Apis Flagship Fund commentary for the first quarter ended March 31, 2025.

Dear Partners,

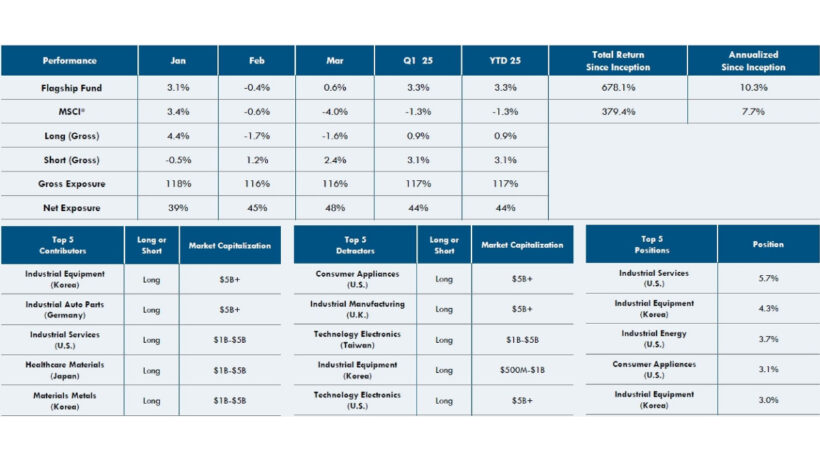

The Apis Flagship Fund was up 3.3% net in Q1 2025. During the past quarter, our longs contributed 0.9% (gross) and our shorts also contributed 3.1% (gross). At the end of March, the Fund was approximately 48% net long with the portfolio 82% long and 34% short.

Read more hedge fund letters here

Performance Overview (Gross Returns)

2025 is off to a good start for our Flagship Fund, with positive returns during Q1 across both longs and shorts. Regionally, the story for the quarter was strong outperformance in Europe, which saw impressive market performance (up...