If 2018 has taught investors anything, it’s that keeping all your investments in one market and falling victim to home country bias – even if that market is the U.S. – is a big risk.

Q3 hedge fund letters, conference, scoops etc

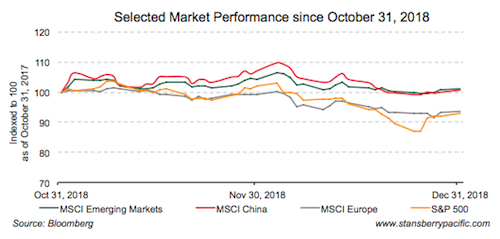

As you can see in the chart below, stock markets all over the world did poorly in 2018…

Emerging markets suffered the most in part because of the ongoing trade war between the U.S. and China.

This led to a strong net outflow of foreign institutional investment (FII) from the region. This is when foreign investment in a country’s stock market and debt market are sold more than they’re purchased, which results in money leaving the country overall.

According to ANZ Bank, emerging markets in Asia experienced a net FII outflow of US$26.1 billion from January to November. That put 2018 on track to be the worst year since 2008 (when outflows hit US$63.4 billion).

Of emerging markets, China’s fell the most last year. The Shanghai Composite Index declined by 25 percent because investors are anticipating a sharp slowdown in the economy. We’ve written before about how manufacturing will remain weak in the early months of 2019, and that you should expect a bad first quarter for China’s economy.

It’s also going through one of the sharpest property market downturns since the global economic crisis. This downturn was a direct result of Beijing’s policies to rein growth in property prices, which had started to reach levels well beyond what ordinary citizens could afford.

Asian stock markets with deep ties to China’s manufacturing supply chain, including Singapore, Malaysia and Indonesia lost 8.8 percent, 5.3 percent and 7.1 percent, respectively, during the year. Japan’s Nikkei 225 Index fell 8.6 percent. (All of these figures are in U.S. dollar terms.)

The MSCI Europe Index held its ground through September, but ended the year down 10.1 percent. Uncertainty about Brexit, debt woes in Italy and the slowing German economy hurt sentiment.

U.S. markets, which until September were the world’s strongest performers, caved to the pressure of trade uncertainty and rising interest rates.

The S&P 500 and Nasdaq closed the year down 7 percent and 5.3 percent, respectively. Both are close to bear market territory (when prices fall 20 percent from their highs).

There were some bright spots

Not all markets were losers in 2018.

India ended the year down 4.2 percent thanks to pro-business government policies and an infrastructure boom. Everything from automobiles to smartphones are experiencing rapid growth in demand.

Russia did even better – its stock market fell 1.9 percent in 2018. Its market was buoyed by a surge in oil and natural gas prices during the first 10 months of 2018 (Russia generates 70 percent of its exports from petroleum products).

The best-performing emerging market was Brazil, which eked out a gain of 0.2 percent for the year. The country has recovered steadily from a two-year recession (2014 to 2016), and got a boost from the trade war as China shifts purchase of soybeans from the U.S. to Brazil. It also elected a new president, Jair Bolsonaro, who rode to victory on a platform of stomping out corruption and crime in the world’s eighth-largest economy.

Investors who owned only India, Brazil and/or Russia last year emerged almost unscathed. But for the most part, 2018 was a forgettable year for global investors.

Three reasons emerging markets could outperform in 2019

Emerging markets fell earlier and faster than developed markets in 2018. But they also bottomed earlier.

In November, emerging markets had experienced their strongest positive inflow of foreign funds for the year, according to Bank of America Merrill Lynch.

From October 31 to the end of the year, the MSCI Emerging Market index rose 1.2 percent. That compares with a 7.2 percent decline in the S&P 500 and a 7.3 percent fall in the MSCI World Index during the same period.

Whether this will continue into 2019 depends on three things:

- Low valuations of emerging markets. This is primarily shown by the cyclically-adjusted price-to-earnings (CAPE) ratio, which for emerging markets currently stands at 14.9 times.

Even with the steep declines in developed stock markets in recent months, their CAPE ratio remains elevated at 24.3 times. The 38 percent discount of emerging markets from developed markets is low considering developed market volatility.

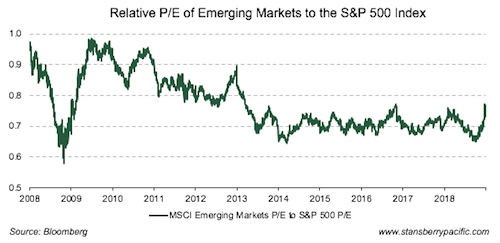

Moreover, emerging market stock valuations in October hit their lowest levels relative to U.S. stocks since the global economic crisis in 2008-2009.

The chart above shows the average price-to-earnings (P/E) ratio of the MSCI Emerging Markets Index relative to the P/E of the S&P 500 over the last 10 years. As the number gets closer to 1.0, it indicates valuations are becoming similar. As the number falls below 1.0, emerging market valuations are becoming cheaper relative to the S&P 500.

While emerging market valuations today aren’t as cheap as they were back in October – due largely to the decline in developed markets – they remain low on a historical basis.

- Strong and sustainable growth. We’ve written previously about two main drivers of economic growth: population and productivity.

Emerging markets are experiencing growth in both of these areas. Combined, this will deliver two to three times the rate of economic growth in developed markets over the next five years. China alone is growing at a rate of 6.5 percent – more than double the U.S. economy’s growth.

- Pace of U.S. interest rate hikes to slow. One of the biggest triggers of the emerging market downturn in 2018 was the precipitous rise in U.S. interest rates. Higher guaranteed returns from U.S. debt instruments make alternative investments less attractive.

But U.S. President Donald Trump has been openly criticising the Federal Reserve for being too aggressive on monetary tightening (i.e., raising interest rates), claiming it endangers economic growth and stock market prices.

And on December 19 (after hiking interest rates a fourth time in 2018), Federal Reserve Chairman Jerome Powell indicated that future rate hikes would be lower than previously planned.

That’s helped push the yield on the benchmark 10-year U.S. Treasury from 2.81 percent to 2.68 percent in just two weeks – down to its lowest level since January 30, 2018.

So we have a situation where emerging markets are trading at a large discounts to U.S. stocks. Meanwhile, emerging market economic growth is racing ahead. At the same time, the return generated from holding U.S. dollars is going down, increasing the appeal of emerging market investments.

So emerging markets should be on your radar in 2019. Start the new year by making sure you have some exposure to this beaten down – but recovering – sector of the global stock market.

Good investing,

Brian Tycangco

Editor, Stansberry Pacific Research