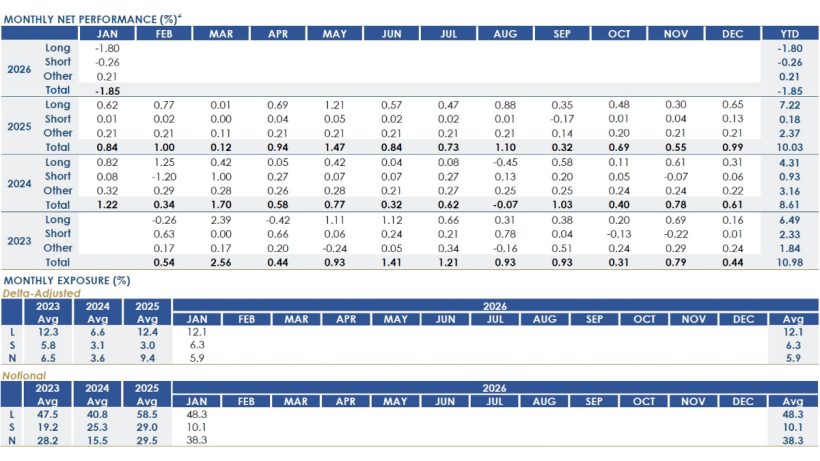

The RPD Fortress Fund declined 1.85% net in January, marking the first meaningful down month since inception. As the Fund completes its third year of operations, it has generated positive returns in 34 of the past 36 months, reflecting the consistency of the strategy across a range of market environments. While the Fund experienced a modest drawdown in August 2024, January represents the first period in which unrealized option positions drove a monthly decline.

The estimated performance figures net of fees as of January 31, 2026

| Month | Year to Date | Inception to Date* | |

|---|---|---|---|

| RPD Fortress Fund | -1.85% | -1.85% | 30.17% |

| BarclayHedge Equity Market Neutral Index** | 0.60% | 0.60% | 29.24% |

| Bloomberg US Aggregate TR | 0.11% | 0.11% | 11.36% |

Performance Statistics

| Annualized Net Return | Volatility | Sharpe | Sortino | Positive Months |

|---|---|---|---|---|

| 9.18% | 2.28% | 2.26 | 1.16 | 94% |

*Inception date - February 1, 2023

**Based off reporting by 12 funds as of Feb 3, 2026

Performance during the month was driven entirely by mark-to-market pressure on existing cash-secured put positions, predominantly within software. Realized trading activity was modestly positive, and realized positions generated small gains; however, these were outweighed by unrealized losses on open put positions. Importantly, cumulative premium captured and premium currently on the books are substantially greater than the January drawdown, with exposure remaining within established portfolio limits. Only two positions finished the month in-the-money, with the remainder out-of-the-money. This premium cushion provides a constructive starting point as the portfolio moves through February, without any change to portfolio risk parameters.

January was characterized by an unusually sharp and indiscriminate selloff in software, driven by heightened debate around AI’s impact on the terminal value of software businesses, and represented the worst monthly decline for the sector since October 2008. Software represents a meaningful area of focus for the strategy given our more than three decades of experience investing across multiple software cycles, and our view that current valuations in select, high-quality businesses already discount overly pessimistic assumptions regarding growth, AI disruption, and terminal value. Our focus remains on companies with durable customer relationships, strong balance sheets, and clear pathways to AI-enabled efficiency or monetization, rather than speculative beneficiaries of AI adoption. All positions that detracted from performance were concentrated in software, where option pricing temporarily became detached from underlying fundamentals. In contrast, consumer discretionary positions contributed modestly positively to results.