L1 Capital Global Long Short (Offshore Feeder) Fund commentary for the month ended December 31, 2025.

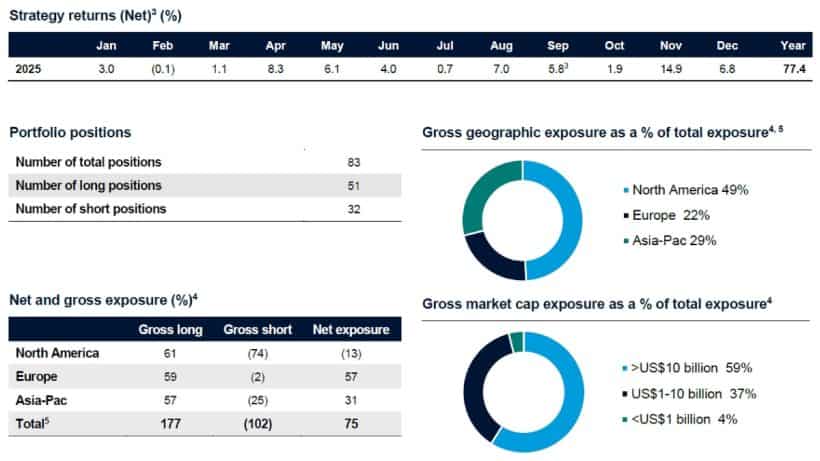

- The L1 Capital Global Long Short Fund (GLSF) returned 6.8%1 in December (MSCI World 0.8%2).

- Since inception in January 2025, GLSF has returned 77.4%1 (MSCI World 21.1%2).

- Markets finished the year with muted returns as easing U.S. inflation data was offset by uncertainty around the timing and pace of future Federal Reserve rate cuts.

Global equity markets were mixed during the month, with U.S. markets largely flat and European and Asian equities recording modest positive returns.

In the U.S., encouraging inflation data – November CPI of 2.7% versus expectations of 3.1% – was offset by ongoing uncertainty around the future path of Federal Reserve policy. While the Fed delivered a widely anticipated rate cut at the December FOMC meeting, commentary signalled a cautious approach to further easing in 2026, tempering investor enthusiasm.

European and U.K. equities were supported by moderating inflation, declining gas prices and rising expectations for early policy easing, with broad-based gains across Financials, Resources and Healthcare.

Asian equity markets advanced on the back of strong semiconductor and A.I.-related performance, with Australian equities also higher, supported by outperformance in Resources and Financials.

The portfolio performed very strongly over the month, with broad-based gains across numerous positions – 28 stocks each contributed more than 0.2% to returns. Since the Strategy’s inception on 1 January 2025, a total of 51 stocks have each contributed more than 1% point to overall performance.

Key contributors during the month included long positions in Mineral Resources and gold equities (including K92 and IAMGOLD), alongside gains from short positions in several high-P/E or unprofitable technology stocks that declined sharply.

Mineral Resources rallied as lithium prices continued to move higher (+37% in December to end the year up ~90%). In addition, the iron ore price held at attractive levels (>US$108/t), positioning the business well, with Onslow Iron achieving nameplate capacity.

K92 and IAMGOLD benefitted from the broader rally in gold equities as gold prices continued to move higher over the month. Gold’s significant outperformance continues to be driven by large and growing U.S. federal fiscal deficits and debt levels, U.S. dollar devaluation, emerging market central bank gold accumulation and a global interest rate cutting cycle.

Equity valuations at current index levels appear relatively full, largely due to significant crowding in a handful of mega-cap names. Beyond these crowded areas, we are finding a large number of attractive investment opportunities across all developed markets, where we see a compelling combination of strong earnings growth, shareholder friendly management, conservative balance sheets and significant valuation support. We continue to believe that infrastructure, gold, U.S. cyclicals, uranium and ‘quality value’ stocks provide some of the best opportunities globally.

Read more hedge fund letters here