WHG Global Long Bias Fund commnentary for the month ended July 31, 2025.

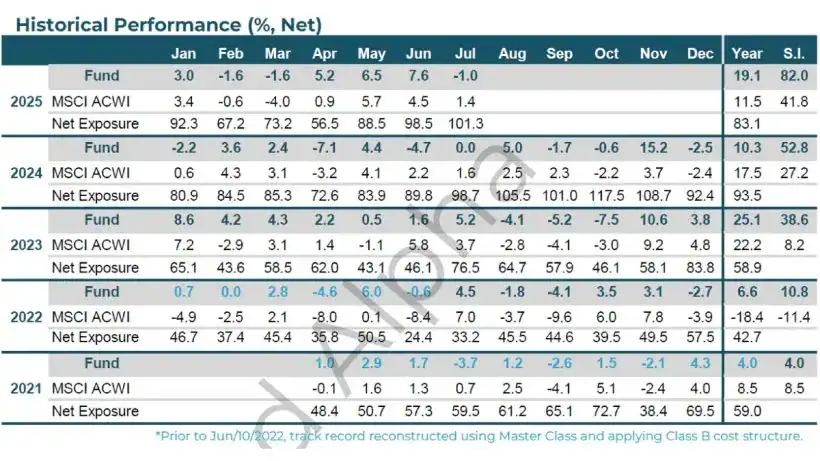

Performance

- July: -1.0%

- YTD: +19.1%

- ITD: +82.0%

Monthly Commentary

Global equities rallied in July as US policy signals turned clearer. Trade agreements with Vietnam, Japan, and the EU helped ease tariff concerns, while the OBBBA package is expected to support economic activity. Corporate earnings exceeded expectations, underscoring the US economy’s resilience. The FOMC kept rates unchanged, but recent softer labor data could lead the Committee to reassess that stance at its next meeting.

Positive Highlights

- AI Winners: Demand for AI accelerated across the entire value chain in July. Google, Meta, and Microsoft now guide for about USD 300 bn of 2026 capex (vs. USD 180 bn in 2024 and a street view of USD 280 bn). Among the leading AI model developers, Anthropic's ARR reached USD 5 billion as of July 2025, up from USD 1 billion in December 2024, while Google's AI Overviews surpassed 2 billion MAUs.

- China Tech: Sentiment around the sector improved after the US eased restrictions on the region, allowing the use of semiconductor design software and export of more GPU models. Additionally, Shein confidentially filed its IPO in Hong Kong, and Chinese regulators shifted their stance to foster "rational competition" among food delivery platforms, replacing prior punitive measures.

- Galderma: The company reported solid results, with strong sales and margins. Nemluvio, their new atopic-dermatitis drug, is taking share thanks to equal-or-better efficacy versus the incumbent therapy.

- Consumer Discretionary (Short): Our short book gained on weak prints/data: Lululemon continued to decline, Chipotle disappointed on same-store sales (SSS), and Wingstop’s alternative data deteriorated.

Negative Highlights

- Europe and Japan (Short): Trade agreements with the US, concluded earlier than expected, came as a positive surprise and supported market performance. Expectations were for negotiations to slip past August due to legislative elections in Japan and a tougher stance from the EU, including potential retaliation measures.

- Natural Gas: Weak energy demand and strong US gas output pressured our position. Rising inventories delayed the rally we've anticipated on AI server demand and stronger LNG exports.

Seee the full factsheet here.

Read more hedge fund letters here