McIntyre Partnerships' commentary for the fourth quarter ended December 31. 2025.

Dear Partners,

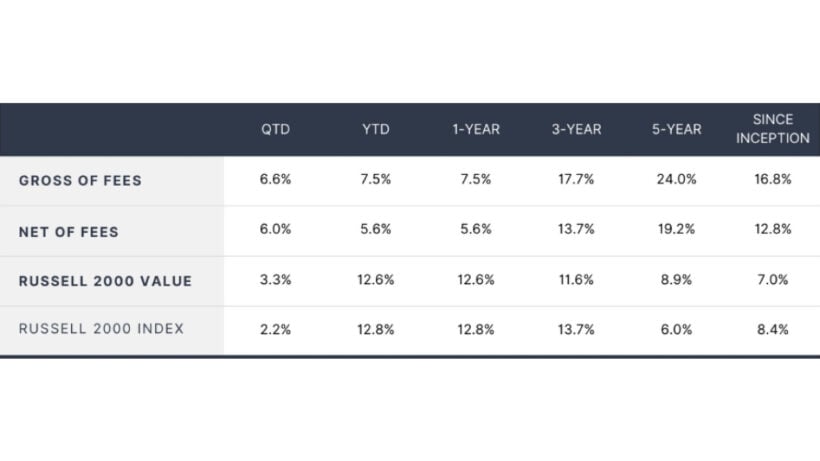

McIntyre Partnerships Returns

Performance and Positioning Review – FY 2025

Through year-end 2025, McIntyre Partnerships' results were approximately 8% gross and 6% net. This compares to our benchmark, the Russell 2000 Value, which increased ~13%. The fund’s trailing five-year returns are ~24% gross and ~19% net per annum, which compares to our benchmark’s return of ~15% per annum. Since inception, the fund has returned ~17% gross and ~13% net per annum, compared to our benchmark’s return of ~7% per annum. Please note that a small residual side-pocket investment was paid out in Q4, which may affect partner statements.

In the winners column, SHC and FTRE contributed >500bps, while GTX, SPHR, and Stock A contributed 100-500bps. In the losers column, LESL, SEG, and STRZ lost 100-500bps.

2025 was a choppy, frustrating year that in the end finished “alright” – not one for the record books, but not awful either. While these years are not my favorites, I consider them an inevitable part of our strategy. We are not short-term traders, and our investments often require multiple years to be proven out. I believe our ~10% per annum of gross outperformance since inception speaks to this. If in our worst years we earn mid-single-digit returns and in our best we achieve >45% returns, as we have had for a third of the time since inception, we will do just fine over time.

Further, beneath the surface, I believe our portfolio substantially improved in 2025 due to new ideas and a significant rotation from gainers to laggards. Among our new ideas, the most important is Stock A, which is now our largest holding. I believe the investment offers multibagger upside over the next few years with minimal risk of permanent loss. Despite its importance to the portfolio, I am still considering a larger investment. I will not provide public comment until I am sure we are no longer adding. In addition, despite modest portfolio-level returns, several investments rallied substantially, while others declined sharply. I have rotated our capital from winners where I think value is fairly reflected to those where things are improving yet the share price actually fell. I believe this sets us up for strong returns in 2026.