FPA Capital Fund commentary for the first quarter ended March 31, 2018.

H/T Dataroma

[timeless]

Q1 hedge fund letters, conference, scoops etc

For the fiscal year ending and quarter ending on March 31, 2018, the fund was down by -4.05% and -2.65%, respectively. In many cases, our companies’ earnings have grown, but because their share prices have not kept up with earnings, their multiples have compressed.

Our largest detractor for the last fiscal year 2017 was Babcock & Wilcox (BW). We have discussed our investment in BW in detail in our first quarter and third quarter 2017 letters.1 BW, after a successful 100-year run with few missteps, managed to incur significant charges from half a dozen projects in a short period. We exited the position in August 2017 because it no longer fit our investment criteria. Another area that detracted from our performance was energy. We believe we are in the early stages of another historic multi-year oil bull market and explained our rationale in detail in our fourth quarter 2017 letter.2 In summary, our energy investment is not just tied to our belief that oil prices will go higher. We also see that extreme investor bearishness has caused oil-related equity performance to disconnect from crude oil commodity performance. As we said in our previous investor letter, we expect our energy shares to benefit from both continued earnings acceleration and a likely multiple re-rating as the performance gap between crude oil and crude oil equities closes over time.

As Founder Retires, GGHC Ends 2017 On High Note, Aided By Mega Telecom Bidding War

On the positive side, in fiscal year 2017 Aaron’s Inc. (AAN) was our largest contributor to performance followed by Allegiant Travel Company (ALGT). AAN is an RTO (rent-to-own) operator. It serves the part of the population that does not have immediate access to credit via its company-owned, franchised locations, and its Progressive brand (virtual). The Company had strong results in 2017, where it beat its revenue and earnings per share (all record results) guidance and raised 2018 guidance across the board. ALGT is an ultra-low cost domestic airline focused on underserved routes. Their results were robust with revenues at the high end of the recently revised (upward) range, better than expected fixed fee and other revenue, and lower than expected unit operating cost on lower maintenance & repair expenses.

As we finish another fiscal year, our 35th, we would like to report our progress on the three portfolio management initiatives we committed to since FPA announced that I would become the sole Portfolio Manager of the FPA Capital Fund (the “Fund”) at the beginning of the fourth quarter of 2017.

1. Avoid position inertia

2. Be more nimble

3. Differentiate between long-term and opportunistic investments

Avoid position inertia:

Our team has been busy transitioning the portfolio. Since the announcement, we have initiated eight new positions and eliminated seven holdings. To put this level of activity into perspective, over the preceding seven years, we invested in an average of four new names per year. It is important to note that our in-depth research process remains intact. We believe we are doing a better job in cutting our work short when the opportunity is not there, which allows us to look at more companies. Also, having just one portfolio manager has streamlined our decision-making process. Because our purchases more than offset our sales, the portfolio’s cash level decreased from 32.0% when I took over on Oct. 1, to 26% at the end of first quarter 2018.

Be more nimble:

We have focused on adjusting position sizing when there are changes in our analysis and the risk/reward profile. Here are a few examples of what we have done since the portfolio management change announcement:

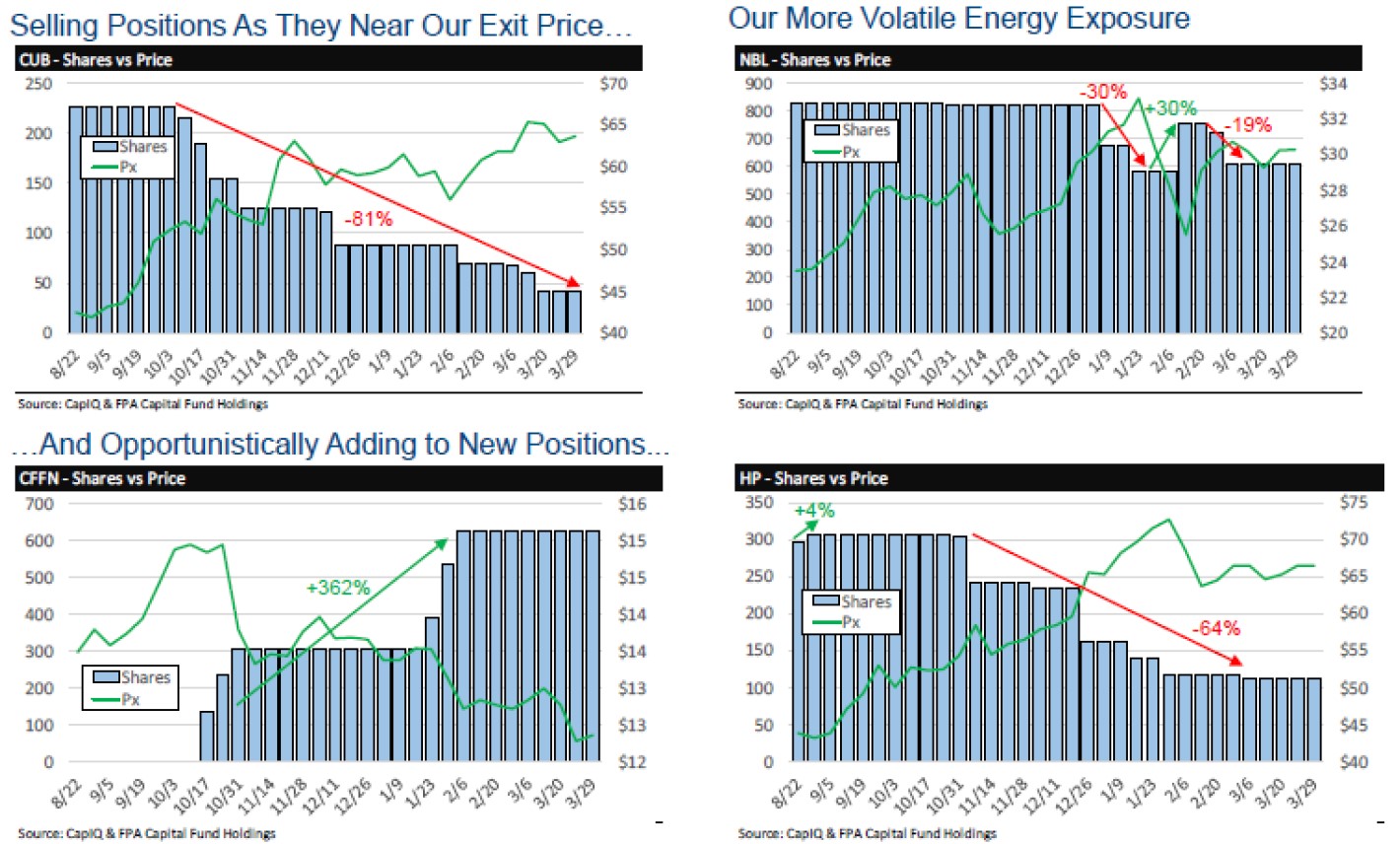

As shown above, we cut our position in Cubic (CUB) by more than 80% as our thesis played out and the stock price approached our target price. We also added opportunistically to one of our newer positions, Capital Federal Financial (CFFN), as the risk/reward ratio got more attractive, allowing us to lower our average cost basis while collecting a very attractive dividend yield. Finally, as you can see on the right side of the above chart, we have been taking advantage of the volatility inherent in our energy positions, and we will look to opportunistically adjust our position sizing to take advantage of these swings. Of course, there can be no guarantee that such strategies will be successful in the future, and past performance does not guarantee future results.

Differentiate between long-term and opportunistic investments:

Going forward, you should expect your invested capital to reflect a higher allocation to long-term core holdings in businesses that we view as having strong competitive positions in stable or growing industries at attractive valuations. We believe increasing the Fund’s weighting to these businesses is especially important during the later stages of the economic cycle, since the larger allocation seeks to mitigate downside risk and in our view increases the likelihood of generating long-term market outperformance.

At the same time, we intend to reserve some room for opportunistic investments in lower-quality businesses, particularly when valuations are at extreme levels. We believe flexing this higher-beta segment of the portfolio during times of market distress also enhances full-cycle returns. In keeping with our philosophy of seeking to minimize downside risk, we will always seek to ensure such investments have ample balance sheet strength to minimize thesis duration risk. Right now, our offshore energy investments are a perfect example of this.

Additionally, we have tightened our process to avoid a permanent loss of your capital by generally sidestepping opportunities that require a correct call on industry cycle timing and identifying where consensus is categorically incorrect about a secular decline theme. The margin for error on such a thesis is very small, while the consequences of getting things wrong can be devastating.

Finally, we would like to point out that we have enacted a process to score our portfolio and pipeline companies on a quality ranking (“1” being highest, and “3” being the lowest) and we are able to track these metrics in the aggregate. A company’s quality score reflects our historic framework (market leadership, history of profitability, solid balance sheets, and high-quality management teams) as well as aspects like industry quality assessed via Porter’s Five Forces.4 Importantly, the entire FPA Capital team reviews and debates each company’s score. Since I became the sole portfolio manager of the Fund, the positions we have sold had an average score of 2.5, while the positions we have initiated have an average score of 1.9. We will continue to update you on this facet of the ongoing portfolio transformation.

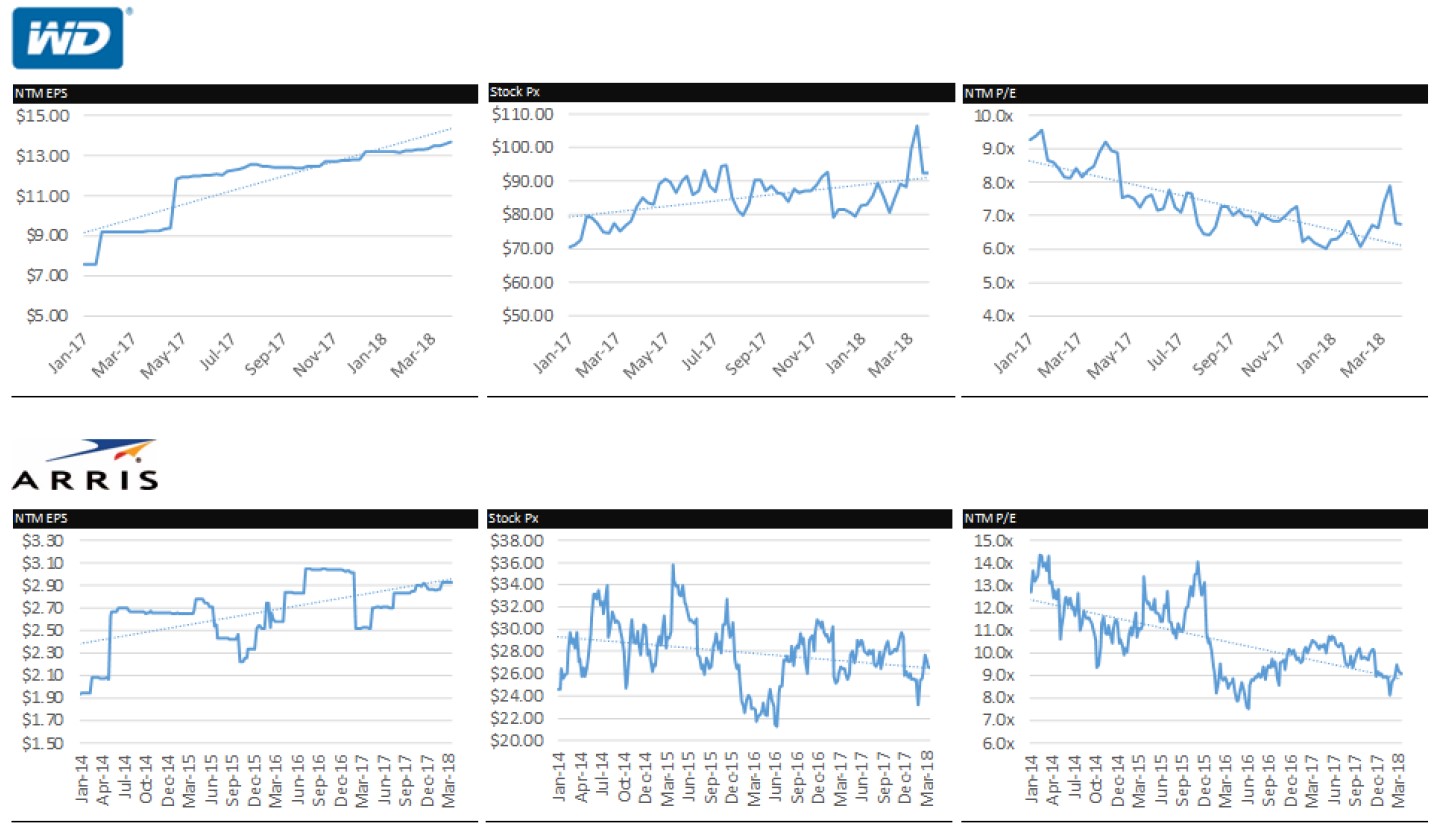

Our portfolio has gotten cheaper:

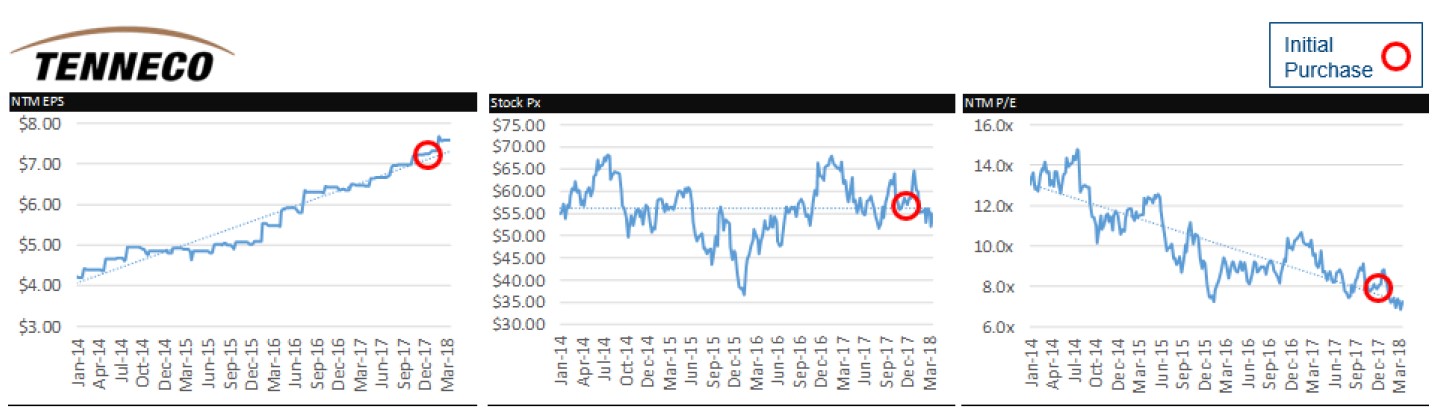

In many cases, our companies’ earnings have grown, but because their share prices have not kept up with earnings, their multiples have compressed. That phenomenon can be seen in the charts below for Western Digital (WDC) and Arris International (ARRS) and is especially prominent in the chart for Tenneco (TEN), one of our latest investments. The charts below show each issuer’s earnings per share (a measure of profitability), price to earnings ratio (a measure of valuation that compares profitability to the stock price), and stock price.

As shown above, Tenneco has done an exceptional job delivering earnings growth, yet the stock has been flattish, producing multiple compression. The bear thesis equates adoptions of electric vehicles with the demise of Tenneco’s Clean Air division. We think this view is an oversimplification and underestimates the growth in clean air content per vehicle as environmental regulations continue to tighten. Furthermore, we believe battery-only vehicles will represent only a tiny fraction of vehicles sold, and that the shift to electrification will start with hybrids—and those still require a substantial amount of clean-air technology. We believe Tenneco will continue delivering organic top-line growth, even stronger bottom-line growth, and ultimately, we think the market will decide that an 8x P/E multiple is insufficient given these metrics.

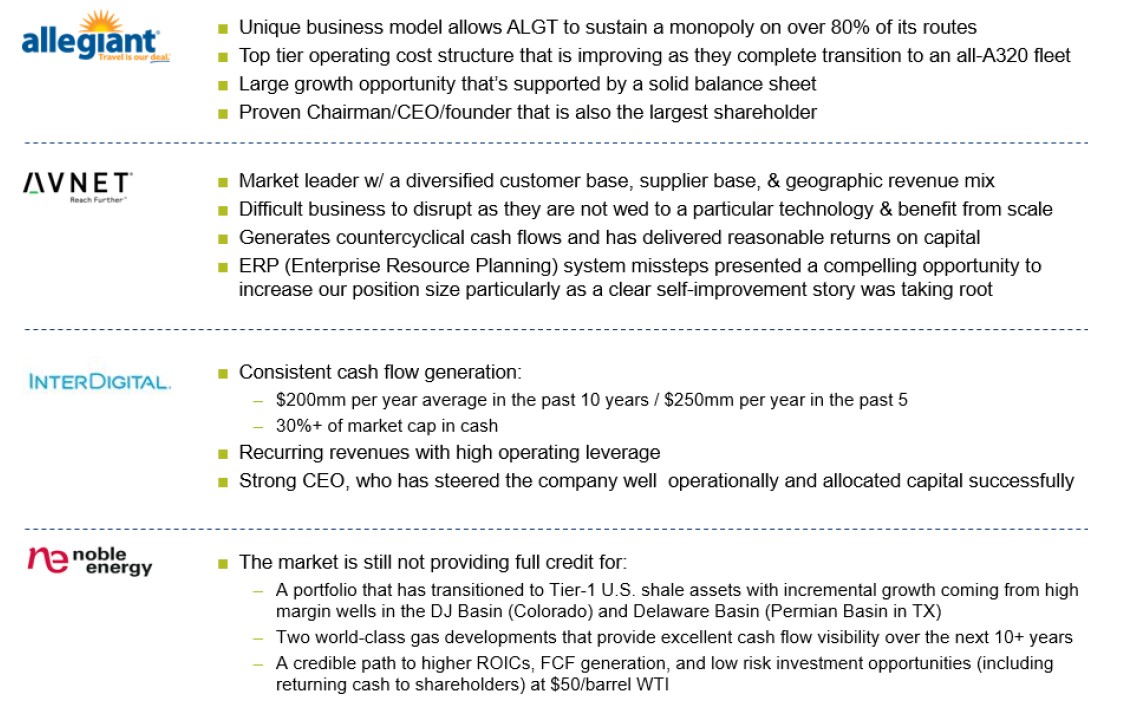

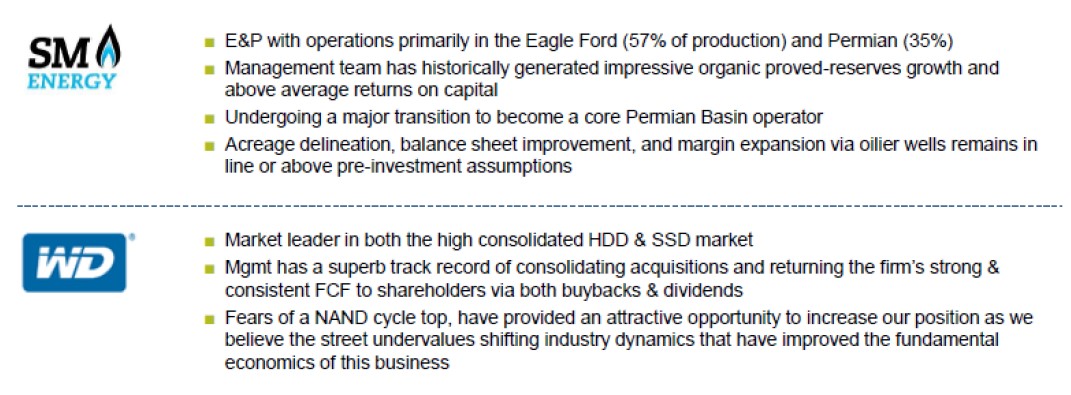

We believe that our largest positions have significant upside potential. Below you can see a quick summary of our thesis for our largest six positions:

We are excited about the current state of our portfolio. Despite near-peak valuation levels in the market, in our view, we have been able to construct a portfolio that is defensively positioned. Our portfolio is trading at earnings multiples that are substantially lower than those of the Russell 2500 Index. We believe that our largest positions, as described above, have substantial upside potential. Moreover, our 26% cash position provides us with great optionality to take advantage of volatility.

In conclusion:

We have been diligently carrying out our commitment to our shareholders. Our goal is threefold: First, we want to avoid position inertia and not hold portfolio holdings past their prime. Second, we will seek to be more nimble. We took steps to accelerate both idea-generation and portfolio execution. And finally, we will seek to do a better job in differentiating between long-term and opportunistic investments. We have made significant changes to the portfolio over the past seven months. Our investments include many strong-but-cheap names. I have increased my ownership in the Fund and expect to continue to add to it.

We appreciate your continued trust in our team and our process.

Respectfully submitted,

Arik Ahitov – on behalf of the FPA Capital Fund Team

Portfolio Manager

March 31, 2018

See the full PDF below.