Sohra Peak Capital's commentary for the third quarter ended September 30, 2025.

Dear Partners and Friends,

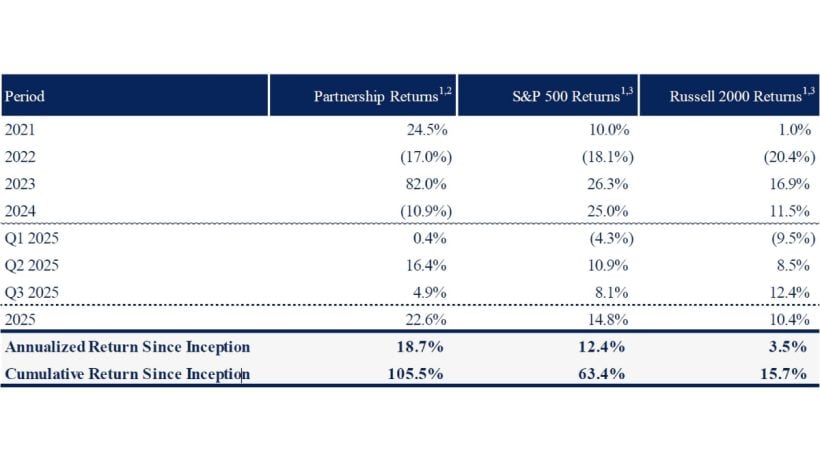

Our partnership recorded a gain of +4.9% net of all fees, expenses, and allocations for the quarter ending September 30, 2025. Over the same period, the S&P 500 recorded a gain of +8.1% including dividends, and the Russell 2000 recorded a gain of 12.4% including dividends.

The below table highlights the partnership’s key portfolio composition metrics as of September 30, 2025:

Our partnership returned +4.9% net of all fees, expenses, and allocations for the third quarter of 2025. At times this year, I am sure I have not been alone in feeling that the only prerequisite that has been needed for a stock to outperform has been to include the words “AI” or “data center” somewhere in its press release. “Momentum” and “junk” stocks have continued to have quite a run, too, defying fundamental gravity for longer than many of us would have wagered.

As you might have correctly guessed, not a dollar of our partnership’s capital has chased the AI theme. Although we perhaps could have doubled (or quadrupled!) our partnership’s assets through well-timed AI trades, in almost all cases, this behavior would have amounted to not much more than speculation in our view. Speculation is neither necessary nor sustainable as an investment strategy, we believe, and history suggests it rarely ends well for those who participate.

During the dot-com unwind, for example, the NASDAQ fell -78% from its March 2000 peak to its 2002 trough.8 Meanwhile, small-cap value stocks led the subsequent years’ equity leadership by a wide margin.9 In other words, there have been long stretches when owning durable, cash generative, smaller companies, the types of companies we seek to own, is precisely the exposure investors wished they had.

Despite the AI mania, we simply continue to apply the same investment approach that we think has served us well since our partnership’s inception. Seek high-quality businesses and management teams, with strong free cash flow per share growth prospects, at low valuation multiples to protect our downside risk. This stance may be unfashionable in a market this narrow, but we would rather be responsible than popular.

As expressed in prior letters, we anticipate reaching a point, perhaps sooner than later, when we will intend to stop accepting new capital. We desire to always maintain a capital base small and nimble enough that allows us to invest in our highest conviction ideas with sufficient concentration. Our goal remains focused on responsibly maximizing investment returns rather than maximizing assets under management. The way we view it, this approach mitigates risk to the durability of our future returns on capital, just as we would expect our portfolio company CEOs to think about their businesses. We also feel we are doing the right thing by our valued partners.

At the moment, we are open to accepting an additional $9 million in new subscriptions. Once our threshold is reached, we intend to close the partnership to new subscriptions forever. Preserving the quality of our partners remains our top business priority. We look forward to meeting likeminded prospective investors.

As always, I would like to extend a thank you to all of our outstanding limited partners, including those of you who have recently joined our partnership, for your steadfast commitment and trust. It is the outstanding quality of our limited partners, a total count which is now 60, that allows our partnership to maintain its long-term orientation over investments, withstand volatility, and realize as best as possible our goal of compounding our capital at the highest rate of return that we responsibly can.

Portfolio Update

Our partners are encouraged to read our commentary on our partnership’s top 5 holdings in Appendix A attached to the end of this letter.

Research Without Reward

Earlier this year, I promised to keep you informed about our pursuit of investment opportunities in Japan. We ended up devoting considerable time this year to one particular Japan-listed company involved in the consumer staples sector. After several months of primary research, including U.S. store visits, competitor scuttlebutt, and a trip to Tokyo, we concluded that this was not a worthwhile investment.

After our first month of research, we sought to speak with investor relations (IR), which was arranged in July. Our primary research had produced encouraging qualitative data points, and thus far, we were becoming increasingly excited about this company’s prospects, pending further, essential outstanding items. I was not quite sure what to expect with IR, given this was my first video call with a Japanese company. I hired a translator (a market that I learned is surprisingly expensive!) and came prepared with a detailed list of questions. Perhaps the most predictive frame of reference for this Japanese corporate meeting came from Peter Lynch’s book Beating the Street:

Japanese firms are very formal and the meetings were ceremonial in nature, with a lot of bowing and coffee tippling. At one company, I asked a question about capital spending, which took about 15 seconds in English, but the translator took five minutes to relay it to the Japanese expert, who then took another seven minutes to answer in Japanese, and what finally came back to me in English was “One hundred and five million yen.” This is a very flowery language. (Peter Lynch, Beating the Street)

Sure enough, our experience was not dissimilar. I knew that hoping to get through my list of 25 questions in an hour was ambitious, but I was not expecting to cover only four and a half of them. While frustrated, I was still determined to receive answers, lest this be an opportunity that got away for lack of trying. Shortly thereafter, upon my request, the company’s management agreed to meet me at their headquarters in Tokyo in August.

The dates offered for this meeting fell less than a week before I was scheduled to travel with my family. In order to make this Tokyo visit work, I booked a round-trip flight where I would leave New York, fly to Tokyo, and be back home just 39 hours later. This allowed enough time to conduct further scuttlebutt at stores in Tokyo, sightsee for a bit, and meet with management before heading back to Haneda Airport for the return flight home.

Contrary to the IR video call, the in-person management meeting was excellent in quality. Three of the company’s top executives attended. Management spent almost two hours with me, addressed almost all of my questions, and noted that I was the first U.S. investor to visit their headquarters in many years. However, it was the substance of their answers that proved surprising. Their responses were detailed yet painted a meaningfully weaker outlook than I had expected, which was the exact opposite message that IR had communicated just weeks earlier! In fact, after we concluded the meeting, IR, who had sat in on the meeting, turned to me and said, “I hope you are still interested in our company,” which was about the closest to an admission of guilt we may ever hear from a public company investor relations representative.

Ultimately, we did not come home with a high-conviction, home run idea, and that was perfectly acceptable. In a different set of circumstances, under different strategic decisions, this company might have become a compelling investment, but in this timeline, it wasn’t. As underwhelming as the outcome was in the moment, nonetheless, for every prospective investment we find that begins to emerge as an attractive situation, we will always conduct those months of diligence and we will always take that 39-hour roundtrip to Tokyo, in the event that the attractive situation does materialize. This is not the first prospective investment of ours with dozens of hours of logged research that has ended in a “pass,” and it certainly won’t be the last, though in between is where the diamonds in the rough are discovered. The only logical course of action as we see it, especially after running into a string of deflating high-effort dead ends, is to accept the result, take it in stride, and move on to the next opportunity with the same high energy.

Relevant to our learnings on Japan, this particular company’s main business involved consumer staples with a notable U.S. component. We therefore believed it might be more insulated than the typical Japanese company from the risk of information and communication frictions for foreign investors, but to the contrary, this experience underscored for us that despite our best efforts, this risk can very much still exist.

With that in mind, I have concluded that the best opportunity for us to participate in Japanese equities is through a basket approach, an approach that we have given a great deal of thought and research to over the course of this year. In May, we spent several weeks carefully constructing a basket of 25 deep value, smallcap Japanese equities that we screened using quantitative criteria and selective judgment. We then monitored that basket’s performance over a trial period through the end of September. We were pleased with the results, as the basket outperformed relevant Japanese stock market indices by a healthy margin, and the worst performer in the basket declined by only -2%.7 As a result, going forward, our partnership may consider a basket of Japanese equities for investment, continually updated and monitored. We would view this as a collective position in our portfolio that we believe could deliver double-digit average annual returns while possessing below-average risk of permanent capital impairment.

Closing Thoughts

Thank you for taking an interest in our latest letter. I am excited about our partnership’s future.

I remain confident that our partnership’s north star will always be to compound our capital at the highest rate of return responsibly possible. In some respects, this approach may render our partnership uninvestible by many institutional investors. That is perfectly fine by me. We will continue to accept as partners only those who understand, and who are aligned with, our objective.

If you wish to learn more about the partnership, please feel free to reach out to me directly. Our partnership currently welcomes introductions to new investors who are aligned with our philosophy and our long-term approach. Readers interested in receiving future letters can register at our website www.sohrapeakcapital.com.

I value the trust you have placed in me to invest your hard-earned capital, as the substantial majority of my own wealth is presently invested alongside yours. I look forward to writing to you again next quarter.

Most Sincerely,

Jonathan A. Cukierwar, CFA

Manager of Sohra Peak Partnership LLC, the General Partner of Sohra Peak Capital Partners LP

Read more hedge fund letters here