GoodHaven Fund's annual letter for the year ended December 31, 2025.

“Once in a while, you get shown the light

In the strangest of places if you look at it right” – Scarlet Begonias by The Grateful Dead

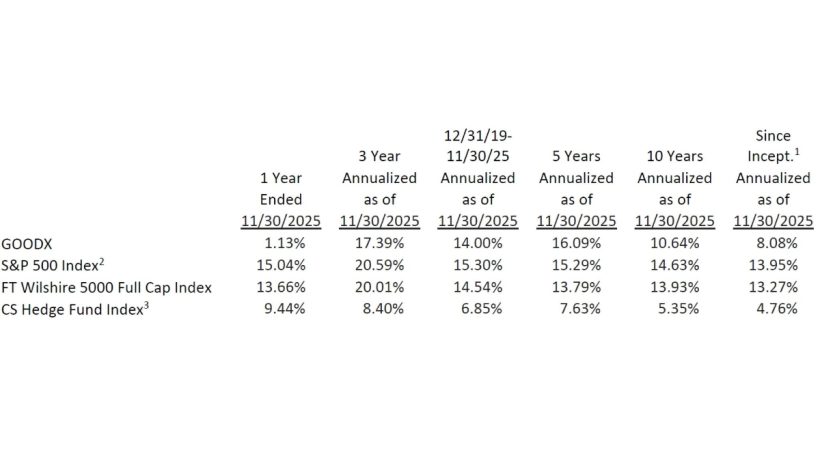

Our long run of consistent outperformance has been temporarily interrupted as we materially underperformed in the 2025 fiscal period. The Fund rose 1.13% while the S&P 500 rose 15.04%.

Our results since the start of GoodHaven 2.0 (12/31/19) through 11/30/25 are a strong annualized total return of 14.00% but now lag the S&P 500’s 15.30% for that period. We feel we have generated these returns while taking less risk than the market overall. While we wonder if there is a perfect “category” for our unique portfolio we note that, according to Morningstar, we continued to rank favorably (at 11/30/25) in the top 6% and 3% of our category for the three year and five year periods respectively.

As we have said consistently over those prior periods of outperformance:

“While this period continues a string of strong results, we take this moment to remind you that our portfolio is managed striving for long-term outperformance, not short-term outperformance. We will underperform the market averages from time to time. We hope you will view such periods when they come as opportunities, as we expect we will.”5

Our fiscal year has always ended in November - with the corresponding semi-annual period ending in May. We have for some time tried to keep our reporting to you simple - commenting on results during such fiscal (versus calendar) periods. It’s a slippery slope to start moving the target after you’ve shot the arrow - and so we’ll stick with our historic approach in the table above. However, it is worth mentioning that our calendar 2025 absolute results fared better than the above with an increase of about 7%. We also continue our historic practice of reporting our results since our internal reorganization some years ago (GoodHaven 2.0) while also referencing a few other relevant indexes.

We had no material realized losses in the period and our companies have overall delivered solid recent business performance – keeping in mind their respective industries. That doesn’t mean we can’t find some internal process flaws in 2025 - we always can, and we always analyze these closely. The upside market potential of many of our holdings now looks even more promising than recently.

We find it’s a useful exercise to look back on some our long-term positions and review what their recent stock prices implied forward valuations were not so long ago, now that we see how earnings have since grown. For example, just two years ago in late 2023, Alphabet’s stock price was trading at an implied 12x what they expect to earn in 2025, Progressive Corporation two years ago was trading at an implied 9x 2025E earnings, and Bank of America was trading at 8x 2025E earnings. Yes, skate to where the puck is going.

As we have said, fiscal quarters seem to now be packing in the range of economic and emotional experiences previously felt over years. The S&P 500 fell over 4% in Q1 2025, and then proceeded to fall an additional approximately 11% in the first eight days of April 2025, before dramatically rebounding since then. In years past, stock prices and financial markets often proved much more volatile than the companies and economies they represented. That feels different today, with the actual economic landscape itself experiencing more genuine volatility than in the past. The White House’s fiscal, economic and geopolitical policies are volatile, unpredictable and fast changing. We feel this is due to some combination of leadership style, a lack of true planning and a desire for periodic chaos. Combine this with financial markets that are now dominated by non-fundamental trading strategies, and this volatility may be the new norm. Our long-term approach of striving to use volatility to help us buy attractive securities and sell those we wish to part with has not and will not change.

Our day-to-day focus on our unique portfolio does not normally change with the economic (or societal) headlines of the day. That doesn’t mean we are not thinking about such things as part of the backdrop our companies operate in and we invest in. Some of the recent prolific headlines involve: tariffs, Artificial Intelligence (AI), affordability and financial market excesses.

It was just last Spring that material uncertainty centered around trade and tariff policies and their economic impact was everyone’s focus. We found the recent Wall Street Journal article - “Why Everyone Got Trump’s Tariffs Wrong” - partially excerpted below - a fun and interesting recap:6

“In the days following “Liberation Day,” the contrast between Trump’s optimism and more dire predictions from trade experts and economists was stark.

As businesses and consumers tried to make sense of the mixed messages, the President doubled down on promises he’d made during his 2024 presidential campaign. “The markets are going to boom, the stock [market] is going to boom, the country is going to boom,” he said on April 3rd.

Economists and business leaders dialed up predictions of a fallout. BlackRock’s Larry Fink said “most CEOs I talk to would say we are probably in a recession right now.” JPMorgan Chase said a global recession was even likely.

An economic collapse hasn’t materialized. Neither has an economic revival.

A lot of federal data is delayed, but the numbers so far show the U.S. economy has held up. The odds of a recession in the coming year have fallen below 25%.

While Trump’s promise on tariff revenues happened to a degree, most of his others have fallen flat. The U.S. has seen little evidence of large-scale reshoring. Cheaper labor abroad continues to give foreign manufacturers an edge, while uncertainty at home over the tariffs has kept many companies from making major investments or bringing manufacturing home.”

We are not taking a victory lap for any macro predictions - we are just reminding you how we strive to always take the long view, not shift the portfolio around unnecessarily over the short-term, and importantly, we strive to use volatility to our advantage. We continue to disagree with many of the administration’s economic policies and approaches, and still worry about their long-term impacts.

On AI - we thought Jeff Bezos said it well recently, as summarized by Bloomberg:7

“Amazon.com Inc. Chairman Jeff Bezos said that the spending on artificial intelligence resembles an “industrial bubble” that could lead to lost investment but will also make society better off.

When people get very excited, as they are today about artificial intelligence for example, is every experiment gets funded, every company gets funded, the good ideas and the bad ideas,” Bezos said, pointing to companies getting billions of dollars of funding before they have a product. “Investors have a hard time in the middle of this excitement distinguishing between the good ideas and the bad ideas.

Still, AI is going to change every industry and improve productivity of “every company in the world,” he said at Italian Tech Week in Turin on Friday. What’s happening currently is an “industrial bubble” akin to the biotech bubble in the 1990s where companies went out of business and investors lost money, but “we did get a couple of lifesaving drugs.” Bezos also pointed to the dot-com bubble a quarter century ago as a frothy investment period that’s benefiting the world today.

Companies building AI as well as the technology around it, from data centers and chips to applications, are receiving enormous amounts of funding. So-called neocloud providers, that provide big technology companies with extra computing power and access to specialized chips for running AI, are being funded even before they’ve built the infrastructure.”

Investigative reporting skills are not needed to locate potential areas of current excess, overvaluation and speculative activity - here are a few fun anecdotes:

“Risk-taking is back for individual investors, and few people have done more to stoke those spirits than the 38-year-old (Robinhood CEO) Tenev. Robinhood’s trading app makes it easy not just to buy and sell ordinary stocks, but to invest in options, cryptocurrencies and other exotic financial products, even to make sports bets and play the prediction markets.”8

“Other recent AI news: Oracle’s stock jumped 25% after being promised $60 billion a year from OpenAI, an amount of money OpenAI doesn’t earn yet, to provide cloud computing facilities that Oracle hasn’t built yet, and which will require 4.5 GW of power (the equivalent of 2.25 Hoover Dams or four nuclear plants), as well as increased borrowing by Oracle whose debt to equity ratio is already 500% compared to 50% for Amazon, 30% for Microsoft and even less at Meta and Google.”

Our biggest detractor in the period was long-time winner Builders FirstSource. Our exposure to single family housing in aggregate, which also includes Lennar and Toll Brothers, was a material sector decliner in the period. We added to our Lennar exposure in the period and more recently established Toll Brothers as a holding. It’s somewhat typical for long-time winners to go through periods of being detractors - especially if the companies have some cyclicality to their businesses.

Our first purchases of Builders’ were in February of 2017 and our average cost is approximately $13 per share. Our returns have been more than satisfactory to date as it closed out the period at $112.23 per share. That journey was not always smooth sailing. Shares declined almost 50% from 12/31/17 - 12/31/18, 55% from 11/29/19 - 03/20/20 and recently 33% from 12/29/23 - 11/30/25. Some of those periods coincided with weaker economic backdrops, some just volatile stock declines, some a bit of both. Many say they prefer “a lumpy 20% to a smooth 15% investment return” but it’s easier said than executed. Single family housing construction and lumber prices, two critical drivers to Builders’ earnings, are experiencing simultaneous downturns. Management continues to execute well and lay the groundwork for continued strong future (though lumpy) returns.

Our next biggest decliner in the period was long-term winner Jefferies. As we wrote after the end of 2024, when Jefferies was a top gainer:

“However, we too have benefited from some of our holdings now trading at higher earnings multiples than previous. We strive to simultaneously think about both the upside and the downside of both the underlying value of our holdings and their market prices in relation to such value. We will normally not sell an attractive long-term holding just because its market price is no longer as cheap as it was or is fairly valued. Cutting the flowers and watering the weeds can be a very counterproductive exercise over time to compound returns, not to mention being tax inefficient. However, we will also seek to avoid holding something we like if we feel the market price has borrowed too much from future performance.”

2025 was really “a tale of two cities” for Jefferies.11 Weaker capital markets and concurrently weaker financial results at Jefferies for the first half of 2025 led to a material stock price decline while solid second half of the year results led to a partial stock price rebound for the year and strong business momentum and potential further upside entering 2026.

Jefferies shareholder and JV-partner SMBC Group recently amended their agreement implying they will increase their Jefferies ownership to 20% from 15% via open market purchases of Jefferies shares.

In October 2025 Jefferies disclosed that through a subsidiary - Leucadia Asset Management – they hold their very manageable (but very high profile) primary exposure to the complex bankruptcy of First Brands. Management’s letter on this sums things up well.

Jefferies shares materially outperformed many of their brethren leading up to 2025 but has lately underperformed that group. We like our upside potential here, assuming a healthy capital markets environment.

Our biggest dollar gainer by far in the period was Alphabet. Lately, it seems like almost everything has gone their way. Judge Mehta’s search remedy verdict was favorable. In September 2025, the court denied the Justice department’s request for Alphabet to sell its Chrome browser for illegally maintaining a monopoly in search, instead the remedies and final ruling allow Alphabet to enter into non-exclusive contracts on a shorter-term basis with its search, AI or Chrome products. Although these behavioral remedies imposed will have an impact on Alphabet, this was a positive outcome compared to the potential structural remedies that could have included a breakup or a forced sale of certain Alphabet divisions. Overall 2025 financial results showed accelerating top line growth and solid margins. Lately Gemini 3.0 - their latest LLM and competitor to ChatGPT - has seen significant market share gains due to its ability to process complex tasks and advanced reasoning capabilities leading to more useful and consistent answers. In the most recent earnings call, the company noted that the scaling of AI Overviews is driving meaningful query growth and with integrated ads and product placement, AI Overview is currently monetizing at the same rate as search. Capital spending continues to increase dramatically. It’s hard not to be pleased with these developments.

Having said that, we did something uncharacteristic and reduced our position in Alphabet in the period, in effect taking profits amounting to approximately two times our entire original cost, while Alphabet remains a material holding. We have written about and executed on the approach of being reluctant to sell (or trim) long-term winners where the fundamental outlook is strong, even if the valuation is no longer cheap. Though we are contrarians by nature, we have lately found ourselves thinking a bit too much about what the digital advertising industry might look like down the road. Our conclusion was that the range of outcomes for Alphabet’s core business was wider than it has been anytime in the decade plus that we have owned it. That does not imply we have a negative outlook, just one that is not as predictable as it has been - which led us to try and mitigate this risk somewhat.

Berkshire was our next biggest gainer in the period. In another selfless act amidst a lifetime of selfless behavior Mr. Buffett, and subsequently the Berkshire Board of Directors, confirmed that Greg Abel has now assumed the CEO role at Berkshire. Mr. Buffett, who at 94 still thoughtfully tackled hours of questions at this year’s meeting, will for now remain Chairman. Contrary to criticisms of Berkshire’s succession plans, this is one of the more well telegraphed plans we’ve seen. Mr. Buffett’s impact as teacher and role model for me and future generations of investors and business people is incalculable - whether you were a Berkshire shareholder or not. For some time, we have focused and articulated our thinking on having Berkshire as a large holding in a post-Buffett and Munger era - which is now upon us. Berkshire’s business results have lately been solid and our returns since we made it a larger holding have been attractive. Berkshire’s optionality for opportunistically deploying its enormous cash resources during a tumultuous future period grows more valuable daily.

By the way, much has been written about the enormous electricity needs domestically to support AI infrastructure growth - as summarized by Ember:

“Electricity demand growth in the US had been near-stagnant for 14 years from 2008 to 2021 (averaging 0.1% per year). However, in 2024, it rose by 3.0% (+128 TWh), following a 1.3% fall in 2023. This marked the fifth highest level of demand growth this century.”

While a myriad of new potential sources of electricity have gained attention lately, we are reminded that Berkshire Hathaway Energy is the 7th largest producer of electricity domestically.

Our biggest purchase by far in the period was to increase our holdings in Chubb. To recap our history with Chubb: our initial purchases were in October of 2020 at about $128/share. This was a few years before Berkshire Hathaway appeared as a material Chubb shareholder. Our thesis at the time for Chubb was centered on continued strong underwriting results, top line growth, higher interest income and an ability to manage the then unknown COVID-era claims uncertainty, and of course what we believed was an undervalued stock price. In subsequent periods, responding to cash needs in our portfolio, we chose to sell our Chubb. It didn’t take us long to regret that and we then reversed course and repurchased our Chubb position. In our view results at Chubb have gone to plan, actually better than plan, and we have continued to opportunistically over time increase our holdings, as we did in the period.

If it seems like recessions have become rarer it’s because - for the moment - they have. As the Economist summed up recently: 15

“In the past four years the world has faced challenges of unusual scope, from higher interest rates and banking crises to trade wars and hot wars. Yet from 2022 to 2024 global real GDP growth was 3% a year on average, and the economy looks set to grind out another 3% this year. Unemployment in the OECD, a club accounting for 60% or so of global GDP, remains near historical lows. In the third quarter of 2025 global company profits rose by 11% against a year earlier, the most in three years.

Aside from a contraction owing to covid-19 lockdowns, the world economy has not suffered a synchronised recession for over 15 years. Perhaps a third of America’s workforce has never experienced a prolonged downturn. This is the good news: slumps exact a tremendous human cost. When the world lives through a “recession recession”, costs begin to mount.

Some suggest an economy needs the occasional downturn to stay healthy. Joseph Schumpeter, an Austrian economist, argued that they provoke “creative destruction". Failing firms leave the market, capital decamps to more promising technologies and workers move to more productive jobs. The result is short-term pain and long- term gain. Schumpeter did not argue that politicians should deliberately engineer downturns. But nor did he think they should try to prevent them. “Depressions are not simply evils, which we might attempt to suppress”, he wrote. They represent “something which has to be done”.

We don’t think recessions are extinct - and always keep that in mind – even if we (nor almost anyone) can predict when the next one will occur.

In addition, our prior concerns articulated here about the worrisome domestic budget deficits and risks to the US Dollar remain and are not improving.

Our answer to the question of how to continue to strive to generate above average returns over time for all of us amidst concerns, excesses and unknowns that are always present, always different and sometimes more extreme than at other times is a consistent one: Assemble a concentrated portfolio of strong companies with attractive fundamentals, management and long-term growth prospects purchased with a material margin of safety. Our appreciation for the impact of a handful of long-term winners can have on a portfolio (and the indexes) was highlighted by the below:

“Hendrik Bessembinder of Arizona State University notes that among listed American firms from 1925 to 2023, most have negative returns. Less than 3% of stocks account for all the increase in shareholder wealth in that time.”

Finally – as a reminder, you’ll notice that we now distribute this letter as a separate document and that the new regulatory format for what was the Semi-Annual and Annual report is now the Form TSR (Tailored Shareholder Report) that can be viewed here: www.goodhavenfunds.com/communications

As of November 30, 2025, my family and I and the team here at GoodHaven Capital Management, LLC, the investment advisor to the GoodHaven Fund, owned approximately 133,019 shares of the Fund. I purchased more shares in the period. It is management’s intention to disclose such holdings (in the aggregate) in this section of the Fund’s Annual and Semi-Annual shareholder letters on an ongoing basis.

I thank all fellow shareholders for their continued confidence as GoodHaven 2.0 continues to unfold. I also thank our Fund Board of Trustees and our long-time partner and investor Markel for their support and wise counsel.

Stay healthy and safe and forward we go.

Larry Pitkowsky

GoodHaven Fund

Read more hedge fund letters here