What is Pinterest?

Pinterest is a visual discovery and bookmarking tool. It has created a niche on its own: we see it alongside Twitter, Instagram, Snapchat and LinkedIn, in terms of having created a unique product with social aspects.

Q1 hedge fund letters, conference, scoops etc

Pinterest allows users to collect and save images within categorized boards, similar to the way that Slack discussions are organized into topic-specific channels. (We reviewed the Slack IPO filing here).

Pinterest is considered “social” because it allows users to follow people or specific boards based on their interests, and this aspirational “pinning” is fun, easy, and sometimes addictive.

Pinterest is a unique advertising business: not only is there high intent (i.e. collecting ideas for a bathroom remodel), but its various ad types (i.e. carousel, ecommerce) are covertly placed within the rest of the pinned images. In addition to Pinterest’s ads being hard to avoid, the ads are routinely pinned by users, thus increasing their reach. (We haven’t found many other platforms where this occurs).

Pinterest is also expanding its ecommerce capabilities, including the discovery of products from photos taken by users.

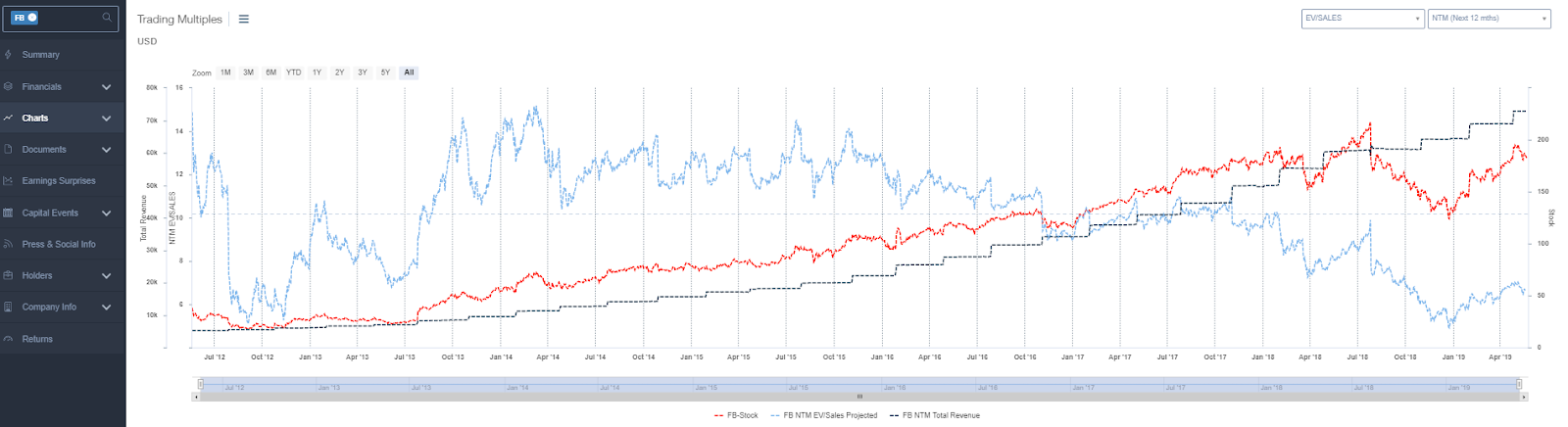

In our view, Pinterest is a unique property in the early stages of monetization (esp. international), similar to where Facebook was after its IPO in 2012. Unlike Facebook, however, there are really no questions around the monetization potential. (Mobile was a big question for Facebook). We are very optimistic on Pinterest in the long term, in contrast to the large unknowns around AVs, as we discussed in our Uber and Lyft AV review).

Product Overview

Below is what the Pinterest homepage for the desktop application looks like for one of our team members. The content suggested for browsing is tailored to several existing boards. Also note the carousel ads from blue chip advertisers (Home Depot and Walmart).

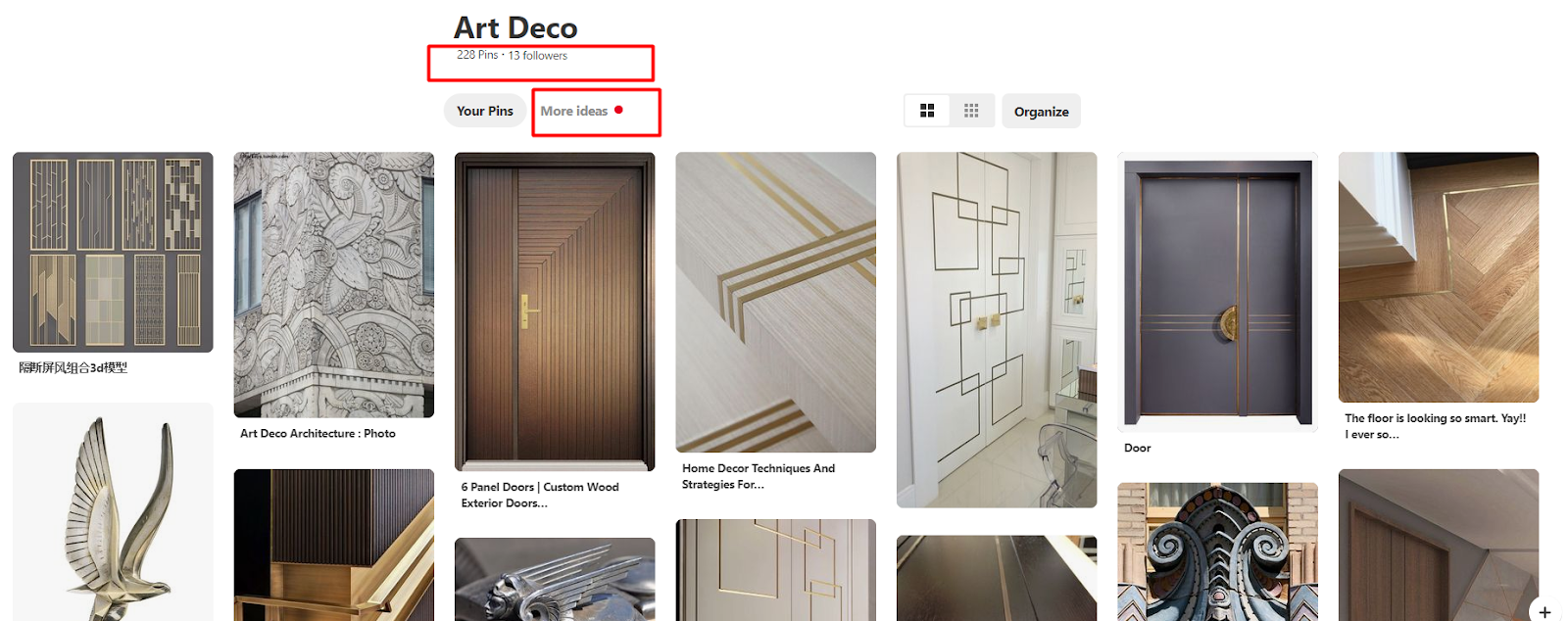

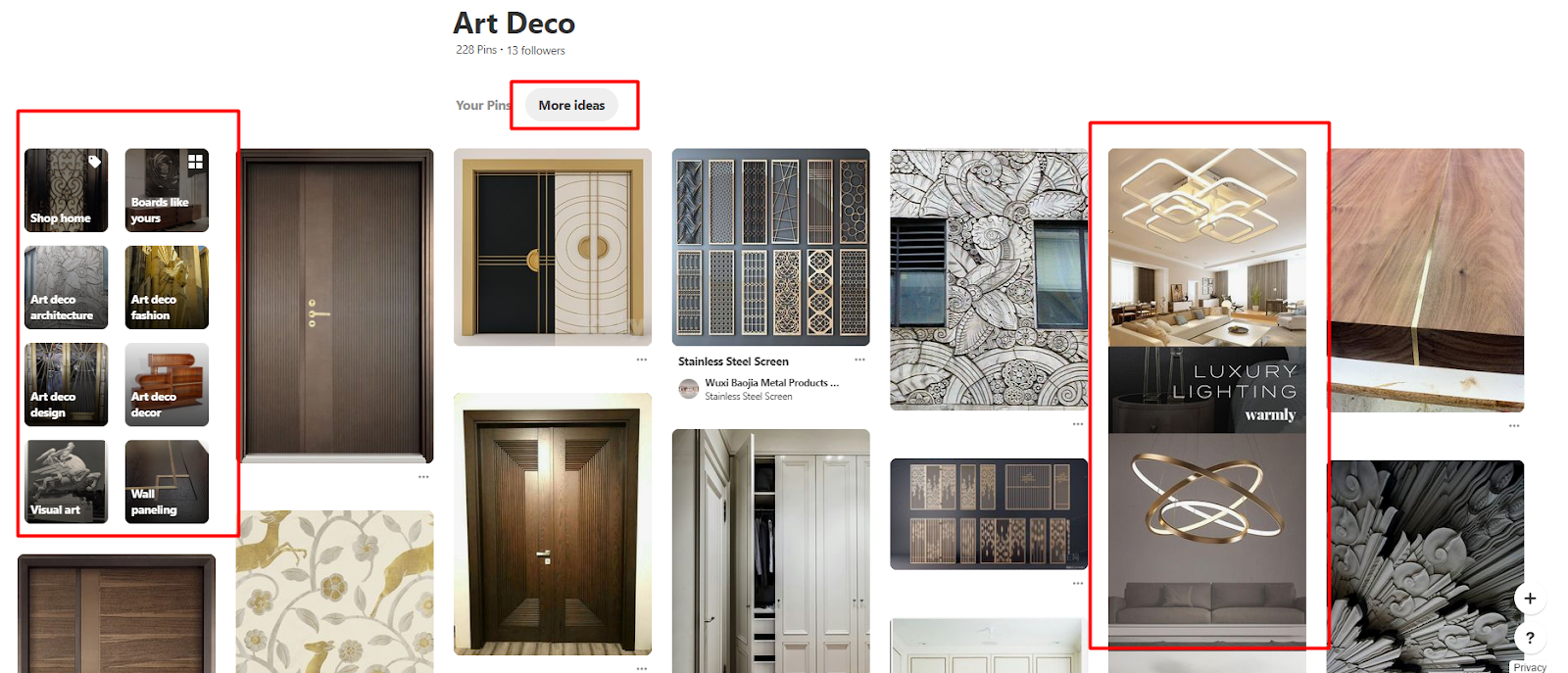

Opening up a board (called Art Deco in this case), reveals the saved pins and invites the user to explore more content of the same kind algorithmically. Users can also search textually. We can also see that this board has 13 followers who will see any new content as it’s added.

Clicking on “More Ideas,” we see an invite to shop, follow similar boards, and an ad that we can pin to save in our board or click to visit.

Scrolling down, we see two more unobtrusive but highly relevant ads, fitting not just the theme but also the color scheme of the suggestions and the board.

Financial Review

After this brief product and navigation overview, let’s look at Pinterest’s post-IPO 424 (full document) and their Q1 results (10-Q here).

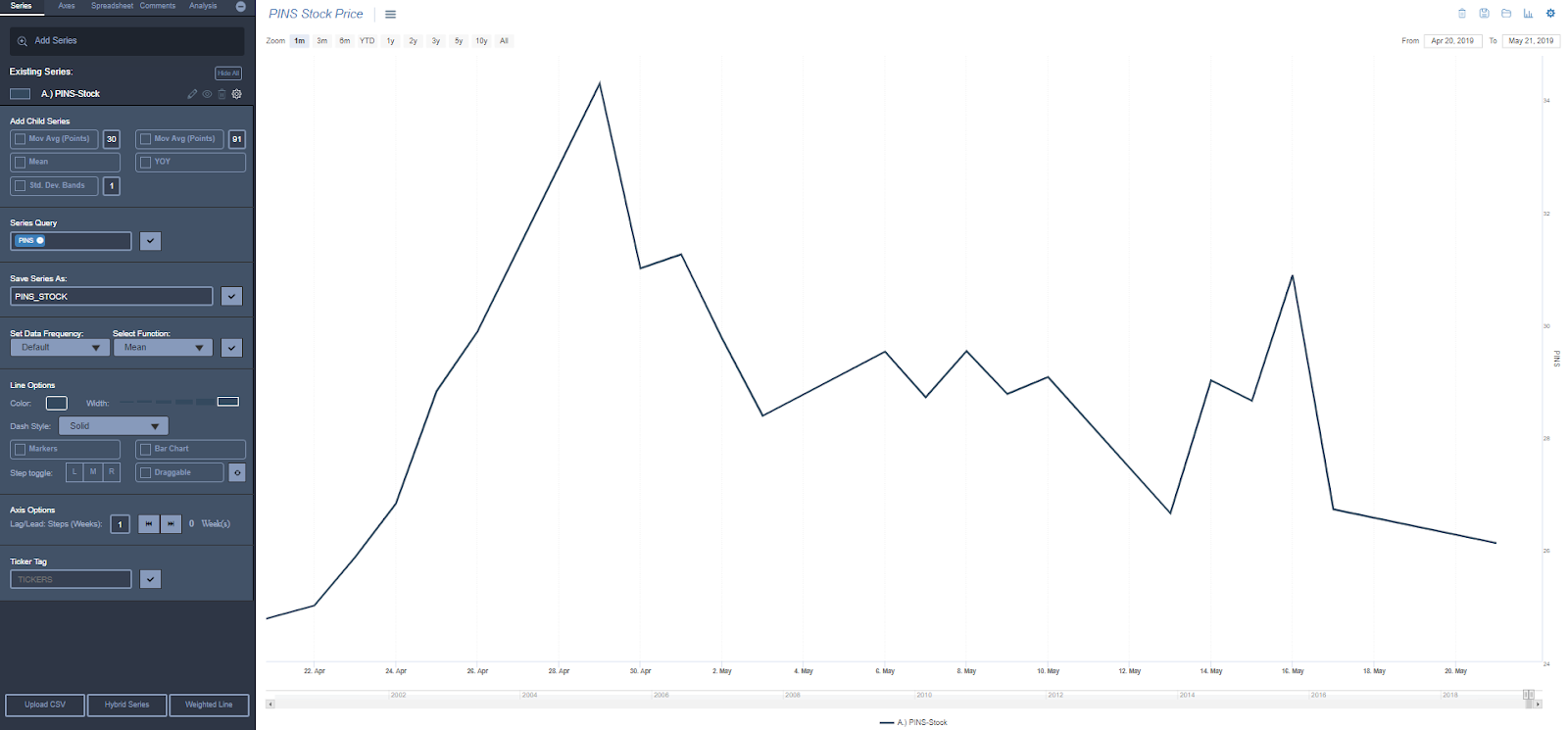

Pinterest IPOed about a month ago in April at $19 per share, then went up to $34 before easing into the mid-$20s after the Q1 results. (Interactive chart)

Notes from our read-through of Pinterest’s Form 424 filing:

Pinterest’s own business description is centered around inspiration and discovery.

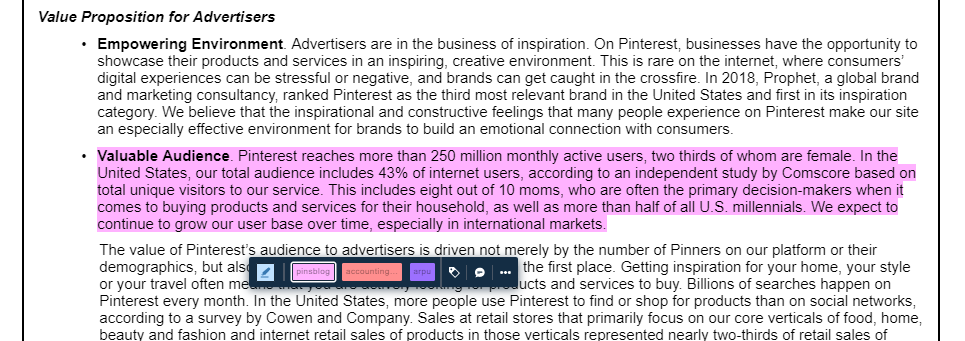

Pinterest’s value proposition to advertisers in clear: 250 million MAUs and 80% of US moms.

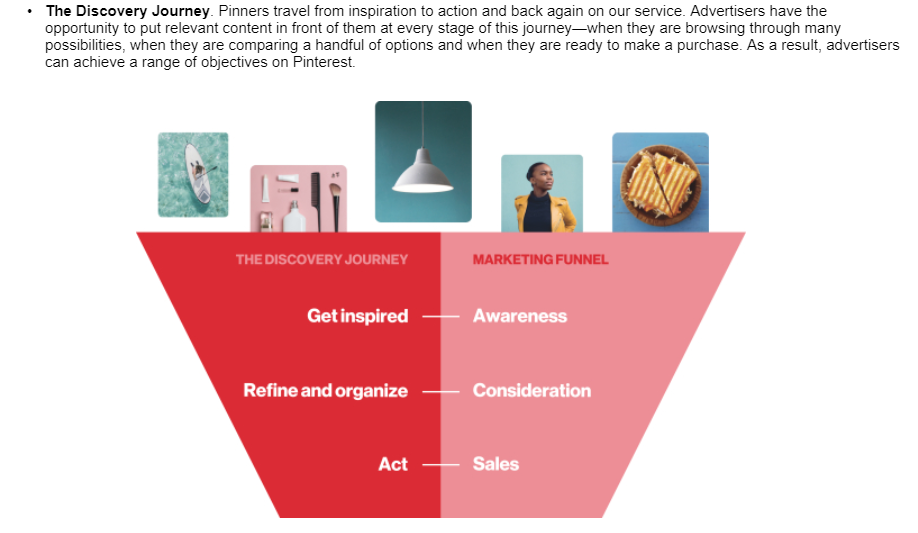

Further, Pinterest hits consumers at different stages in the shopping journey:

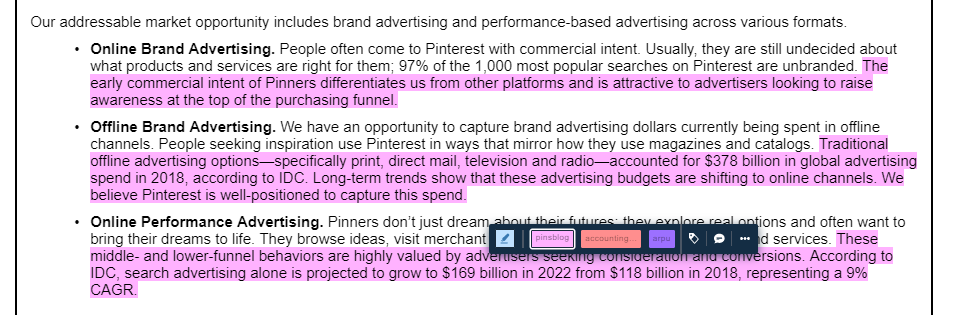

Pinterest is naturally a high-intent environment that is a secular ad dollar share-taker:

The growth vectors that Pinterest is listing include:

- on the consumer side, more shoppable products (similar to the recent Instagram ecommerce integrations)

- more verticals (men can be pinners, too!)

- more localized content

- more commercial content to be “discovered”

On the advertiser side, the growth will come from better relevance, more ad products, and more native and third-party tools.

As we mentioned in our introduction, these are all currently existing monetization paths. Pinterest, in our view, has a very low technological risk.

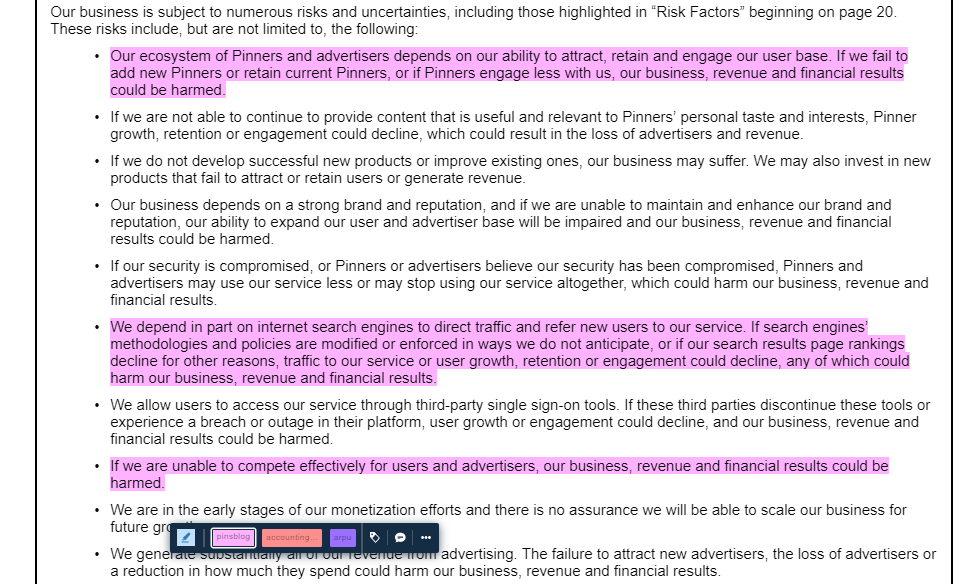

Pinterest’s Risk Factors include a lot of the “usual” factors that we see in tech IPOs. We have highlighted the major ones, in our opinion:

Pinterest needs the network effects of people contributing and sharing content on the platform, it depends on search engine traffic, and there might be competition.

Further down in the document, we see examples of the dependence on search:

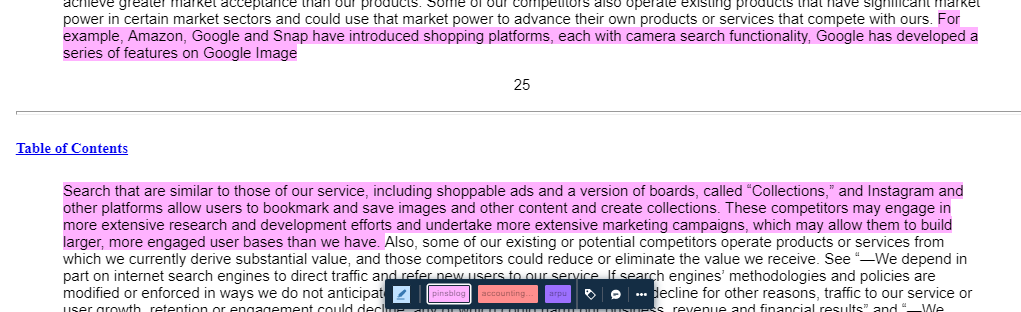

We also see the competition around visual and ecommerce:

In our view, external competition is really the main risk factor: Pinterest has the network effects and the visual search leadership, and digital advertising in its many forms was, is and will be a share-gainer regardless of the economic cycle.

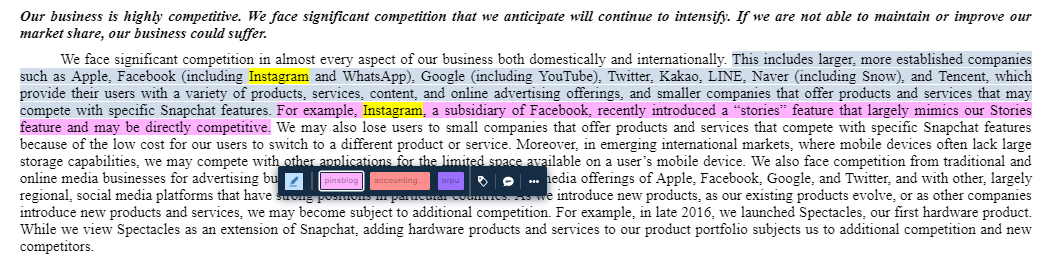

We can see Facebook’s Instagram launching a competitor, similar to what happened with Stories and Snapchat. We do not see this succeeding easily. Pinterest is centered around topics (the way Slack channels or Twitter lists are), unlike the personality-driven Instagram product.

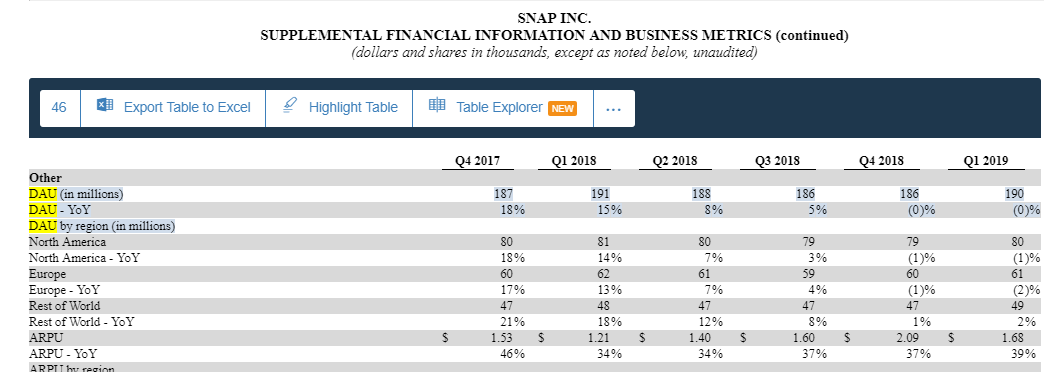

There is a bad precedent though: Snapchat was hit by Instagram’s launch of Stories: the company had to include this in its pre-IPO filing (below), and we saw its DAU growth dampen quickly, and flatline afterwards.

Snapchat’s DAUs have been at 0% growth in the last two quarters, and is actually declining in North America and Europe.

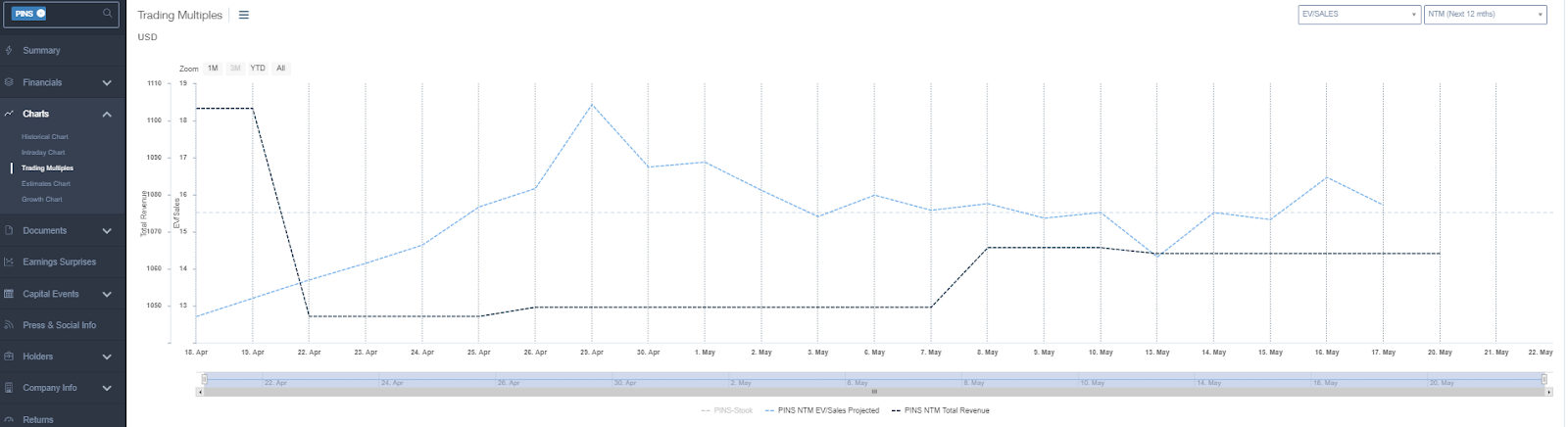

And Snapchat’s stock never really recovered: it is down by about two-thirds from the post-IPO high and its NTM EV/Sales multiple (left axis) has compressed from over 26x to under 9x. (Interactive chart)

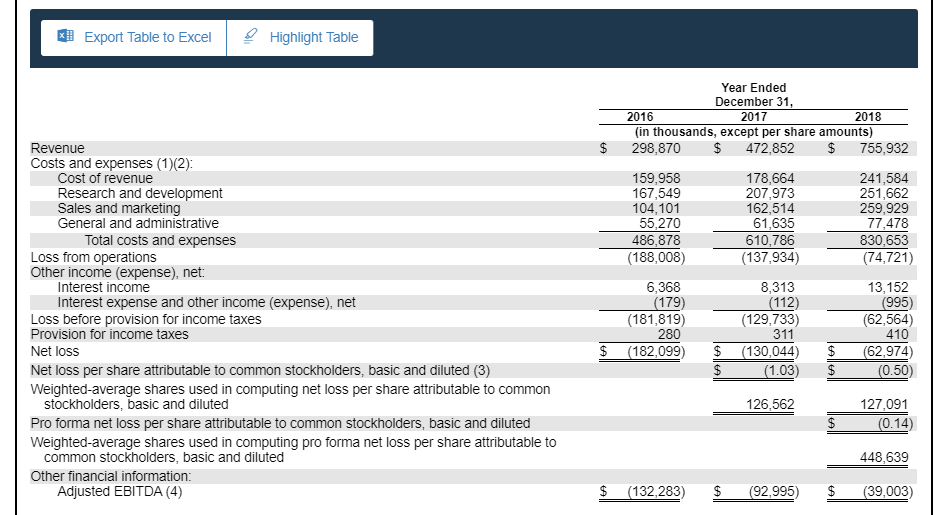

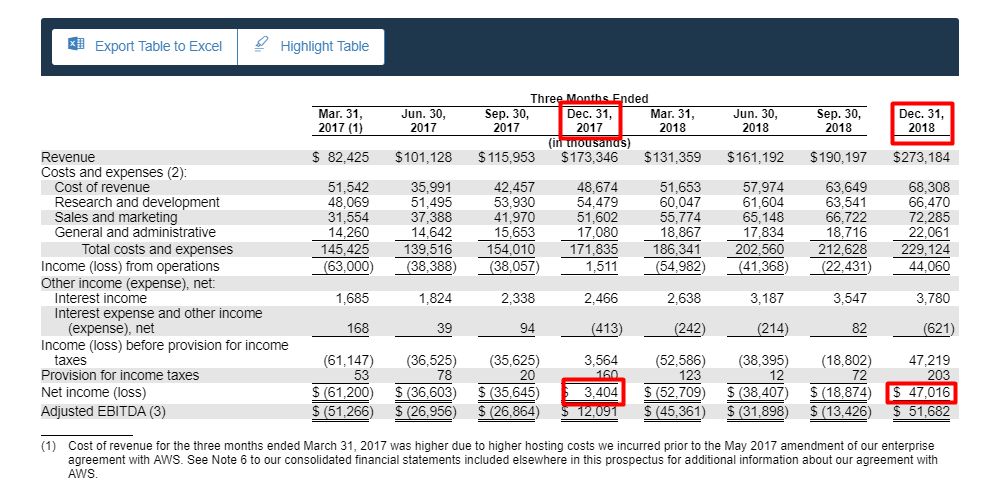

Back to Pinterest: the financials look great.

We see exactly what growth investors want to see: increasing revenues (2.5x over two years) AND narrowing losses (GAAP loss reduced by 2/3rds over the same period).

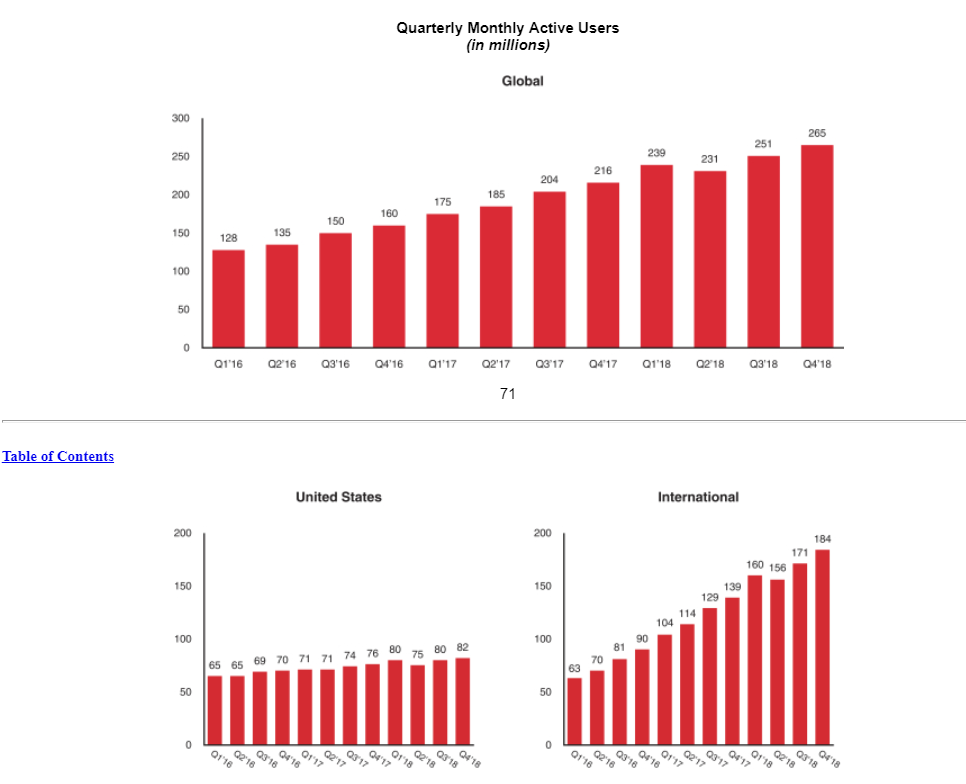

Pinterest’s operating metrics are also going in the right direction: we can see that US growth has naturally flatlined at around 82 million (this is already very well-penetrated), but international is 2x larger already, and growing very well.

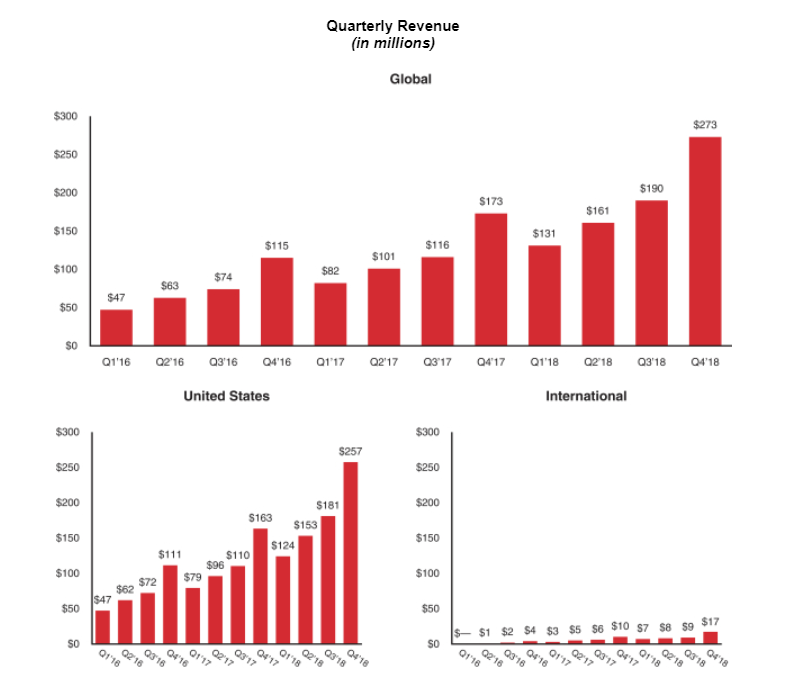

Unlike the user metrics, revenue metrics are very heavily skewed to the US: this is where the largest opportunity lies with Pinterest. There is practically zero international revenue, and dominant US platforms have demonstrated, time and again, that international user monetization is very doable.

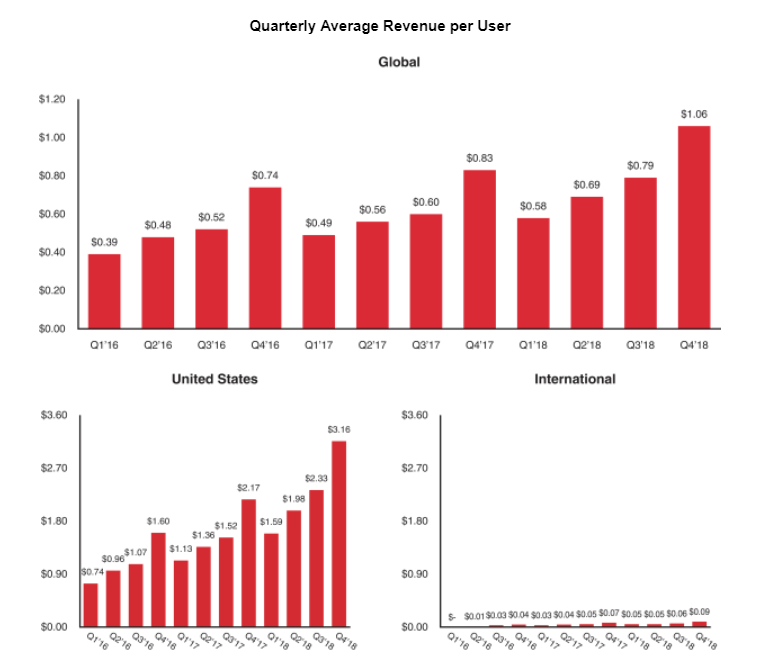

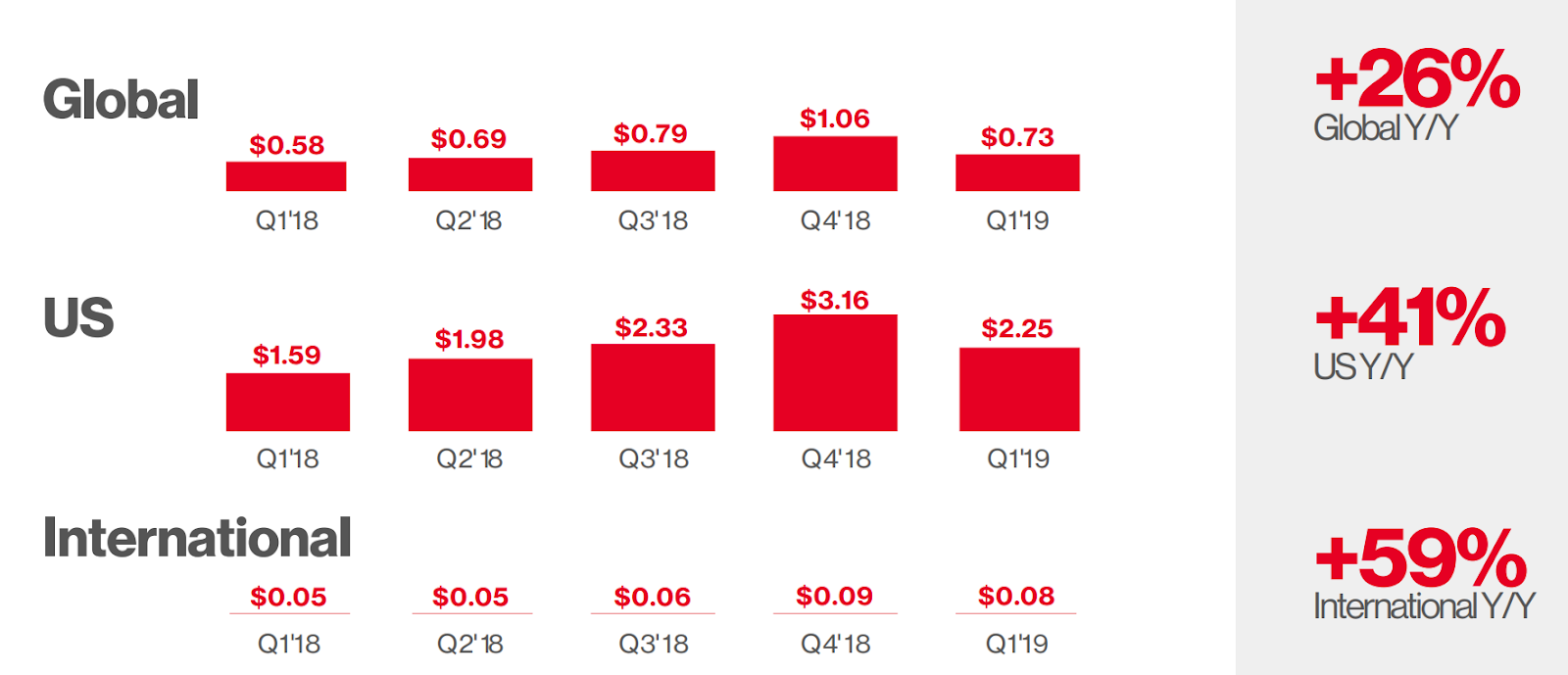

The picture is really stunning at the ARPU level: the US monetized at $1.59 to $3.16 per quarter in 2018, while international users monetized at $0.05 to $0.09 per quarter. International monetization is lower in Pinterest’s comps like Facebook and Twitter as well, but it is not non-existent like we see below.

Perhaps you saw the seasonal spikes in the charts above for US users: Pinterest’s quarterly metrics reveal that the company was actually profitable, on a GAAP basis no less, in both Q4 2017 and Q4 2018. This confirmed our initial feeling that Pinterest is very close to profitability.

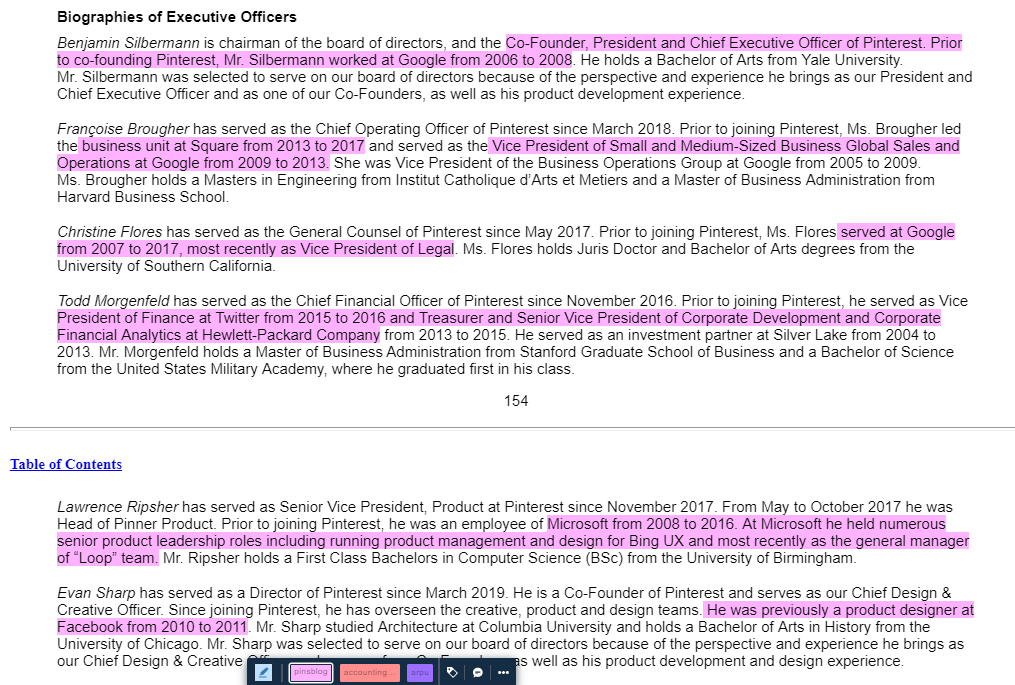

Pinterest is led by its founder, and its management team has prior experience around “Big Tech.” The founder and several employees came from Google, Square, HP, and Microsoft. This is the type of professional background that we like to see.

The Board consists of venture capitalists, predictably, as well as people with online media backgrounds.

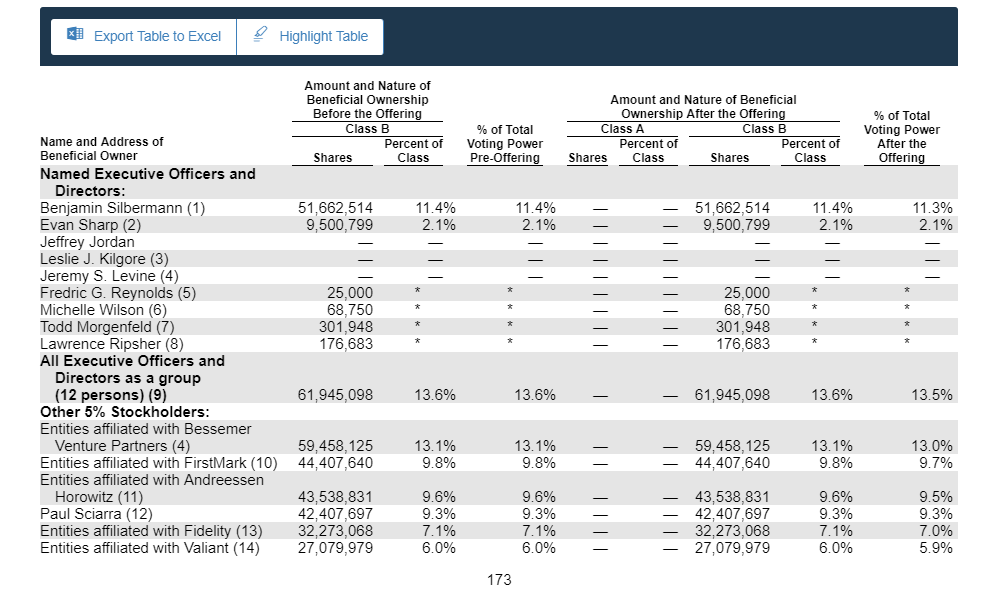

The governance is similar to that of other tech IPOs (ie. dual class shares). The pre-IPO shareholder composition is also typical of recent high-profile tech IPOs: founders, management and VCs.

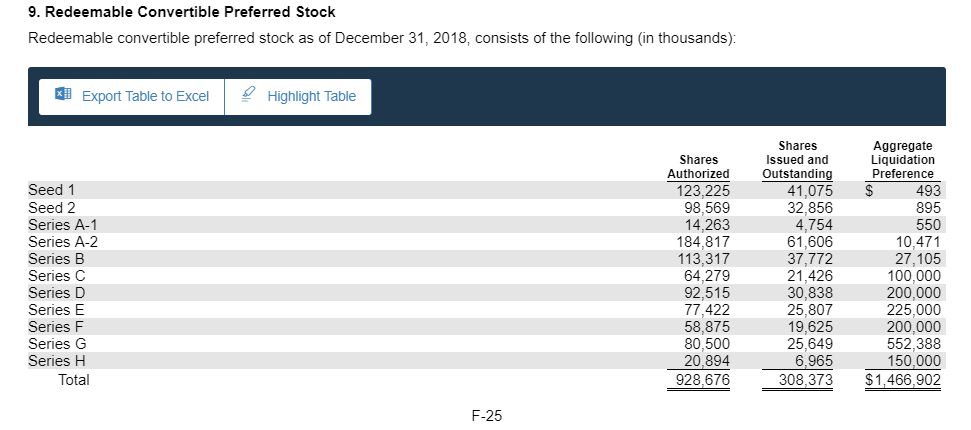

Like we noted in our Slack post, companies are waiting for longer before IPOing: this results in multiple rounds of private financing (here up to Series H).

Since Pinterest reported results recently, we also took a look at their Q1.

First, we saw that everything is going according to plan: more international markets are being monetized, and more features are being added to gain share with ad clients.

The financials also looked great: 54% revenue growth and 22% MAU growth, driven by 29% international MAU growth. MAU growth has been fairly steady in the last 4 quarters: 25%. 23%, 23%, 22%.

ARPU is also growing rapidly, both domestically and internationally:

Losses also improved as a percent of revenue:

However, the stock dropped as media reports indicated that the guidance for 2019 was light (along with the usual “how can they bomb their first quarter?”):

We are much more optimistic on the business in the intermediate and longer-term.

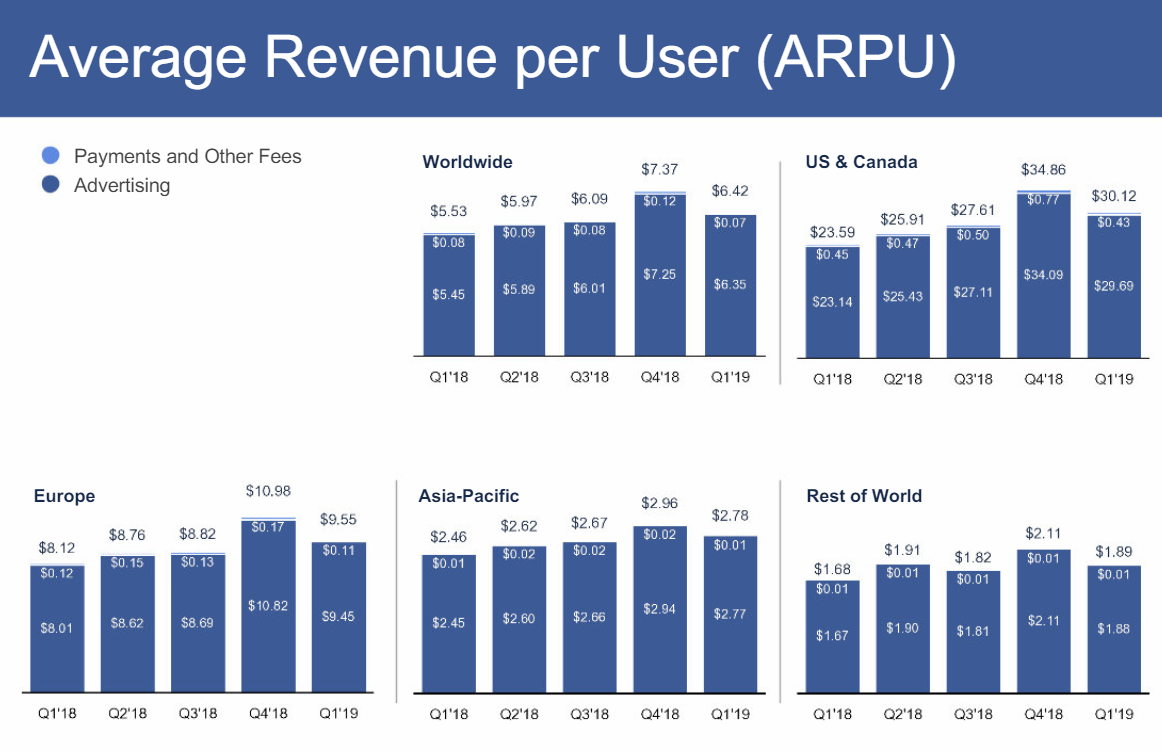

This slide below caught our eye in the earnings release deck. On a running four-quarter basis, Pinterest is monetizing in the low $3’s globally, and literally in the pennies for the international segment.

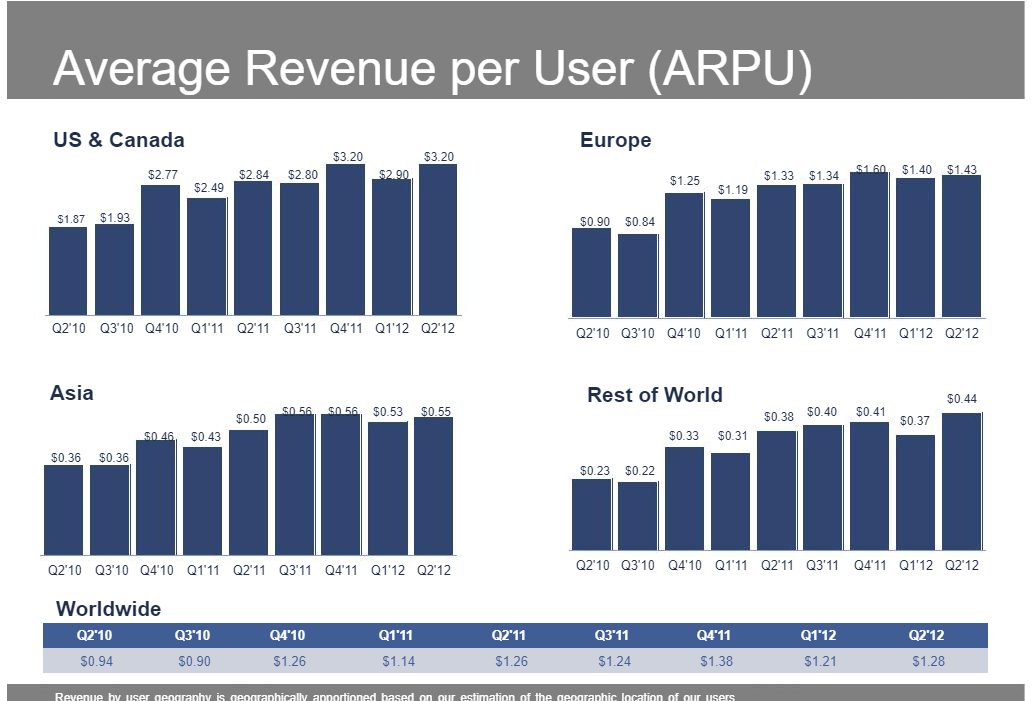

This really reminded us of another great advertising business that you might have head of: Facebook. In this 2012 deck, we can see that pre-IPO, in 2010, Facebook had similar US monetization numbers.

Facebook is now running US monetization at 10x — roughly the ARPUs from back then.

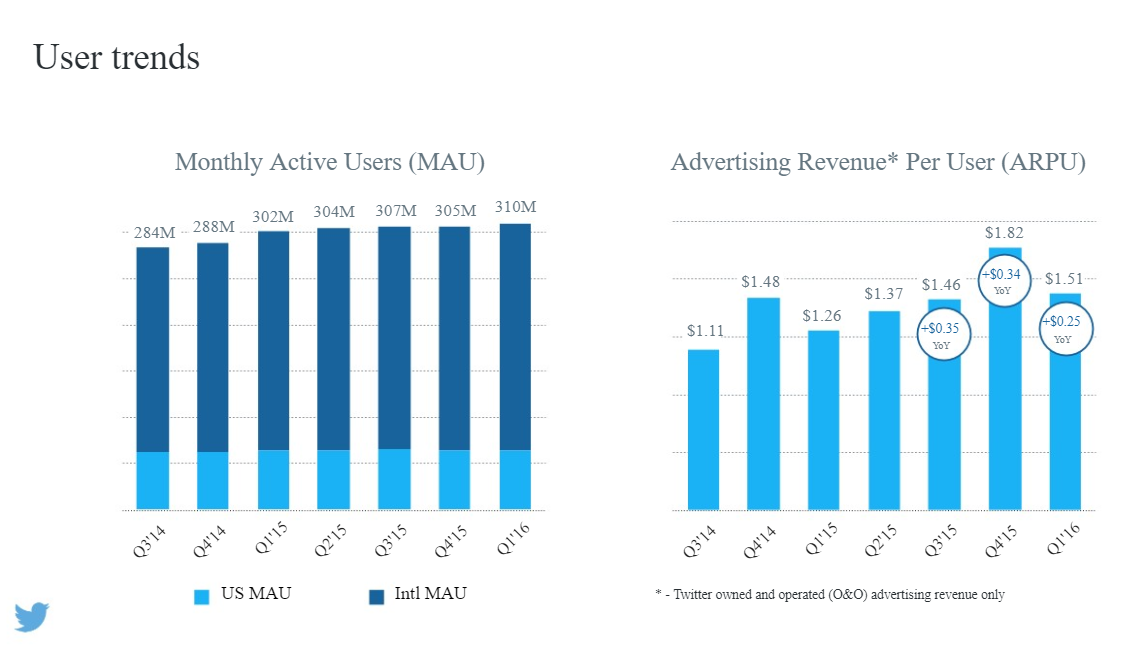

We see something similar with Twitter, but in 2016 (around the same number of MAUs- though this is not a great metric for Twitter and the company recently switched to mDAU, monetizable DAU). US ARPUs are also similar to what Pinterest is running now. Twitter’s US ARPU is now 3-4x these 2016 amounts.

We can see Pinterest monetizing at levels above Twitter — due to the high level of intent — and lower than Facebook, as Facebook has two large monetizable properties.

We can see that Pinterest is currently trading at around 15x EV/Sales on an NTM basis:

Facebook also spent a lot of time trading in the low teens on a EV/Sales basis:

What is different here is that, unlike Facebook’s “early years,” we know for a fact that mobile is monetizable, and we know that video is monetizable, so the business risks are much lower. It really is heavily about the management team executing and following the path that has already been established by others in the space.

We see a similar picture when we combine EV/NTM Sales for LinkedIn, Facebook, Twitter, Snapchat and Pinterest on the same scale: high multiples are not unusual in the early years. (Interactive chart link)

This is even more clear when we align the origins (trading start) for the EV/Sales chart above. (Interactive chart link)

Completely speculatively, we can see Facebook acquiring Pinterest: we have no special knowledge and we would guess that Facebook must have looked at doing this prior to the IPO.

But we know that Facebook is a very smart acquiror (Whatsapp and Instagram being Hall of Fame acquisitions), so it is entirely possible that Facebook (or Amazon) will step in if Pinterest starts gaining more traction. This is a similar situation to LinkedIn: it became the de-facto depository for global, white collar professional information, and it was acquired by Microsoft after a short stint as a public company. We also think that Twitter will be an acquisition target if the business continues its “Disney-fication”, a process we discussed when we listed it as one of our top 11 long ideas in January 2019.

To summarize our view, we see Pinterest as a unique advertising and potentially ecommerce property that has established a very attractive vertical, and is only now turning on the monetization “machine.” Valuation is not dissimilar to what we saw in early Facebook, but with substantially lower business risks: we know what works.

Article by Sentieo