RPD Opportunity Fund's commentary for the month ended January 31, 2025.

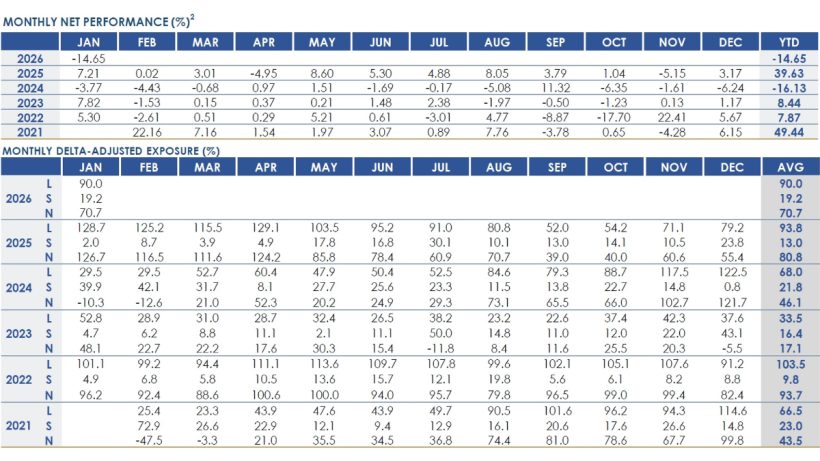

The RPD Opportunity Fund declined 14.65% net in January. The drawdown was driven almost entirely by unrealized mark-to-market losses on the long side, reflecting a sharp and concentrated selloff across core long positions. There were no meaningful realized losses during the month. Short exposure detracted modestly, while the remainder of the portfolio had a limited impact on overall results.

The estimated performance figures net of fees as of January 31, 2026

| Month | Year to Date | Inception to Date | Annualized Net Return | |

|---|---|---|---|---|

| RPD Opportunity Fund | -14.65% | -14.65% | 74.71% | 11.83% |

| BarclayHedge Equity L/S | 1.96% | 1.96% | 49.45% | 8.37% |

| S&P 500 | 1.44% | 1.44% | 101.02% | 14.99% |

| Russell 2000 | 5.34% | 5.34% | 34.80% | 6.15% |

Inception date - February 1, 2021

January was characterized by a severe and largely indiscriminate selloff in software, despite broader equity indices finishing the month higher. The software index (IGV) declined approximately 15% during January, while the typical enterprise software name was down closer to 20%. Losses in the fund were concentrated in software, largest area of exposure as outlined in last month’s commentary, and were driven by a sharp swing in sentiment, positioning, and a broad narrative shift around artificial intelligence rather than company-specific fundamentals. Valuations across multiple holdings declined to levels last seen during past recessionary lows, despite strong balance sheets, durable free-cash-flow generation, and ongoing share repurchase activity. Conservative expectations embedded in prices became even more pessimistic.

Nearly all of the Fund’s losses during the month were unrealized. Core holdings became materially cheaper despite no deterioration in operating performance. We believe current prices imply long-term outcomes that are inconsistent with the earnings power, competitive positioning, and cash generation of the businesses we own.

From a portfolio construction standpoint, the Fund carried approximately 130% notional long exposure as of the end of the month. This consisted of roughly 70% outright equity positions, 30% exposure through in-the-money put options, and an additional 30% exposure through out-of-the-money put options. These put options were written with the intent to acquire stock at prices we view as materially discounted relative to intrinsic value.