- Shares of Limbach appear extremely cheap based on 2018 EBITDA guidance, which includes unanticipated expenses (aka one-time) that are unlikely to recur in

- Assuming nothing worsens when the company reports 3Q results in November, we expect a significant relief rally. Recent management commentary appeared bullish regarding

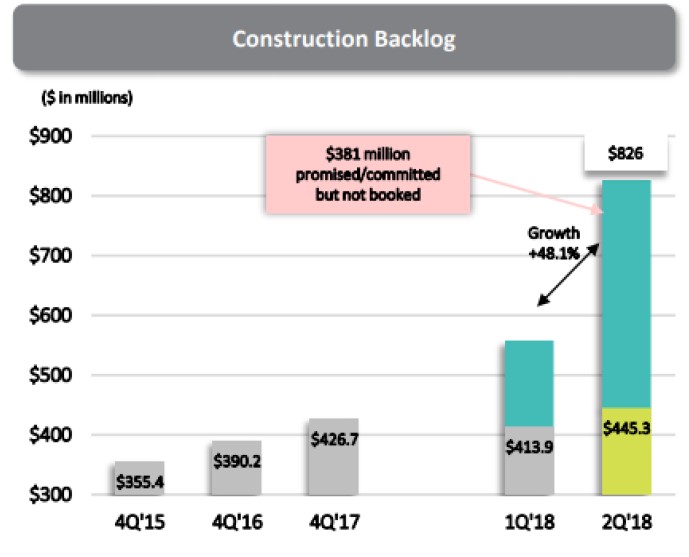

- Adding back non-recurring costs, substantial backlog growth coupled with higher pricing on that backlog, and a recently announced accretive acquisition, EBITDA should expand dramatically in 2019, even with conservative

- We believe that 2019 EBITDA that could approach $37-$41mn$18-20mn in 2018. Additional acquisitions or reimbursement from claims settlements could add further EBITDA upside.

- At a 1-2 EBITDA turns discount to 2019 peer multiples, Limbach shares would triple. Heads, I win (a lot); tails, I don't lose much!

Dane Capital – Limbach: Potential 3-Bagger, A Surprisingly Feasible Scenario

Jacob Wolinsky

This article first appeared on HiddenValueStocks

Jacob Wolinsky is the founder of HedgeFundAlpha (formerly ValueWalk Premium), a popular value investing and hedge fund focused intelligence service. Prior to founding the company, Jacob worked as an equity analyst focused on small caps. Jacob lives with his wife and five kids in Passaic NJ. - Email: jacob(at)hedgefundalpha.com FD: I do not purchase any equities to avoid conflict of interest and any insider information. I only purchase broad-based ETFs and mutual funds.