Kernow Asset Management's commentary for the month ended August 31, 2025.

In August, the strategy dipped 0.4% as the market caught the scent of incoming November tax hikes.

Too much is never enough.

“We are not going to be coming back with more tax increases.” - Chancellor of Exchequer, November 2024.

It feels like déjà vu. We are again ready for any AIM IHT opportunities that arise. We hope the government goes after gambling firms this time. The Kernow portfolio is exposed in banking, housing and retail. Our shorts will be kept busy, though they were built for skirmishes rather than sieges.

WH Smith: Putting The 'Con' Into Convenience Store.

Ironically, we were starting to think about cutting that very protective short book. It kept burning us, and the pressure was building. Then came a bucket of cold water to the face. Junk shares, one by one, stopped rallying. WH Smith led the retreat.

Historically, this business has been high on debt and low on imagination. The goods are generic, the racking woeful, and the lighting is photophobia incarnated. It is a low moat business, propped up by nothing more than location inertia and the desperation of a captive audience. Exceptional management could make it work. That has not been the case. Even the board agrees and has been selling off limbs.

To make matters worse, it now turns out 21% of its profits are made up. To us, it does not appear to be a full scale fraud. WH Smith’s culture and lack of sophistication suggest something more like sloppiness than deception. This is not Uzi Katz territory.

Scapegoats Don't Pay The Rent

We imagine that the board already knows the problem and has lined up US scapegoats to fire. An independent report by Deloitte will follow. It will be narrow in scope, forward looking in tone. It will discover a “small number” of accounting errors, which management will declare immaterial. Promises will be made. Controls will be tightened. Lessons will be learned. Apologies will be issued in a conditional tense.

In the real world clean up, more issues and costs will surface, resulting in two profit warnings. Much of this is already priced in. A fine is not. Factor in expensive rents and the Kernow valuation falls to £330m versus the market’s £850m. We are clearly missing something for now.

Metro Signals 36% Valuation Gain

Good news. Metro Bank’s H1 2025 results landed with profits tripling, and the regulator unexpectedly signalled that the bank may be allowed to exit the MREL band. Think Justin Timberlake leaving NSYNC. Metro is going solo!

This shift would unlock c.£500m in expensive capital that currently sits idle. Releasing this could increase profits by one-third. This is still an active mispricing. One more regulatory update is needed. The structure is complex. Even under a simple runoff model to 2028, we raise our valuation to £5.50. The shares trade at £1.30.

One Bank’s Provision Is Another’s Funeral.

The mysterious bank we have been acquiring this year is Secure Trust Bank. Apologies for the delay in naming it; some climbs are safer in silence. The trade has now cleared the death zone, helped along by the recent UK car finance court ruling, which landed firmly in the company’s favour. The judge sided with the downtrodden banks and penalised the great unwashed. At last, justice for the people… who repossessed my nan’s Volvo.

The cases were brought by a factory supervisor, a trainee nurse, and a postman over second-hand cars they purchased from dealerships with financing that included egregious commissions as high as 25% of the car's value. Upsettingly to us, the judgment suggests that there is no such thing as a savvy second-hand car buyer or a decent used car dealer. Getting fleeced is simply part of the experience. How lovely.

Our estimate is that Secure Trust’s provisions may still rise from £6m to £20m. We’ve modelled £40m to stay on the cautious side, and even at that level, the bank remains comfortably capitalised. At the same time, we’re short another bank where a similar provision escalation would be terminal. Same storm, different kit.

Next waypoint: Secure Trust’s Capital Markets Day in November.

US GAAP: Lipstick On A Pig

We are betting against the worst business model in the FTSE. Last month, this company issued a profit warning, causing the stock to decline by 20%. The CEO lashed out and hinted that its listing might move to the US – two separate red flags.

The only thing “asset-light” about this business is its profits. The company switched to US GAAP to make the numbers more palatable. Reported profits stand at zero. Adjusted for real accounting, it's a loss of over £100m. Even before accounting for off-balance sheet items, it is in negative equity. The company is more than 20 years old and has been saved from bankruptcy four times. It operates with zero margin, high capital expenditure, and extreme leverage. It has only ever been profitable during periods of rising inventory values. That is when it raises capital to expand the empire.

In a strong market, it's a house of cards. In a weak one, someone sneezes.

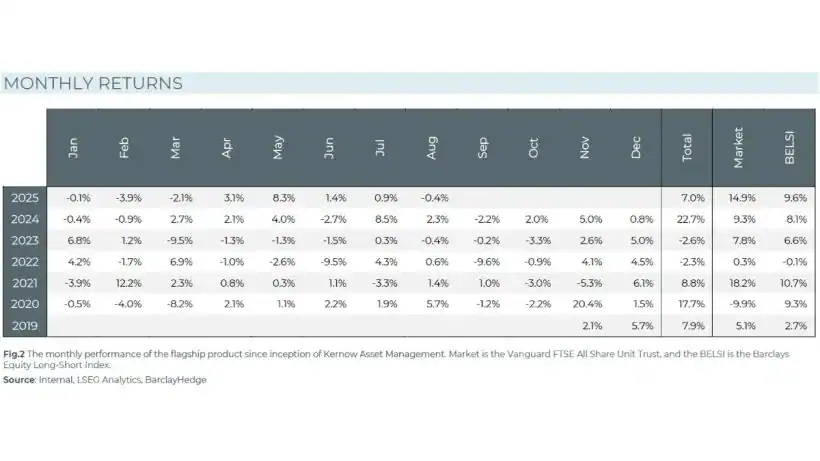

Since its inception in November 2019, the Kernow strategy is up 73%

This compares to the UK equity market, which has increased 52% over the same period. The collective upside in the portfolio is worth more than 226%.

- Book of the month: The Victorian Internet by Tom Standage

- Good month for: Anglo-Eastern Plantations PLC, + 41% on strong financial performance

- Bad month for: WH Smith PLC, -33% after ‘overstatement’ of profits

Cliff Notes

Kernow at Six: An Evening Among Art, Investors, and Ideas

Kernow will host a private evening at the Maas Gallery to mark its sixth anniversary. Set among Sarah Adams’ evocative Cornish landscapes, this invitation-only event will welcome over sixty clients, CEOs from across our portfolio, and the legendary investor Andy Brough.

With access limited, new investors seeking to allocate are encouraged to enquire about availability.

All the best

Alyx Wood

Chief Investment Officer

Kernow Asset Management

Read more hedge fund letters here