Apis Flagship Fund commentary for the second quarter ended June 30, 2025.

Dear Partners,

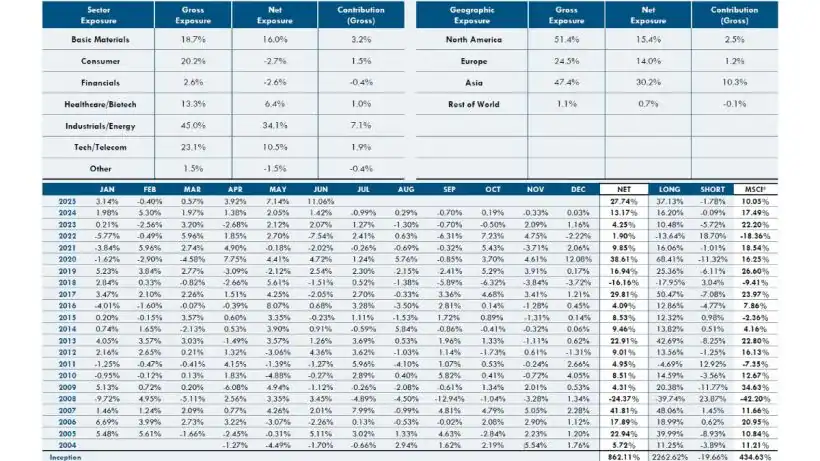

The Apis Flagship Fund was up 23.7% net in Q2 2025. During the past quarter, our longs contributed 35.9% (gross) and our shorts detracted 4.9% (gross). At the end of June, the Fund was approximately 60% net long with the portfolio 92% long and 32% short.

Performance Overview (Gross Returns)

Q2 2025 was an excellent one across all Apis strategies, with broad-based contributions across regions and sectors. Long positions were the primary driver of returns, though our short book also generated meaningful alpha, appreciating significantly less than the broader markets.

Asia stood out as a major source of performance, contributing approximately 18.0% for the Flagship strategy, with South Korea leading the way. As highlighted in the chart below, Korea has been a long-term underperformer – lagging the S&P 500 by 50.0% over the past four+ years – offering compelling opportunities for differentiated stock selection.

Following the initial rally driven by Trump’s capitulation on tariffs, the Korean market received an additional boost from the so-called “Lee Jae-myung bump” after the DPK party’s victory in early June elections. Lee’s platform – centered on corporate governance reform and fiscal stimulus – was well received by investors. Coupled with strong earnings growth, attractive valuations, and a long stretch of underperformance, one can make a reasonable case for further upside in Korea.

Beyond Asia, both Europe and North America contributed meaningfully to performance, each adding approximately 5.0% during the quarter.

Industrials continued to lead all sectors, contributing approximately 18.0% to returns, with particularly strong performance in defense and power generation/distribution. Stock selection remained strong across the board, with all major sectors contributing positively. Technology also rebounded from a weaker Q1, as several AI-related names recovered losses tied to the DeepSeek-driven sell-off.

Looking at specific names, four of our top contributors in June – each adding 2.0 to 4.0% – were Korean names, led by Doosan Enerbility. Often described as a mini-GE, Siemens, or Hitachi, Doosan is exceptionally well positioned to benefit from the global resurgence in nuclear energy. Other notable Korean contributors included previously highlighted names such as Poongsan and Hyundai Rotem in defense, and Iljin Electronics, a key player in power transformer manufacturing.

On the detractor side, GEO Group was the largest drag on performance, costing the portfolio about 90 bps as immigration deportations faced renewed political resistance. However, the recent passage of the "Big, Beautiful Bill" should provide a tailwind for GEO going forward.

Shorts detracted modestly overall, largely due to broad market strength, with the largest losses coming from the strongest-performing markets. Three Korean short positions were among the top detractors, though individual losses were contained to 15 to 30bps each.

Portfolio Outlook And Positioning

Looking ahead to the second half of 2025, there are several portfolio themes and unique idiosyncratic opportunities that we believe will continue to drive performance.

Defense remains one of the most structurally supported sectors globally. Following decades of underinvestment, defense budgets are expanding meaningfully across regions. At the same time, the emergence of next-generation technologies –drones, counter-drone systems, directed-energy weapons (like Iron Dome/Giant Dome platforms with integrated lasers), and space-based defense applications – is creating new markets for smaller, specialized companies. In some cases, firms with previously overlooked defense-related divisions (such as NOF, highlighted below) are now gaining investor attention.

The space industry is another area of growing interest, with a growing ecosystem of companies supporting both consumer and military applications. We are finding attractive opportunities across the value chain – from component manufacturers to service providers enabling satellite-based capabilities.

Power infrastructure, like defense, is an area marked by years of chronic underinvestment. While China has aggressively expanded its power capacity and grid modernization, many Western markets have lagged behind. If power is the critical enabler of AI and digital infrastructure (as we believe), this imbalance presents a significant investment opportunity as the West plays catch-up.

On a related note, nuclear energy is experiencing a global resurgence – a trend that continues to benefit Apis, given our early positioning in top nuclear-exposed names outside the U.S., including in Korea, Japan, and France. Much like defense, nuclear was long excluded from ESG frameworks, allowing us to invest before sentiment and policy began to shift more favorably.

European infrastructure is another supportive theme. As noted in our previous letter, multiple infrastructure spending bills have now passed, directly benefiting several portfolio holdings tied to energy, construction, and heavy industry across the region.

“Trump Trades” also present emerging opportunities. These include positions that benefit from stricter immigration enforcement, a weak dollar or higher interest rates, such as Gold where we have a roughly 8.0% allocation to some mid-cap gold miners, which are growing earnings at attractive valuations (typically 3–4x P/E on current gold prices). Mining services companies are similarly poised to benefit from rising commodity prices. U.S. distressed REITS will continue to struggle if rates remain stubbornly high. Other “Trump Trades” we’re monitoring include the MAHA movement (“Make America Healthy Again”) as scrutiny intensifies on Big Food and Big Pharma, resulting in potential winners and losers.

Meanwhile, the return of speculation (yes, SPACs are back!) and growing retail/quant involvement only seems to expand its influence in the markets. For those who tread carefully, there’s no shortage of overhyped concepts – quantum computing being one recent example – where we see clear signs of excess and potential implosion (refer to our write-up below).

Outside of these broader themes, we remain focused on idiosyncratic opportunities with strong return potential, including Magnite and NOF, which we explore further in the section below.

Investment Highlights

Magnite, Inc. (U.S. – $3 billion market cap)

Magnite Inc (NASDAQ:MGNI) is one of the largest independent sell-side platforms (SSPs) – effectively serving as enterprise software for digital publishers, including websites and connected TV channels. Its platform enables publishers to manage ad serving, optimize yield, and target audiences more effectively by connecting their ad inventory to a broad network of demand partners.

In return, SSPs earn a percentage of ad spend flowing through their platforms. Magnite benefits from deep integrations with publishers and demand-side platforms, creating high switching costs and a durable competitive moat. The company is widely recognized for its fast, reliable technology infrastructure.

Two major trends are reshaping the digital advertising landscape. First, ad budgets continue to shift from traditional linear TV to Connected TV (CTV) as platforms like Netflix and others expand their ad-supported offerings. Second, a recent antitrust ruling against Google may significantly alter the dynamics of the open web advertising market – specifically for video and display ads on browser-based websites. The court found Google had engaged in anti-competitive practices, and a follow-up hearing this September could result in structural changes that benefit independent ad tech providers.

CTV now represents approximately 50% of Magnite’s revenue, with the segment expected to grow at a 15% CAGR over the medium term. The company is well-positioned to outpace this growth thanks to their scale, deep publisher relationships, and strong technology platforms. In mid-2024, Magnite was named Netflix’s exclusive ad tech partner, positioning it to benefit as Netflix targets $9 billion in ad revenue by 2030. In the open web advertising market, Google maintains a dominant 60% share, compared to 7% for Magnite. Despite its relatively small share, open web ads still account for approximately 40% of Magnite’s revenue. A meaningful shift in market share following the recent antitrust ruling could serve as a powerful catalyst, with potential double-digit revenue growth beginning in 2026.

To illustrate the upside: each 1% shift in market share away from Google would translate into an estimated $50–75 million in high-margin revenue (with about 90% incremental margin) – equivalent to roughly half of Magnite’s 2024 EBITDA. At current valuations – 15x forward EBITDA for Magnite – we believe this embedded optionality is not yet priced in, and the stock could offer 50–100% upside from current levels.

NOF Corporation (Japan - $4.6 billion market cap)

NOF Corp (TYO:4403) is a Japanese company with a compelling investment profile: a stable, cash-generative core business in functional chemicals, supported by high-growth segments in cosmetics and pharmaceuticals. These segments are driving both top-line expansion and margin improvement. Despite this favorable mix, the company continues to trade like a basic chemicals business at just 17x earnings. With leading market positions in faster-growing, higher-margin niches, we believe NOF is well-positioned to deliver double-digit growth for years to come, and that the market has yet to fully reflect this structural shift in its valuation.

In the near term, cosmetic surfactants – which account for approximately 20% of NOF’s sales and 25% of profits – are poised to drive meaningful upside, following a recent doubling of production capacity. NOF operates as an original design manufacturer (ODM) for leading cosmetic brands, including Ryohin Keikaku (popularly known as Muji). The cosmetics segment grew 36% last year, fueled by Ryohin’s success and continued store expansion, particularly in China. With sustainable double-digit revenue growth and operating margins of 25% or higher, the cosmetics business is well-positioned to support 1–2% annual expansion in group-level margins over the next few years – a key driver of long-term value creation.

NOF also has clear visibility into long-term, sustainable growth through its Pharmaceutical and Drug Delivery Systems (DDS) platform, which now accounts for about 20% of sales and 35% of profits. Like the cosmetics segment, DDS recently doubled its production capacity to support future demand. The company holds a 60% global market share in polyethylene glycol (PEG) – a key drug additive that enhances stability and prolongs therapeutic effects. In addition, NOF is rapidly scaling its capabilities in lipid nanoparticles, a critical delivery technology for nucleic acid-based therapies (RNA, DNA) and other next-generation treatments. While still in the early stages, the lipid nanoparticle market is projected to grow at a 40% annual rate, positioning NOF to benefit from secular growth well into the 2030s.

A final growth catalyst lies in NOF’s explosives division, which represents approximately 10% of sales and holds a 100% market share in Japan for rocket propellants used by the Self-Defense Forces (SDF). While the company provides limited disclosure on this segment, it recently announced a doubling of capacity to meet rising demand. However, with captive customers like IHI ramping up missile and rocket production by several multiples, even this expansion is unlikely to fully meet growing needs – suggesting continued upside and strategic importance for this niche, high-barrier business.

NOF is also making encouraging progress on corporate governance. While the introduction of a formal Investor Relations function and explicit shareholder return policies may seem like modest steps, they represent meaningful improvements for the company. With only two analysts currently covering what is otherwise a well-established “mid-cap” company, we believe there is still significant discovery and re-rating potential as governance standards improve and investor visibility increases.

Quantum Noise

Quantum computing has emerged as a notable theme in our short book, particularly as a handful of SPACs have entered “meme stock” territory amid hype surrounding the technology – some trading at over 250x sales! While we share the broader optimism about quantum computing’s long-term potential and are closely monitoring global developments (including the race with China to perfect it), we’re also cautious about the growing number of public companies exploiting the complexity of the science to inflate their narratives.

Several of these companies are pursuing approaches widely viewed by experts as technological dead ends. Nonetheless, they continue to issue grandiose press releases while generating minimal revenue, typically limited to early-stage trials and prototypes. We believe this disconnect between fundamentals and valuation presents a compelling opportunity on the short side.

While serious quantum computing efforts are underway at tech giants like IBM, Google, Intel, and Microsoft, none claim to be close to commercialization. IBM, for example, recently committed $30 billion over five years to quantum R&D. The others are reportedly spending close to $1 billion annually on their programs – yet even the most optimistic projections place a commercially viable quantum computer 5–10 years away.

In stark contrast, a handful of SPAC-backed quantum companies claim to have already achieved commercialization – despite skeleton R&D budgets and limited technical transparency. These companies are aggressively burning cash and repeatedly tapping markets via at-the-market (ATM) offerings, capitalizing on inflated valuations. Many also exhibit troubling patterns of management turnover, insider selling, and vague or evasive commentary about their underlying technology. We believe this disconnect is unsustainable. As investor scrutiny increases, we expect these stocks to fall back to earth once the market gets wise to their tendency to overpromise and underdeliver.

A recent illustrative – and comedic – moment at CES in January underscores the growing skepticism: when asked about the timeline for quantum breakthrough, Nvidia CEO Jensen Huang said he doubted if a useful quantum computer would hit the market within 15 years, and that 20 years was a more realistic timeline. When asked about his comments negatively affecting the public quantum stocks, he quipped, “How could a quantum computing company be public?”

As always, we encourage your questions and comments, so please do not hesitate to call our team here at Apis or Will Dombrowski at +1.203.409.6301.

Sincerely,

Daniel Barker,

Portfolio Manager & Managing Member

Eric Almeraz,

Director of Research & Managing Member

Apis Flagship Fund

See the Q2 2025 Factsheet here.

Read more hedge fund letters here