Gator Capital Management's commentary for the fourth quarter ended December 31, 2025.

Dear Gator Partners:

We are pleased to provide you with Gator Financial Partners, LLC’s, Gator Offshore Partners, Ltd.’s, and Gator Qualified Partners, LLC’s (the “Funds”) 2025 4th quarter investor letter. This letter reviews the Fund’s 2025 Q4 and shares our investment thesis on TFS Financial Corporation.

Review of Q4 & 2025 Performance

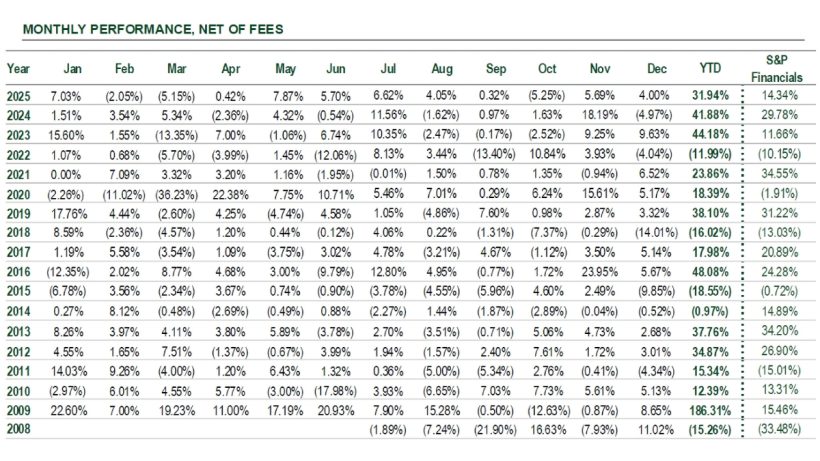

During the 4th quarter of 2025, the Funds had solid performance. We outperformed both the broader market and the Financials sector benchmark. The Fund’s holdings in small and mid-cap Financials outperformed the largest bank and insurance companies again this quarter.

Our long positions in Anywhere Real Estate, Societe Generale, First Citizens Bancshares, Customers Bancorp, and Sotherly Hotels were the top contributors to the Fund’s performance. The largest detractors were long positions in Virtus Investment Partners, Global Payments, and PayPal, and short positions on TD Bank and Citigroup.

During 2025, we had strong performance and outperformed both the broader market and the Financials sector benchmark. The two major drivers were our positions in Robinhood Markets and Anywhere Real Estate.

We entered 2025 with Robinhood as our largest position after it had a strong 2024. The stock had another strong year as the company continued to introduce new products, which drove accelerating growth. We hedged the position throughout the year as the valuation increased and currently have minimal exposure to the stock. One factor in hedging the position is that we are uncomfortable with the regulatory stability of prediction markets. We believe prediction markets have allowed people in non-sports gambling states and people 18-20 years old to gamble on sports through their brokerage accounts because prediction markets are considered exchanges and not casinos.

Anywhere Real Estate was a strong performer in 2025. We originally purchased the stock at $4 in May of 2020. It ran up to $20. We mistakenly added to it at $15 on a pullback and even wrote about it in our 2022 Q1 letter. We completely missed the pullback in the housing market and took our losses in late 2023 at $5. We repurchased the position at $3.29 on the closing print when the stock was kicked out of the Russell 2000 in June 2024. We added to the position several times below $4. Then in Q3 of 2025, the stock started to perk up on the prospects of a housing market recovery. In September 2025, Anywhere agreed to be acquired by its competitor Compass for a 100% premium. It finished the year up 329%. The acquisition by Compass was completed in early 2026, and we now hold Compass shares.

For FY 2025, our top contributing positions were Robinhood, Anywhere Real Estate, Barclays PLC, Customers Bancorp, and Jackson Financial. Our top detractors were our long positions in PayPal, Global Payments, and Virtus Investment Partners and our short positions in TD Bank and JP Morgan Chase. We exited our PayPal position in Q4. PayPal management presented at two conferences during Q4 and talked about continued challenges in the business. We decided to step to the sidelines and watch the next couple of earnings reports.

Investment Thesis on TFS Financial Corporation (“TFSL”)

In December, we purchased a position in TFS Financial Corporation (“TFSL” or “Third Federal”). TFSL is the holding company for Third Federal Savings & Loan, which is a $17 billion bank headquartered in Cleveland, OH. TFSL has a unique corporate structure. It is majority-owned by a mutual holding company, while the public shareholders own a minority stake in the bank. We think the mutual holding company structure can help create superior returns for the public shareholders. TFSL’s stock has underperformed since 2021 due to the increase in interest rates during 2022 and the inverted yield curve. We think the recent decline in short-term rates has helped TFSL turn the corner, but the stock price does not yet reflect this turn.

Before sharing our investment thesis, we share brief background on the mutual holding company structure and the opportunity for shareholders:

Mutual holding companies (“MHCs”) occupy a small but fascinating corner of the U.S. banking landscape. They are few in number, often misunderstood, and structurally complex, all of which repel generalist investors but attract us due to the leveraged structure, capital optionality, and embedded catalysts. For investors familiar with bank valuation, capital ratios, and consolidation dynamics, the MHC structure presents a unique blend of conservatism and asymmetry. The opportunity lies not in financial engineering, but in disciplined capital allocation, management incentives, and the intelligent use of time.

Before discussing MHCs specifically, it is helpful to briefly review the more familiar traditional mutual-to-stock conversion model that many bank investors actively seek out. A traditional mutual bank is owned by its depositors rather than shareholders. Depositors technically control the institution, though in practice governance is largely delegated to a self-perpetuating board. Mutual banks tend to grow slowly through retained earnings, operate conservatively, and lack access to public equity markets for capital or acquisitions.

In a full conversion, the mutual bank demutualizes entirely and becomes a conventional publicly traded bank holding company. Depositors receive subscription rights in the IPO, the mutual ownership is extinguished, and public shareholders own 100% of the institution from day one. Governance, capital allocation, and strategic control fully transition to the public company model. The IPO proceeds flow into tangible equity and are not paid out the depositors. Adding the IPO proceeds to the existing equity creates significant excess capital relative to the bank’s immediate growth needs. And, the new stock is priced at a discount to tangible book value. Management typically works down the excess capital over several years through a combination of organic loan growth, opportunistic share repurchases, modest dividends, and occasionally small acquisitions. As capital normalizes and profitability improves, the stock often rerates toward peer multiples. Ultimately, many of these institutions become attractive acquisition targets for larger banks, generating an additional valuation uplift. Investors are drawn to this model because it offers a clear playbook: discounted IPO pricing, strong tangible book value support, capital deployment catalysts, improving ROE over time, and a high probability of eventual sale.

Mutual holding companies represent a variation on this familiar framework but introduce additional leverage, optionality, governance complexity, and time arbitrage.

What Is a Mutual Holding Company?

A mutual holding company structure, by contrast, arises when a mutual bank executes a partial conversion rather than a full demutualization. Instead of selling 100% of the institution, the bank forms a mutual holding company that retains majority ownership, usually 51% to 70%, while selling a minority stake to public shareholders through an IPO.

The operating bank becomes wholly owned by a newly created public holding company, while the mutual holding company owns a controlling stake in that publicly-traded entity. Depositors remain indirect owners of the mutual holding company, preserving mutual control and influence. Public shareholders receive minority economic ownership and liquidity, but limited governance control.

Economically, both full conversions and partial conversions raise capital and increase tangible equity. The critical difference is that in a partial conversion, minority shareholders effectively own a levered economic interest in the bank’s equity and earnings, because a significant portion of the equity base is owned by depositors through the mutual holding company rather than by other public shareholders. Usually, mutual holding companies will waive their rights to dividends. Also, because anytime the mutual holding company sells shares, the proceeds go to the bank, the minority shareholders effectively have a leveraged stake in earnings and equity of the bank. Growth in tangible book value and net income accrues disproportionately to the minority float, magnifying per-share value creation when the franchise performs well.

This embedded leverage also creates asymmetry around the eventual second-step conversion, when the mutual’s retained stake is monetized and ownership normalizes. Importantly, stock repurchases further increase this embedded leverage. When shares are repurchased below the implied tangible book value based on minority shares, the remaining minority shareholders gain a larger proportional claim on slightly smaller underlying equity base. Over time, disciplined buybacks can meaningfully amplify per-share tangible book growth and earnings power for minority investors. In effect, well-managed MHCs allow patient investors to compound a levered claim on a growing bank franchise.