David Einhorn’s Q4 2025 letter to Greenlight Capital investors. See the full letter at the bottom of this post in PDF format.

Dear Partner:

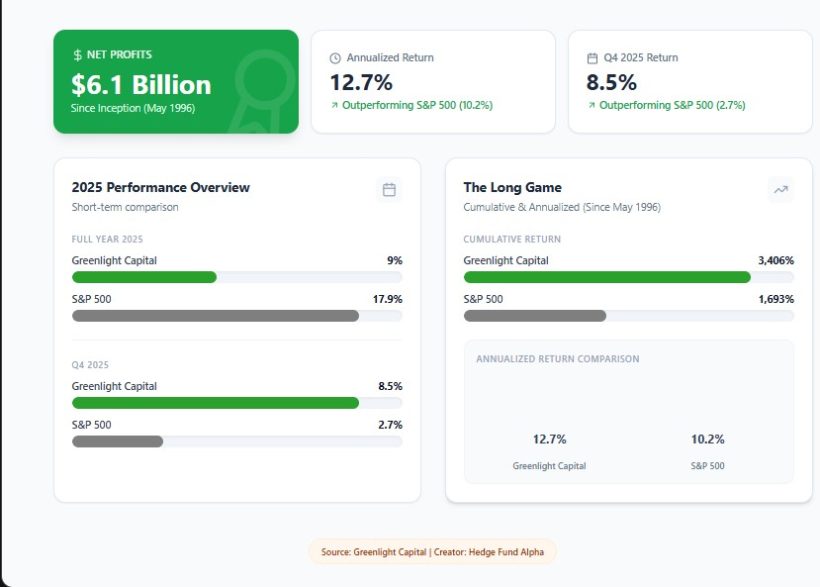

The Greenlight Capital funds (the “Partnerships”) returned 9.0% in 2025, net of fees and expenses, compared to 17.9% for the S&P 500 index. In the fourth quarter, the Partnerships returned 8.5%, while the S&P 500 index returned 2.7%. Since the inception of Greenlight Capital in May 1996, the Partnerships have returned 3,406% cumulatively or 12.7% annualized, both net of fees and expenses. Over the same period, the S&P 500 index has returned 1,693% or 10.2% annualized. Greenlight’s investors have earned $6.1 billion, net of fees and expenses, since inception.

Many have reached out to express concern over New York City’s new mayor. We confess to sharing some of that apprehension. Afterall, we are not Democratic Socialists. However, when we hear President Trump say things like, “I, as President of the United States, am calling for a one year cap on Credit Card Interest Rates of 10%,” and “We [the government] should take stakes in companies when people need something,” perhaps concerns about socialism should extend beyond the five boroughs. We wonder if in a few years there will be a trivia game called, “Who said it: Trump or Mamdani?”

As we reflect on these uncertainties and think about our investment strategy and portfolio construction, our goal is to build a bottom-up portfolio of equity longs that are absolutely cheap and, where possible, misunderstood, paired with a portfolio of equity shorts that are overvalued, poorly understood and deteriorating. We complement this with a macro book, partly designed to hedge macro risks and partly to capture macro insights. We may also use index positions to adjust overall exposure to align with our top-down thinking. In a typical year, we would expect most of our performance to come from the long-short book, with a small contribution from macro.

For 2025, we made all our return and alpha in the macro portfolio, as shown in the table below:

Read more hedge fund letters here

Read more hedge fund letters here

All told, by our calculation we generated 14.5% of alpha, which on its own is a perfectly acceptable result. Macro investing continued to shine, even as the long-short portfolio lagged.

We did have a few notable successes in the long portfolio this year. The highlights were:

- Brighthouse Financial (BHF): After years of frustration, the company put itself up for sale, which led to a sale process that culminated in a buyer agreeing to purchase the company. While the valuation at less than two-thirds of book value is not exciting, it does provide us with a reasonable exit from a challenged situation. We likely will write more about this after we do, in fact, exit.

- The Fluor/NuScale Power stub (FLR/SMR): FLR owned the majority of SMR, which essentially went parabolic. We anticipated FLR would dispose of its SMR stake and use the proceeds to repurchase its own shares, and this is exactly what is happening. The result of the heavy sales by FLR combined with SMR’s very speculative valuation has led to a sharp decline in SMR, while FLR has been largely stable. The result is that the value of our stub position increased substantially.

- Victoria’s Secret (VSCO): A prior management team nearly destroyed one of the most well-known brands in the world. To be more politically correct, it got rid of sexy and eliminated its world-famous fashion show. New management is reversing those decisions and the brand is beginning to recover. The stock, which was all but left for dead, is beginning to reflect the brand’s recovery.

- Teva Pharmaceuticals (TEVA): The company continued to deliver rapid growth in its patented branded portfolio, with results consistently exceeding expectations. The market began to reflect this progress only after policy headwinds eased, including a negotiated pricing agreement with the Centers for Medicare & Medicaid Services for TEVA’s drug Austedo beginning in 2027. These developments more than offset muted performance in the generics business and highlight the progress TEVA has made in its transition to a branded pharmaceutical company.

Many of the remaining large names in our long portfolio suffered for the reasons described above, though thankfully we didn’t suffer any major meltdowns. The closest would be Lanxess (Germany: LXS), which suffered a cyclical decline and a loss of market share to China in one of its three segments. We believe that other cyclical names that hurt us, including CNH Industrial (CNH), CNR, Graphic Packaging (GPK), Solvay (Belgium: SOLB) and United Parks & Resorts (PRKS) will likely recover in due course. Green Brick Partners (GRBK) also faced strong cyclical headwinds, but the stock still managed to gain 11%, while most other homebuilders were flat or down.

Read more hedge fund letters here

We initiated several small long positions during the quarter.

Antero Resources (AR) is a natural gas exploration and production company with operations in the Marcellus Shale in West Virginia. The company operates at the low end of the cost curve and has a stable production profile with significant acreage. In December, AR announced an acquisition that we believe will be accretive to earnings and will extend the runway of its future production. We acquired our shares at an average price of $33.92, implying an 11% free cash flow yield. AR shares ended the quarter at $34.46.

Deckers Outdoor (DECK) designs, markets and distributes footwear and apparel, including the Hoka (running shoes) and UGG (casual luxury cold-weather shoes) brands. DECK stock declined after it posted disappointing results early in 2025, which were impacted by tariff uncertainty, a warehouse transition in Europe, and warm weather during the early part of the UGG selling season. As Hoka expands internationally, we expect growth to re-accelerate and believe the company will use its strong balance sheet, including net cash equal to roughly 9% of its market capitalization, to increase the pace of stock repurchases. We acquired our shares at an average price of $85.49. DECK ended the quarter at $103.67.

Global Payments (GPN) is a payments processor serving mostly small and mid-size merchants in the U.S. After exiting the position in 2023 at $108.61, we re-acquired shares at an average price of $77.85. In 2024, the company surprised investors by announcing a two-step transaction to sell its issuer processing business and acquire Worldpay. While the market did not like the announcement, we understand the logic behind it and the likely synergies it should create. Pro forma, GPN is targeting $5 billion of free cash flow in 2028, which equates to nearly 25% of the current pro forma combined market capitalization. Once the Worldpay transaction closes, we expect GPN’s consistent history of organic growth and its commitment to return nearly $7 billion to shareholders (one-third of the market cap) over the next two years to be better appreciated by the market and to provide runway for the shares to re-rate higher. GPN ended the quarter at $77.40.

Henry Schein (HSIC) is a leading distributor of dental and medical products. Since COVID, cost inefficiencies have led to margin erosion that we believe is now set to be addressed by newly installed activist board members and a pending CEO change. Should the company be successful in correcting these issues and improving its e-commerce capabilities, we expect margin improvement that will lead to significant free cash flow generation and share buybacks. We purchased our shares at an average price of $68.11. HSIC shares ended the quarter at $75.58.

Spectrum Brands Holdings (SPB) is a consumer products company focused on pet care, home & garden, and home & personal care (HPC). The company faced challenges in 2025 that now appear largely behind it, and we expect SPB to return to growth this year. There is also potential for the company to realize proceeds from a divestiture of its HPC segment, which we believe the market currently values at zero. In the meantime, the company is returning capital through sizeable share repurchases. We acquired our shares at an average price of $52.75, and SPB ended the quarter at $59.08.

Warner Bros. Discovery (WBD) is a media conglomerate that owns HBO, the Warner Bros. Studio and content library, and various linear cable networks. We acquired our shares at an average price of $22.66 after Paramount Skydance (PSKY) bid $23.50 for the company, as we expected additional bidders to emerge. Shortly thereafter, Netflix submitted a $27.75 bid for WBD’s streaming and studio assets, prompting PSKY to raise its offer to $30 per share. We believe a sale in the low- to mid-$30s is the most likely outcome. WBD shares ended the quarter at $28.82.

Read more hedge fund letters here

At year-end, the largest disclosed long positions in the Partnerships were Brighthouse Financial, Core Natural Resources, Fluor, Green Brick Partners and Solvay. The Partnerships had an average exposure of 89% long and 50% short.

“You measure the size of the accomplishment by the obstacles you had to overcome to reach your goals.” - Booker T. Washington

Best Regards,

Greenlight Capital