the 61% peak from 2023.

- Direct investments stood firm at 48%, marking the highest level over four years, while secondaries dipped slightly to 30% compared to 32% in 2024. Meanwhile, reliance on fund managers fell to 70%, continuing a steady shift year-over-year, (72% in 2024, 86% in 2023, and 77% in 2022), perhaps signaling that LPs are looking for greater control and flexibility within their portfolios.

- For four years running, generative AI has ranked the top area in which LPs want their tech-focused fund managers to invest. These movements reflect a steady commitment to established strategies alongside a measured adaptation to changing market dynamics.

Geographical Preferences

- North America, while still dominant, saw a significant decline to 48%, down from a peak of 78% in 2024.

- Europe experienced a remarkable surge in focus, climbing to 27% from just 10% last year—the highest level recorded to date. Asia also gained significant traction, rising to 23% from 10% in 2024.

- Meanwhile, interest in regions such as the Middle East/Africa and Australia/ New Zealand remains minimal, highlighting the continued preference for established markets.

These trends emphasize LPs’ growing interest in diversifying geographically while balancing risk and opportunity.

Read the full report here by Dynamo Software