Crosspoint Capital Management commentary for the second quarter ended June 30, 2018.

Q2 hedge fund letters, conference, scoops etc

Markets Overview

After pulling back in the first quarter US equities finished higher at the close of the second quarter. Trade remained the big story and the main driver of market volatility; still, pockets of strength surfaced within small to mid-caps, energy, consumer discretionary, and technology sectors. Even though trade tensions created a noticeable headwind throughout the quarter, the notion of a full-fledge trade war seemed to be overblown as the positive US economic data, coupled with strong earnings growth, outweighed the trade fears. According to FactSet, “S&P 500 EPS increased ~25% in Q1, better than the 17.1% expected in late March and the strongest growth since it began tracking the metric in Q3 2008.” However concerns of peak growth muted performance. In the end, the market was able to climb the wall of worry.

Market Sentiment Indicator (MSI)

For those who are not aware, our Market Sentiment Indicator (MSI) is our weekly proprietary breadth indicator of the market. Our MSI tracks roughly 3500 stocks, giving us a broad perspective of the market’s current health. The MSI breaks down the market into three readings: Positive, Neutral, or Negative depending upon the short term trends of the equity market. This foundation guides our equity exposure amongst our strategies to the market.

Throughout the first half of 2018 our MSI was reactive to market volatility, especially within the tail months of Q1 and the early days of Q2. On the quarter, we witnessed two Negative, two Neutral, and one Positive readings. The chart below reflects our weekly MSI readings over the past year.

As indicated above, the early weeks of Q2 displayed volatility however this ceased on May 18th, when our MSI shifted into a Positive stance, where it remained throughout the remaining portion of the quarter; ultimately aligning our strategies, Crosspoint Tactical All-Cap and Crosspoint Accelerated Growth, with the recent uptrend and thus facilitating the outperformance of those said strategies over the quarter.

Crosspoint Tactical All-Cap

Our longest running strategy, dating back to January 1, 2005, the Crosspoint Tactical All-Cap (CTAC) couples elements of technical and fundamental analysis to compose a diversified equity portfolio of thirty market leading stocks. The investment approach of CTAC is truly an active approach to investing, active managers over the past few years have shown difficulties in outperforming the S&P 500. The difficulty is largely attributed to the narrowness of the past quarters rallies, a few names have controlled performance within the S&P while the rest of the market either suffers or sputters along. However over the past few months the strength of the Russell 2000, an index comprised of 2000 small cap stocks, displayed broad market participation. This indication of broader market participation, creates a stock picker environment. In the end, a healthier market should result, where portfolios do not solely hold Apple, Amazon, or Netflix.

For the quarter the Crosspoint Tactical All-Cap returned +6.3% gross of fees vs. the S&P 500 return of +3.4% total return.

As we re-entered the market on May 18th, via our MSI, we did purchase Netflix and Amazon for our portfolio, but obviously they were not our sole holdings. The makeup of our diversified portfolio of thirty stocks were more weighted towards SMID Caps ($2b-$4b market cap companies), comprising a 30% weighting within the portfolio. Our top sector weightings within the portfolio were Consumer Discretionary, Healthcare, followed by Tech. A high number of our top gainers were found within this fabric, driving our outperformance on the quarter. However, as such with the market, we witnessed strength throughout the portfolio. Indicative of our low turnover within the portfolio, two sales occurred – one on a fundamental shift and the other on a stop loss trigger.

Even though we are constantly looking for new market leaders, we move into the third quarter with positive momentum within our portfolio. However headwinds could present themselves, headwinds around corporate earnings and the trade debate, but we will remain diligent to our process.

Crosspoint Accelerated Growth

We are extremely excited to introduce Crosspoint Accelerated Growth (CAG), the strategy became open to investors early in 2018, but performance dates to May 2017. Even though the strategy is infant, it has been receiving increasingly high interest. Outside of positive returns, excitement, lays within a belief that we have been able to blend “Active vs. Passive” investment approaches. Whereas our CTAC takes purely an active approach CAG however uses the same foundation as CTAC, relative to our MSI, yet employs a “passive” approach, that overlays an “active” rules based approach to create a hybrid investment solution. Granted, like all investments, suitability needs to be defined for each client, but we believe it merits an allocation within an overall portfolio construction due to the metrics it has thus displayed.

For the quarter the Crosspoint Accelerated Growth returned +8.7% gross of fees vs. the S&P 500 return of +3.4% total return In a difficult tape for market trending strategies, CAG was able to generate alpha through its rotational features. These features seek beta exposure by shifting amongst ETFs to hopefully maximize gain and limit downside exposure. Through preset rules, outside of a brief period, CAG was fully allocated throughout the quarter. Even though the beta exposure ebbed and flowed, the constant market exposure was paramount, driving the outperformance. Note that capital preservation is not taken for granted, hence that brief period where the strategy held a 100% cash allocation.

As we exit Q2, CAG remains allocated to the market. We believe, through our MSI data, the market is posed to continue its most recent uptrend if so CAG will generate increased alpha.

Looking Forward

“Chaos in the world brings uneasiness, but it also allows the opportunity for creativity and growth.” ~ Tom Barret Timely and true words on many levels especially within the current environment.

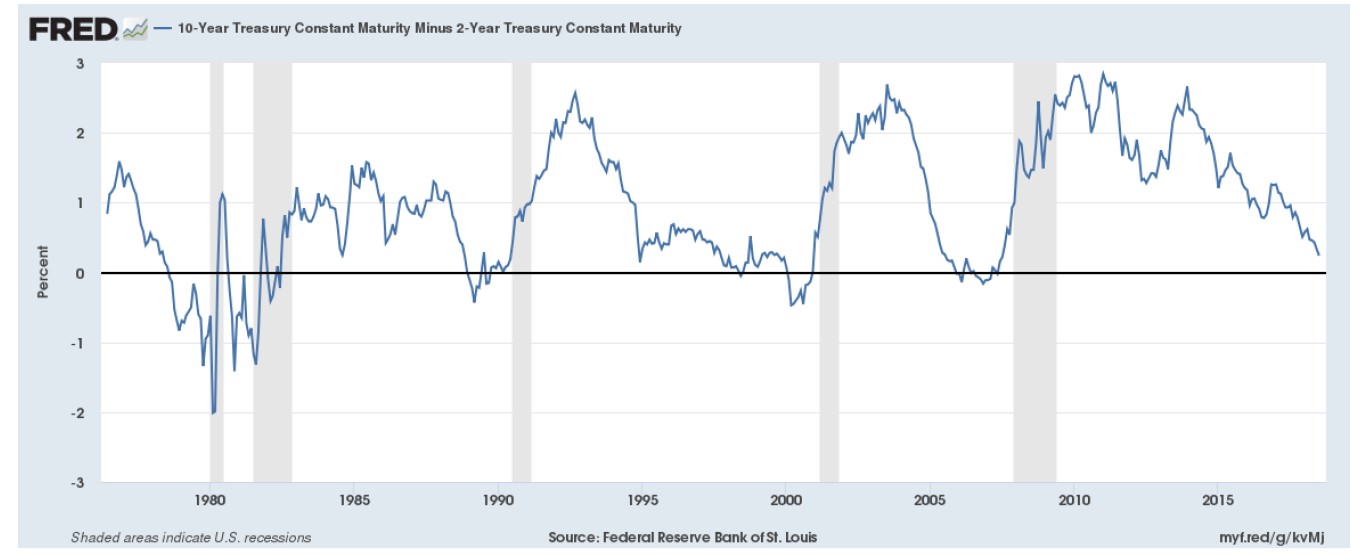

The second quarter “Market Overview” could be essentially inserted into the “Looking Forward” segment. Many of the events and issues remain as we move into Q3. Expect one, the yield curve – the spread between the 2yr and 10yr T-bill, to gain increasing amounts of headline exposure. Historically the compression in the spread has led to recession, as indicated in the chart below.

As we laid out prior, we feel many factors are currently playing into this occurrence – trade war rhetoric, earnings peak, etc. In our opinion, this is all noise. For example, the trade war benefits no one, we all know this, and the rhetoric is pure negotiation. A strengthening US economy is being leveraged, which should result in compromise. If not, the Fed will become dovish if the environment becomes dicey. In the end, we feel many are not looking at the big picture, the world needs inflation, which will steepen the curve and place lipstick on the growing deficit. So we believe the market should continue to climb the wall of worry.

Over the past couple years, Crosspoint Capital Management, on a firm level, has experienced change, positive change. Changes that has refined our vision establishing new goals while aligning us on a deeper level with clients and prospective clients. We are thankful for these developments. Within this correspondence, we indirectly touched upon one, the introduction of our new strategy Crosspoint Accelerated Growth, which we anticipate will be one of many to come. This being one of many goals, increasing our investment offerings to help clients achieve their respective goal. We look forward to growing with our client’s.

Sincerely,

Tony Cantando | CEO

Crosspoint Capital Management