RPD Fortress Fund’s commentary for the month ended October 31, 2025.

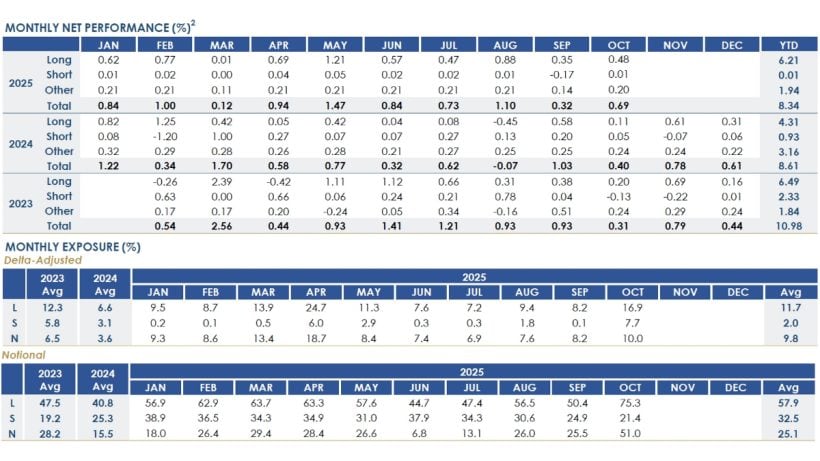

RPD Fortress Fund returned +0.69% net in October, bringing year-to-date gains to +8.34% net and inception-to-date performance to +30.61% net. The Fund has now delivered positive results in 32 of the 33 months since inception, underscoring the consistency and resilience of the strategy across varying market environments.

The estimated performance figures net of fees as of October 31, 2025

| Month | Year to Date | Inception to Date* | |

|---|---|---|---|

| RPD Fortress Fund | 0.69% | 8.34% | 30.61% |

| BarclayHedge Equity Long Short Index** | 0.70% | 12.43% | 28.52% |

| Bloomberg US Aggregate TR | 0.62% | 6.80% | 10.70% |

Performance Statistics

| Annualized Net Return | Volatility | Sharpe | Sortino | Positive Months |

|---|---|---|---|---|

| 10.18% | 1.75% | 3.47 | 6.73 | 97% |

*Inception date - February 1, 2023

**Based off reporting by 16 funds as of Nov 4, 2025

Both cash-covered put and call writing contributed positively during the month, while the Fund’s long deep-in-the-money SPY puts, a newly implemented part of our refined risk management framework, detracted modestly. These SPY puts now serve as a dynamic hedge, enabling the portfolio to always maintain a net delta below 15% while allowing the flexibility to write additional puts when opportunities arise. The portfolio remained fully cash-covered and effectively market-neutral in October, with monthly average exposures of 75% long and 21% short notional, resulting in a 10% net delta.

Performance during the month was supported by disciplined premium capture and select opportunities identified through our fundamental research. ZoomInfo (GTM) was a notable contributor, where Fortress benefited from option writing at compelling strike levels, leveraging deep research insight without taking directional exposure. GTM continues to trade at attractive valuations of roughly 10x P/E and a 12% free cash flow yield at our strike price – levels that, in our view, offer a strong margin of safety for a stable, recurring-revenue software business positioned to benefit from AI-driven sales and marketing efficiency trends.

Criteo (CRTO) also added to performance. A long-standing research focus since 2019, CRTO operates a leading performance marketing and commerce media platform. Despite durable profitability, robust cash generation, and a clean balance sheet, the stock continues to trade at unusually depressed levels—below 2x EV/EBITDA, under 1x EV/Revenue, and below 4x P/E at our strike prices. CRTO has been mispriced due to overstated concerns about agentic commerce risk; Fortress selectively wrote cash-secured puts around this dislocation, capturing elevated implied yields into month-end.

The Fund continues to emphasize liquidity, discipline, and precision in strike selection, maintaining capital protection through conservative delta management and dynamic hedging. The introduction of long SPY puts provides an additional layer of flexibility, allowing measured participation during stable markets and meaningful downside insulation should volatility resurface.

If you have any questions or require additional information, please contact Investor Relations at [email protected].

Best regards,

RPD Fund Management LLC

(212) 201-2650

Read more hedge fund letters here