Amova Asset Management’s latest market outlook from Yeu Huan Lai, Head of Asian Equity, and Kenneth Tang, Senior Portfolio Manager. The piece, “ASEAN’s Promising Outlook,” explains why ASEAN is emerging as one of the most attractive regions for investors as global capital and supply chains continue to shift away from China.

Key highlights include:

- Tariff tailwind: U.S. import tariffs on ASEAN goods average 19 to 20 percent, compared with 30 percent on China and 50 percent on India and Brazil. This gives countries like Vietnam, Thailand, and Malaysia a major competitive edge.

- Weaker-dollar boost: As the Federal Reserve moves toward rate cuts, capital could return to higher-yielding emerging markets, supporting a rebound in ASEAN equities.

- Structural growth drivers: Two enduring engines, industrial development and consumer expansion, are reshaping the region’s economy.

- Investment positioning: The team sees Singapore, Indonesia, and Vietnam as high-conviction markets with strong policy support and domestic demand.

ASEAN is poised for robust growth, supported by expectations for a softer US dollar, favourable interest rate dynamics and a shift in global supply chains away from China. The region benefits from lower US tariffs, competitive labour costs and rising foreign investment—particularly in manufacturing and technology. Amid evolving macroeconomic and policy backdrops, we believe that ASEAN presents investors with selective, long-term opportunities.

ASEAN seen benefitting from a softer dollar, lower US rates

Several ASEAN economies, particularly Indonesia, the Philippines, and Vietnam, have historically relied on external dollar funding to support their financial systems and economic growth. In this context, a weaker US currency tends to ease funding pressures, reduce debt servicing costs, and improve liquidity conditions, all of which are supportive of local equity markets.

Looking ahead, the dollar is expected to remain under pressure due to a combination of slowing US economic growth, a dovish pivot by the Federal Reserve (Fed), and narrowing interest rate differentials with emerging markets. As inflation moderates and the Fed shifts toward rate cuts, capital could flow back into higher-yielding emerging markets, reinforcing the tailwind for ASEAN equities.

Empirical data from Bloomberg shows that ASEAN stock markets have generally performed well during periods of dollar depreciation (Chart 1), reflecting the positive impact of currency dynamics on investor sentiment and capital flows into the region. This relationship underscores the importance of global monetary trends in shaping ASEAN’s investment landscape.

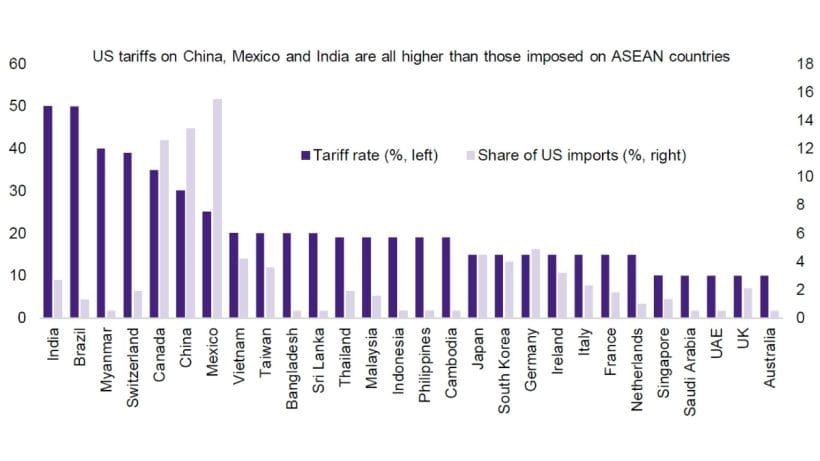

US tariff rates favour ASEAN relative to other key economies

ASEAN holds a clear tariff advantage in the global trade landscape, particularly when compared to major manufacturing hubs like China, Mexico and India (Chart 2). US tariffs on imports from India and Brazil are a steep 50%, while China faces 30%, and Mexico 25%. In contrast, ASEAN countries such as Vietnam, Thailand, Malaysia, Indonesia and the Philippines face significantly lower tariffs, ranging from 19% to 20%, making them more cost-effective partners for global supply chains.

This favourable tariff positioning is further amplified by the region’s competitive labour costs, expanding workforce, and rich resource base. Vietnam, Malaysia, and Thailand are especially well-placed to benefit, notably in the electronics and electrical sectors, where these structural advantages converge.

Supply chains will continue shifting towards ASEAN

The shift in global supply chains from China to ASEAN has become a defining structural trend in international trade and investment. Initially catalysed by the first Trump administration’s trade policies and further accelerated by the disruptions of COVID-19, this realignment has continued under the second Trump administration, with no signs of reversal (Chart 3).

ASEAN’s enduring advantages—a large workforce, cost competitiveness, strategic location and improving infrastructure—have made it a preferred destination for diversified manufacturing and investment.

As a result, ASEAN’s share of US imports and global foreign direct investment (FDI) inflows has now surpassed that of China, according to data from CEIC and UNCTAD. This milestone underscores the region’s rising importance in global supply chains and its growing role as a manufacturing and export powerhouse.

ASEAN’s twin engines for growth and investment opportunities

ASEAN’s long-term investment appeal is anchored by two powerful structural drivers—industrial development and consumer growth—that are reshaping the region’s economic landscape.

Industrial development: building the backbone of ASEAN’s future

Industrial development is a cornerstone of ASEAN’s growth story, driven by structural transformations, deeper economic integration, and the rise of advanced manufacturing.

The region is rapidly positioning itself at the forefront of the global energy transition, with increasing investments in renewable energy and the electric vehicle (EV) ecosystem. Simultaneously, ASEAN is embracing the digital revolution, with data infrastructure and artificial intelligence (AI) becoming key enablers of productivity and innovation.

Economic integration across member states is also accelerating, supported by expanding logistics networks, modern transportation systems, and the evolution of financial services.

In advanced manufacturing, ASEAN countries, particularly Malaysia, Vietnam, and Thailand, are climbing the value chain through participation in the semiconductor ecosystem, automation technologies, and Industry 4.0 capabilities.

Consumer growth: the rise of the ASEAN middle class

Alongside industrial progress, ASEAN is experiencing a powerful consumer transformation, underpinned by its demographic dividend. By 2030, ASEAN is expected to host approximately 415 million middle-class consumers out of a total population of 720 million, according to HSBC and Statista.

This demographic momentum, characterised by a young, urbanising, and increasingly affluent population, provides a durable foundation for long-term consumer growth and makes ASEAN one of the most compelling consumption stories globally.

With a young, expanding population and rising income levels, the region is seeing a surge in consumption and digital adoption. Digitisation is reshaping how people live, shop, and access services, with new media, digital healthcare, e-commerce, and fintech driving innovation and inclusion.

As disposable incomes grow, consumers are upgrading their preferences, seeking premium products, better healthcare, and enhanced leisure experiences. This shift is fuelling demand in sectors such as hospitality, wellness, and lifestyle services.

At the same time, fast-growing local brands in consumer foods and retail are capturing market share and expanding across borders.

Politics in the headlines

While ASEAN’s structural growth narrative is compelling, political developments in key markets like Thailand and Indonesia introduce a layer of uncertainty. Politics in these markets underscore the importance of monitoring policy continuity when the region is viewed from a broader perspective.

Thailand: interim stability with an eye on elections

Thailand has entered a transitional phase with the formation of an interim government led by Prime Minister Anutin Charnvirakul of the Bhumjaithai Party. This administration is expected to hold office until national elections are conducted within the next four months.

Early signs are encouraging, with cabinet appointments largely seen as technocratic and credible, helping to stabilise sentiment in the near term. The government’s policy agenda is focused on boosting domestic consumption, which could provide short-term economic support.

However, longer-term political stability remains crucial for sustaining investor confidence, ensuring policy continuity and unlocking Thailand’s growth potential.

Indonesia: policy recalibration amid political noise

In Indonesia, President Prabowo Subianto has taken steps to ease political tensions by making concessions aimed at curbing excesses among lawmakers. These moves have helped calm market sentiment and restore a degree of investor confidence.

However, the recent replacement of the Indonesian finance minister, while intended to reinvigorate the growth agenda, remains a key focal point, particularly in terms of fiscal discipline and policy continuity.

On the macro front, Indonesia stands to benefit from a weaker dollar and potential rate cuts by the Fed, creating room for domestic monetary easing amid stable inflation and subdued growth. A major fiscal initiative—the rollout of a free nutritious meal program—is expected to provide a short-term boost to consumption, with central kitchens ramping up by year-end.

Still, longer-term challenges such as weak household spending and persistent income inequality will require sustained and targeted policy attention.

Our outlook by country

ASEAN countries offer a diverse set of opportunities with varying degrees of macro resilience. We focus on what in our view are the “high-conviction” markets of Singapore, Indonesia and Vietnam; we also explain our views on what we see as the “neutral” markets of the Philippines, Malaysia and Thailand.

High-conviction markets: Singapore, Indonesia and Vietnam

Singapore: government support for equity market

Singapore has been the best-performing equity market in ASEAN over the past three years, supported by solid industry fundamentals and proactive government measures to bolster the local market.

We continue to view Singapore as a quality, high-yielding market, while we have taken profits and rotated into deeper value opportunities. Our focus is now on undervalued names with restructuring catalysts and mid-cap stocks that could benefit from ongoing policy support and targeted market initiatives.

Indonesia: supported by rates and policy shift

Indonesia also benefits from the same supportive macro backdrop of easing US rates and a softer dollar.

Recent political developments, including concessions by President Prabowo Subianto to curb legislative excesses, have helped calm investor sentiment. However, the replacement of the Finance Minister introduces a degree of uncertainty, particularly around fiscal discipline and budget execution.

We remain constructive, with preferred exposures in food manufacturers poised to benefit from the rollout of the free nutritious meals program, materials linked to the electric vehicle (EV) ecosystem, and property and cement companies that stand to gain from lower interest rates and infrastructure spending.

Vietnam: export-led growth and reform momentum

Vietnam continues to be a prime beneficiary of global supply chain diversification away from China thanks to its geographic proximity, competitive labour costs, and improving infrastructure. The country’s new leadership is pushing forward with structural reforms and large-scale infrastructure investment, reinforcing its attractiveness to foreign investors.

We favour retailers and property developers as proxies for rising domestic consumption, infrastructure owners and industrial park operators capturing manufacturing relocation inflows, and local champions in IT services and food production. These exposures align with both Vietnam’s export-driven growth and its evolving domestic economy.

Neutral markets: Philippines, Malaysia and Thailand

Philippines: rate and renewable play

The Philippines stands out as a key beneficiary of a weaker US dollar and lower US interest rates, which ease external funding pressures and support domestic liquidity. Economic growth remains resilient, underpinned by healthy domestic demand and a stable consumer base.

Within this environment, we favour property developers that benefit from lower borrowing costs and robust retail activity, solar energy producers aligned with the country’s green transition agenda, and banks offering attractive dividend yields. These exposures position us to capture both cyclical tailwinds and structural growth themes.

Malaysia: selective exposure in data and tech

Malaysia’s market profile is defensive, and while the global macro backdrop favours ASEAN, sustained outperformance is less likely.

We remain selective, with a focus on property and construction proxies benefiting from the rapid buildout of data centres, and semiconductor supply chain companies positioned for cyclical recovery. These exposures offer targeted access to structural tech themes without broad market exposure.

Thailand: value opportunity amid stabilisation

Thailand’s market has stabilised at historically attractive valuations, supported by improved political visibility and fiscal stimulus. The formation of an interim government under Prime Minister Anutin Charnvirakul has reduced near-term uncertainty, while stimulus measures are expected to support consumption and infrastructure activity.

We favour construction and consumption-related names that stand to benefit from fiscal support, as well as hospital operators with resilient demand and strong bottom-up growth drivers.

Conclusion

ASEAN’s ascent is being shaped by a convergence of macroeconomic tailwinds, trade advantages and industrial and consumer transformation. As global capital focuses on emerging markets, the region’s competitive positioning—reinforced by supply chain realignment and tariff benefits—makes it a compelling destination for long-term investment. Political developments in key markets like Thailand and Indonesia should be monitored closely. However, with various opportunities across markets, we believe that ASEAN offers a dynamic and resilient landscape for investors seeking growth and diversification.