Many advisors use historical data to project expected returns for U.S. stocks and bonds. But a close look at the historical data suggests that the excess performance of stocks relative to bonds occurred mainly in two historical periods and has been much less consistent over the last 25 years. Advisors illustrating the decision to increase investment risk to fund future goals should acknowledge the possibility that the historical equity risk premium may be lower – indeed, low enough to no longer be considered a puzzle by financial economists.

Q2 2022 hedge fund letters, conferences and more

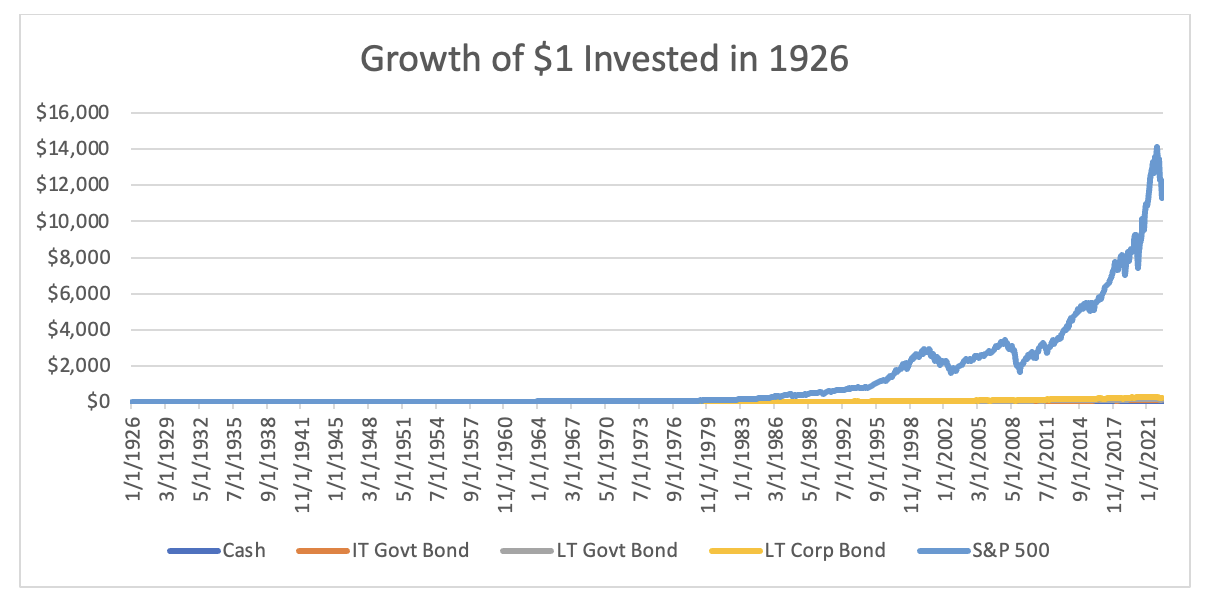

We’ve all seen the graph that compares historical stock and bond performance since 1926 using Ibbotson/Morningstar data:

The graph shows the dramatic performance of stocks compared to bonds over the last 95 years. Advisors show the graph to clients to explain why increasing investment risk pays off over the long run, and how they can provide value by creating portfolios that harness the power of equities.

The outperformance of stocks over bonds is a mystery to financial economists who refer to it as the “equity premium puzzle.” Between January 1926 and June 2022, the arithmetic average return on the S&P 500 was 11.43%, while the average return on intermediate-term Treasury bonds was 4.91% and T-bills returns were just 3.2%. Richard Thaler, who recently won a Nobel Prize in economic sciences, co-authored a widely-cited paper in 1995 that explained low stock ownership among individual investors as a behavioral anomaly driven by the tendency to focus on short-term losses rather than long-term excess performance. In other words, by helping investors manage short-term volatility and focus on long-term growth, advisors could help their clients capture puzzlingly high investment returns.

The idea that stocks are an engine that powers successful achievement of long-term goals has become dogma among financial professionals and even among academics. According to this dogma, investors with long-term spending goals should increase equity allocation to maximize expected long-run returns. I even co-authored a paper that uses a goals-based approach to estimate how much optimal equity allocation should rise when an investor’s time horizon increases.

However, much of the historical data covers time periods where, for stocks, the information was scarcer and transaction costs were much greater than the modern era. Today half of all American households invest in the stock market in mutual funds and ETFs that allow us to create well diversified stock portfolios at a very low cost. More than half of workers invest in stocks every month in 401(k)s through target-date funds. Capital gains tax rates are also historically low. The low costs and widespread automatic investment in stocks mean that markets do not need to provide a high equity premium to encourage investors to accept the risk of stock investments.

Whether the equity risk premium will persist is fundamental to planning strategy. Quantitative planning tools that estimate optimal asset allocation and saving will recommend riskier portfolios and lower optimal saving when fed stock return data from periods where stocks dominated bonds. Retirement planning software will provide analyses that assure clients that taking greater investment risk will reduce the probability of running out of money.

But a closer look at the data shows the inconsistency of the equity risk premium and suggests that the premium became far more modest as the costs of stock ownership fell.

Read the full article here by Michael Finke, Advisor Perspectives.