RPD Opportunity Fund commentary for the month ended September 30, 2025.

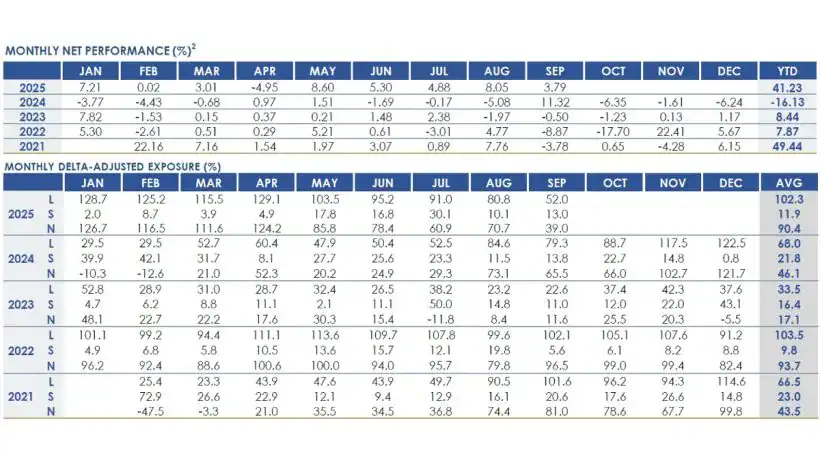

The RPD Opportunity Fund gained 3.79% net in September, bringing the year-to-date performance to 41.23% net and inception-to-date returns to 107.06% net. September performance was led by our outright long positions and steady option premium income, while shorts modestly detracted.

The estimated performance figures net of fees as of September 30, 2025

| Month | Year to Date | Inception to Date | Annualized Net Return | |

|---|---|---|---|---|

| RPD Opportunity Fund | 3.79% | 41.23% | 107.06% | 16.90% |

| S&P 500 | 3.64% | 14.82% | 93.01% | 15.13% |

| RUSS 2000 | 3.06% | 10.34% | 25.16% | 4.93% |

| NASDAQ | 5.67% | 17.92% | 79.58% | 13.37% |

Inception date - February 1, 2021

Anywhere Real Estate (HOUS) was the standout contributor. We built our position at a cost basis of $3.50 about a year ago and fully exited at $10.50 during the month. At entry, our thesis was threefold: (1) buyer agents would remain integral to the industry following the National Association of Realtors (NAR) settlement, which restructured U.S. broker commission rules but ultimately preserved the traditional role of agents; (2) commission rates would stabilize; and (3) housing demand would recover as mortgage rates began to ease. Those views were validated by three consecutive quarters of stable commissions and early signs of pent-up demand emerging. September also brought a strategic takeout proposal from Compass (COMP) that further underscored the value of HOUS’s platform. The market recognized what we believed all along—that its brokerage, franchise, title, and escrow businesses held significant strategic appeal. Our disciplined entry and decisive exit produced an excellent result.

We also exited Baidu (BIDU) during the month. Investor sentiment around the company has improved meaningfully, a sharp reversal from the search monetization pessimism that weighed on the stock for more than a year. Investors are now focused on Baidu’s AI initiatives, cloud growth, and proprietary chip development, even though search monetization concerns continue to persist. While the rally in Baidu highlighted the depth of its AI ecosystem and potential monetization beyond traditional core search, we exited into strength and fully eliminated China exposure, consistent with our cautious stance on the region.

Our options strategy added meaningfully to results. Cash-secured put selling in Monday.com (MNDY) and Appian (APPN) provided attractive opportunities as temporary AI-driven concerns created dislocations across application software. Monday’s August earnings disappointment, specifically tied to changes in Google Search, created an ideal entry point. After September’s Investor Day, shares had recovered, and option premiums decayed in our favor. Appian shares continued to benefit from strength in its sticky process automation business, which has helped insulate its growing Federal business from DOGE-driven scrutiny. These outcomes highlight how our three decades of experience in software enable us to identify and act quickly when sentiment diverges sharply from fundamentals.

Consumer discretionary positions including Crocs (CROX), Six Flags (FUN), Bath & Body Works (BBWI), and Snap (SNAP) also contributed, supported by stable consumer demand relative to mediocre second-quarter prints, which produced favorable entry valuations.

Even though we have recently generated strong returns, on a delta-adjusted basis our outright positions are as light as they have been in some time—a reflection of the scarcity of attractive opportunities in today’s elevated market. Average notional exposure in September was 120% long and 20% short, for net exposure of about 100%. On a delta-adjusted basis, however, long exposure was just 52% and short exposure 13%, resulting in net exposure of 39%. A significant portion of the portfolio remains expressed through short-dated, fully cash-covered puts that generate premium income while preserving the flexibility to deploy capital into outright longs if valuations become compelling enough to meet our strict investment criteria.

Since inception in 2021, the Fund has delivered a net annualized return of 16.90% during one of the most challenging stretches for value investors in decades. We believe the combination of our strict discipline, research process, and ability to act decisively when dislocations emerge will allow us to compound meaningfully when opportunities become more plentiful.

If you have any questions or require additional information, please contact Investor Relations at [email protected].

Best regards,

RPD Fund Management LLC

(212) 201-2650

Read more hedge fund letters here