Holding cash feels safe

Holding cash feels safe, what you put in your piggy bank, home safe, or mattress today is safe because you can take out in the future. Most people like to feel safe and prefer to avoid risk.

Q1 hedge fund letters, conference, scoops etc

Our human tendency to dislike risk is referred to as risk aversion. The level of risk aversion differs from person to person; some people can accept a lot of risk, others almost none. The latter group would prefer to hold cash in their piggy bank at home. By keeping cash though, the money won’t grow. A Bt100-bill will stay a Bt100-bill, i.e., it will yield a 0% return.

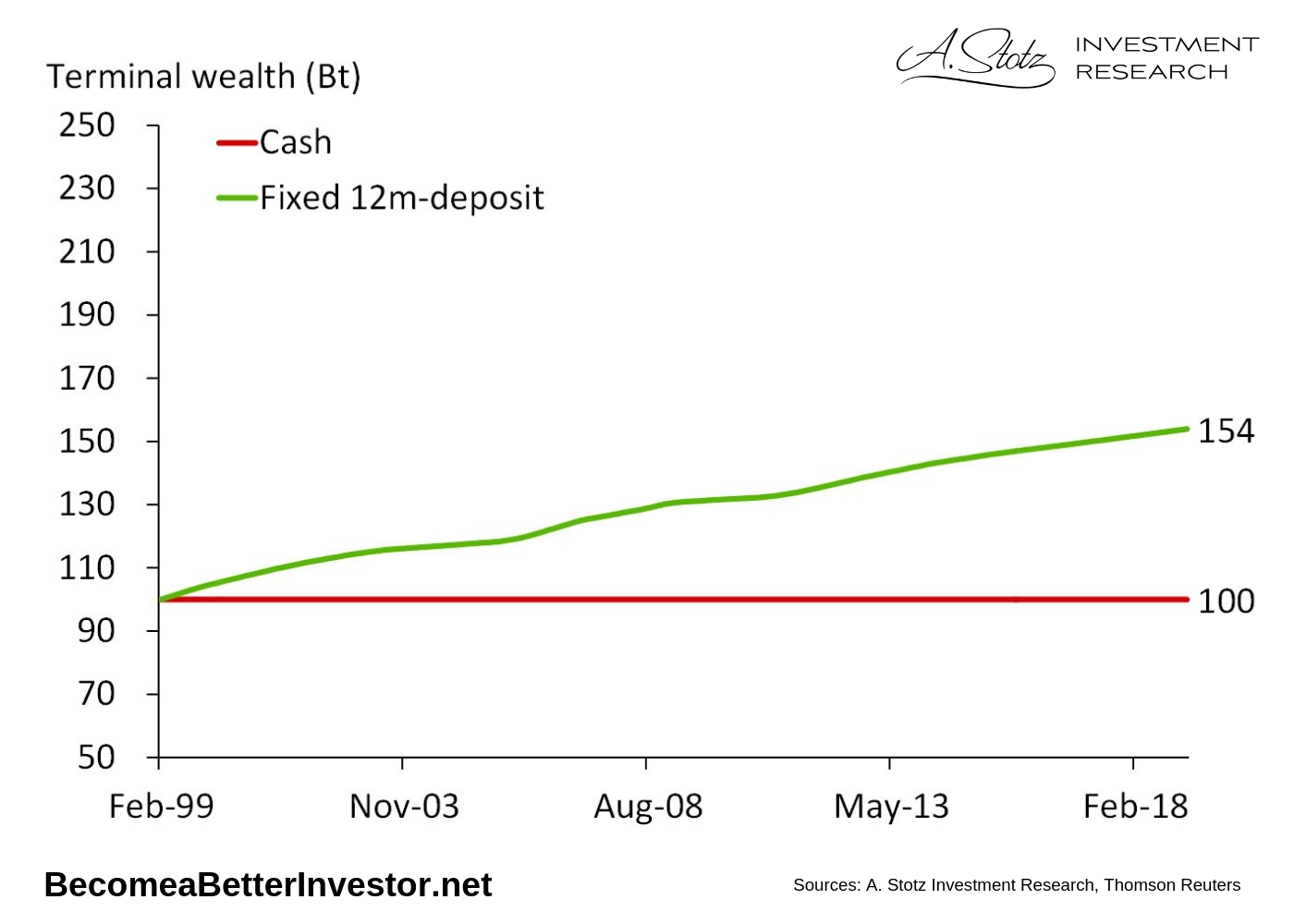

Putting it in the bank should earn you some interest

Instead of holding cash at home, you can put your money into a bank deposit. Besides safeguarding the money for you, the bank is also going to pay you some interest on the money you deposit.

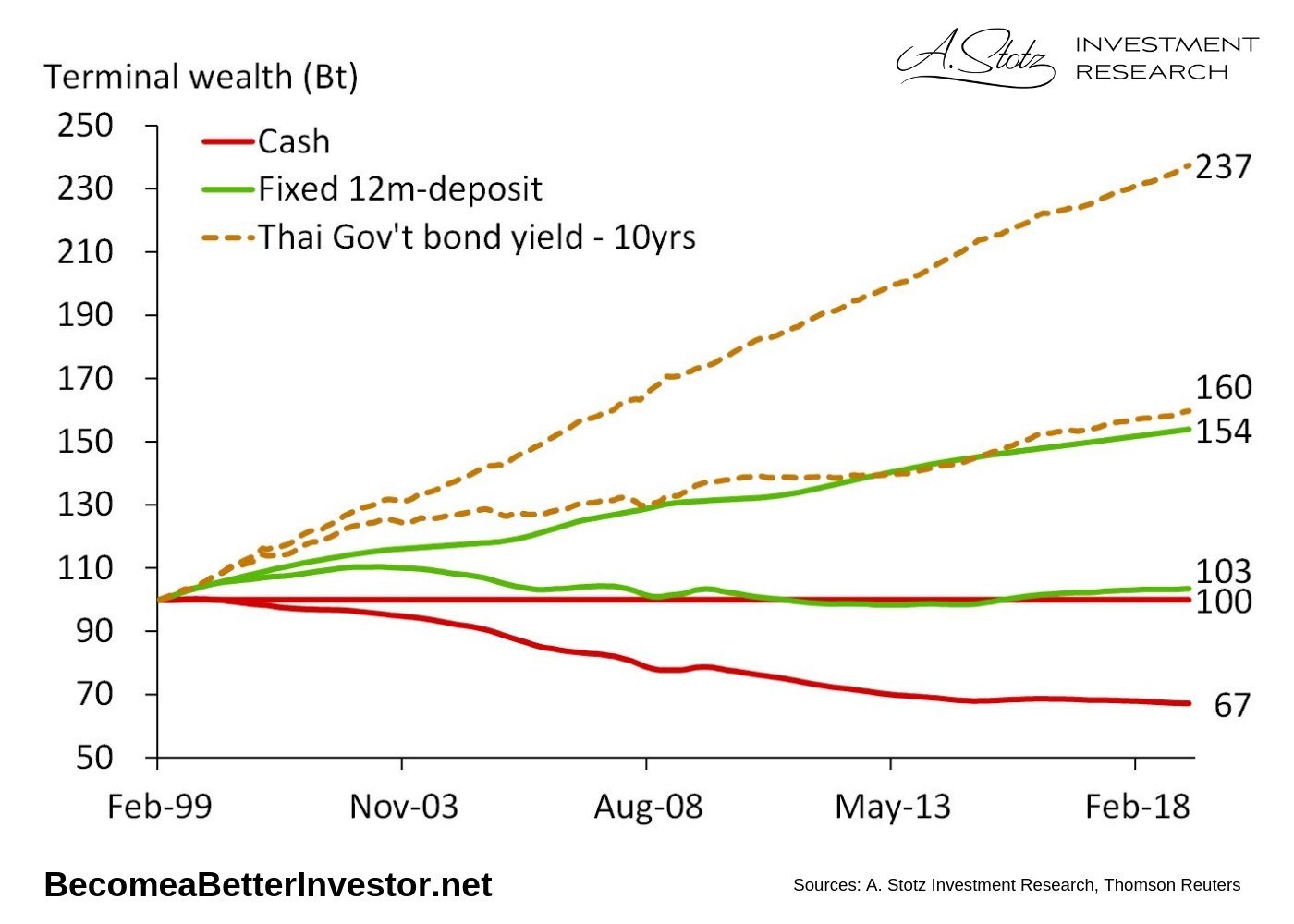

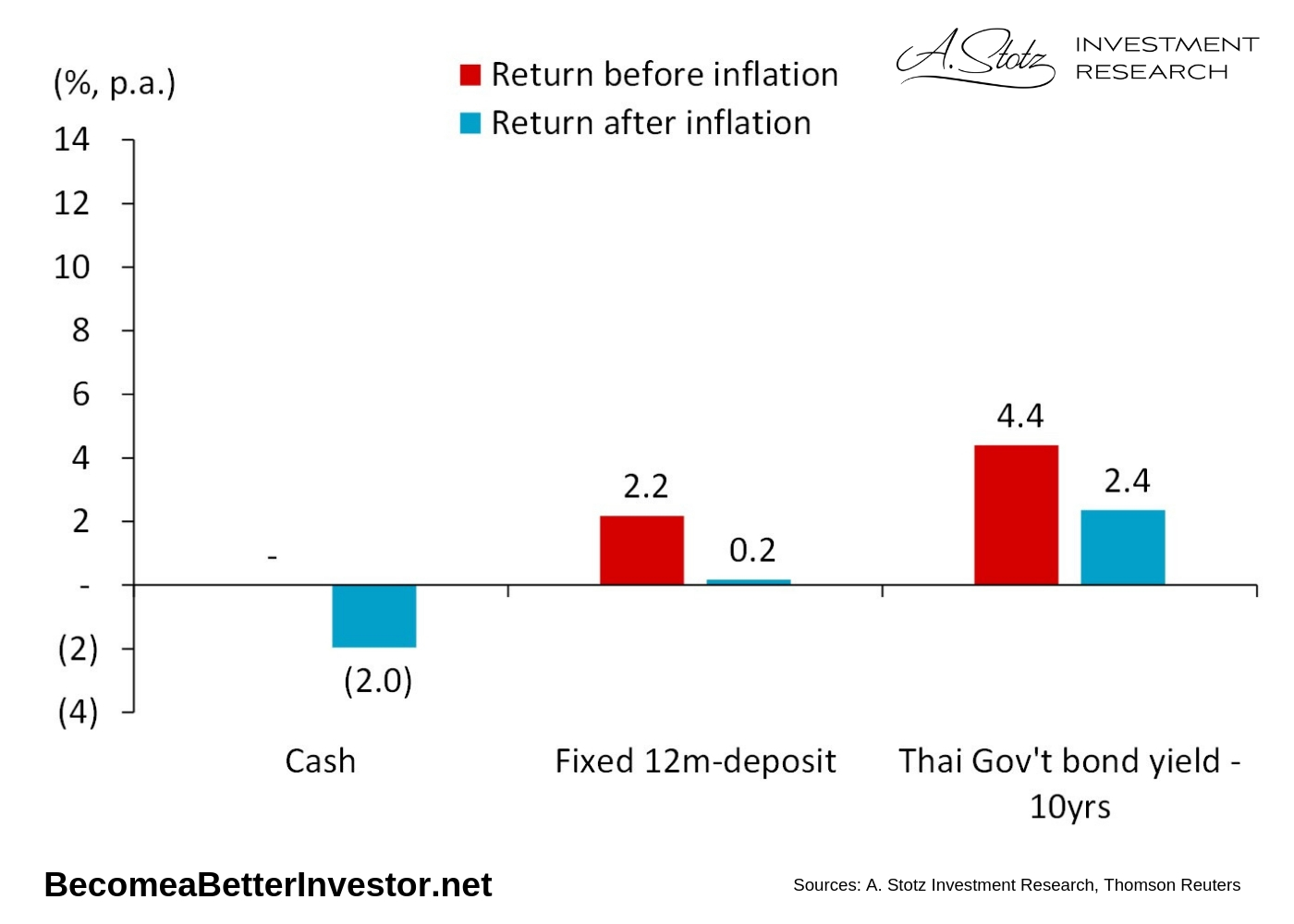

Since 1999, cash deposits in Thailand have yielded an average return of 2.2% per year. If you had put Bt100 into a cash deposit in 1999, it would have grown to become Bt154 today. Better than zero percent indeed.

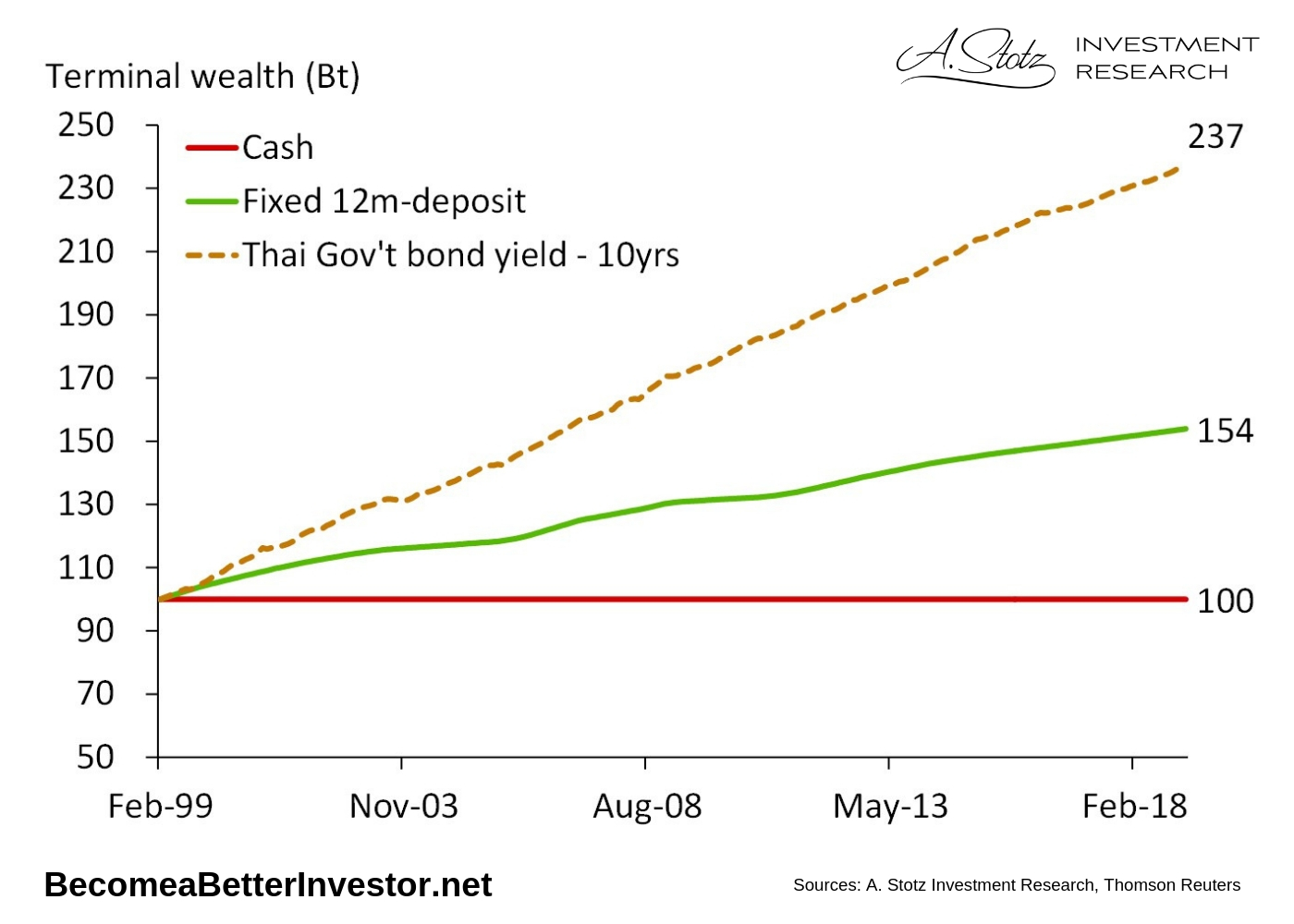

Lending your money to the government should earn you more

Lending your money to the government should be risk-free and earn you more interest compared to a cash deposit. How do you lend money to the government? When you buy government bonds, that’s what you’re doing.

In Thailand since 1999, government bonds have on average generated a return of 4.4% per annum. If you bought government bonds with your Bt100 in 1999, your money would have grown to become Bt237 today. That’s more than double compared to keeping your money in your piggy bank. Not bad, right?

But there’s one thing we haven’t talked about yet… Noodles!

How much is a bowl of noodles in Thailand today? Maybe Bt40-50. How much was a bowl of noodles 10 years ago? Maybe Bt25-30. What happened?

Inflation happened

Inflation is the reason that the same bowl of noodles today cost more than it did 10 years ago. Due to inflation, our money loses purchasing power as time passes.

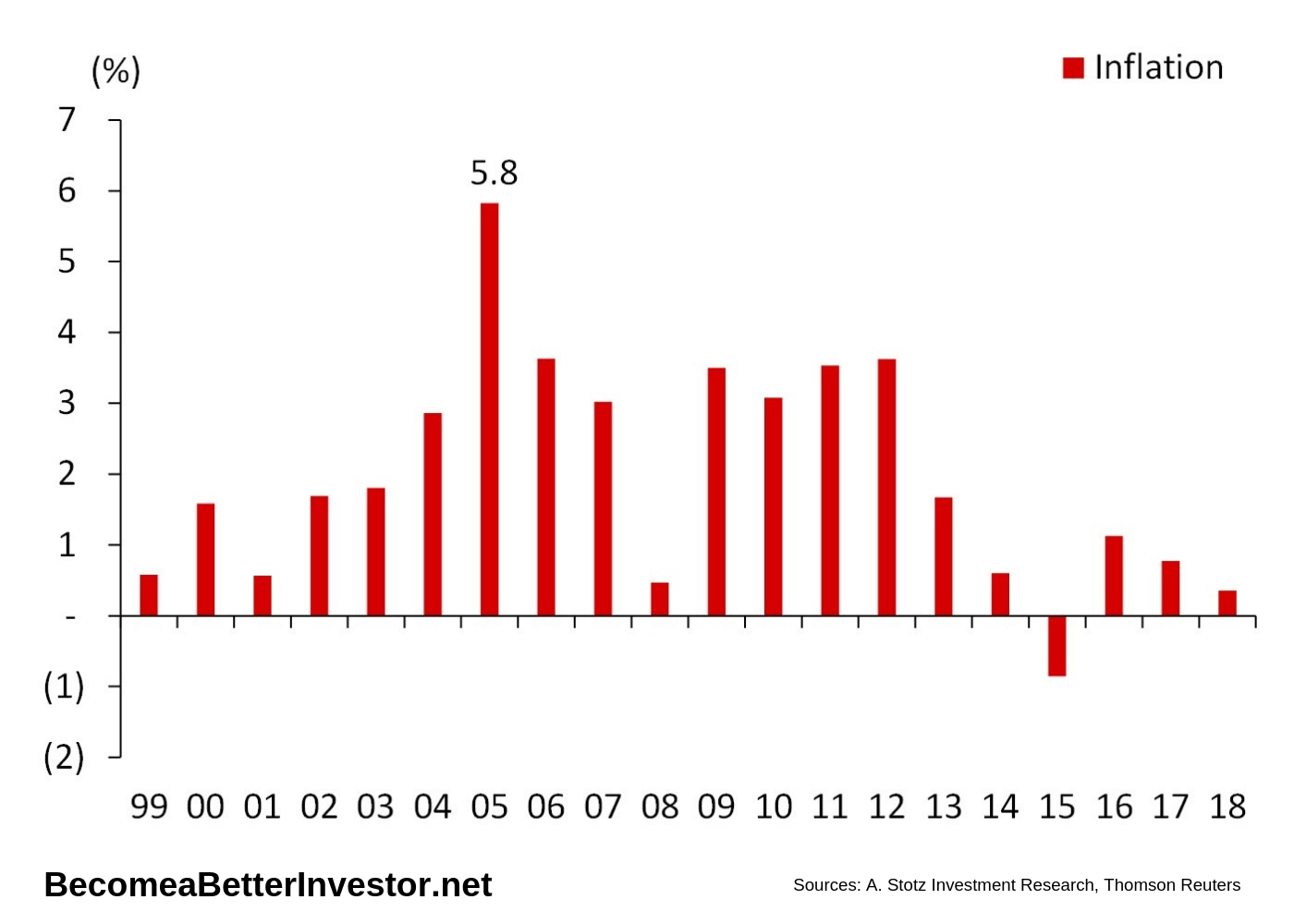

For example, in 2005, Thai inflation was 5.8%. Let’s say a bowl of noodles cost Bt20 at the end of 2004. At the end of 2005, that same bowl of noodles would cost you Bt21.

Even though the rate of inflation varies from year to year, you can see that inflation is the normal state of the economy. Only in 2015 did Thailand have negative inflation, i.e., deflation of about 1%. Meaning if you had Bt100 at the end of 2014, by the end of 2015 you could buy Bt101 worth of goods for that Bt100-bill.

Inflation reduces the real return on your investments

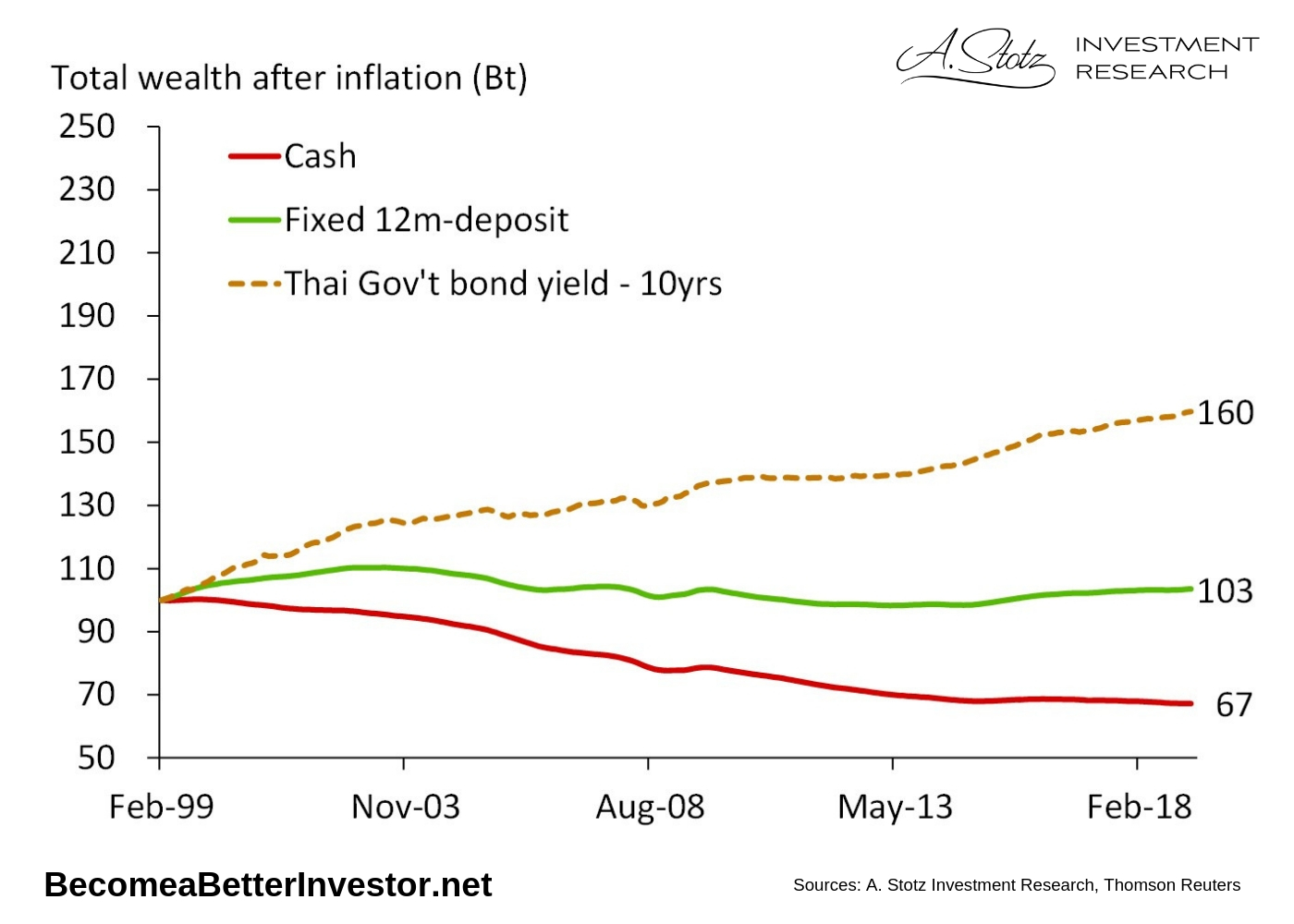

As you can see, money in the piggy bank is losing value due to inflation. Bt100 put in the piggy bank in 1999 is not worth Bt100 today, it’s only worth Bt67. Your hard-earned cash has lost one-third of its value over about 20 years.

Putting your money at the bank in a cash deposit wouldn’t have gotten your Bt100 deposited in 1999 to buy Bt154 of goods today, but rather about the same amount of goods. After inflation, you had only gotten Bt103 today.

If you lent your money to the government, it would have grown in real terms as well. If you bought Thai government bonds in 1999 for Bt100 it would not be worth Bt237 today as the average 4.4% per year return implies, but Bt160 when we consider inflation.

Inflation has reduced returns by 2%

Since 1999, inflation has on average reduced the value of your money by 2% per year in Thailand. So, the cash in your piggy bank has lost 2% every year you kept it there!

Keeping cash means you’re losing in real terms. While cash may feel safe, as the value doesn’t move up or down all the time, due to inflation, you’re losing in real terms.

Money in a bank deposit only earned on average 0.2% per year in real terms, not 2.2%. Thai government bonds yielded on average 2.4% per annum in real terms, not 4.4%.

The 4.4% per year return of government bonds first appears quite attractive. It more than doubles your money over 20 years. But when you consider inflation it doesn’t double your wealth.

If your savings only grow by 2% per year for the next 30 or 40 years will you have enough money to live in comfort when you get old?

By avoiding taking on any risk, you can’t expect to earn very much in return. You expose yourself to so-called shortfall risk which is something discussed in the next post.

Article by Become A Better Investor