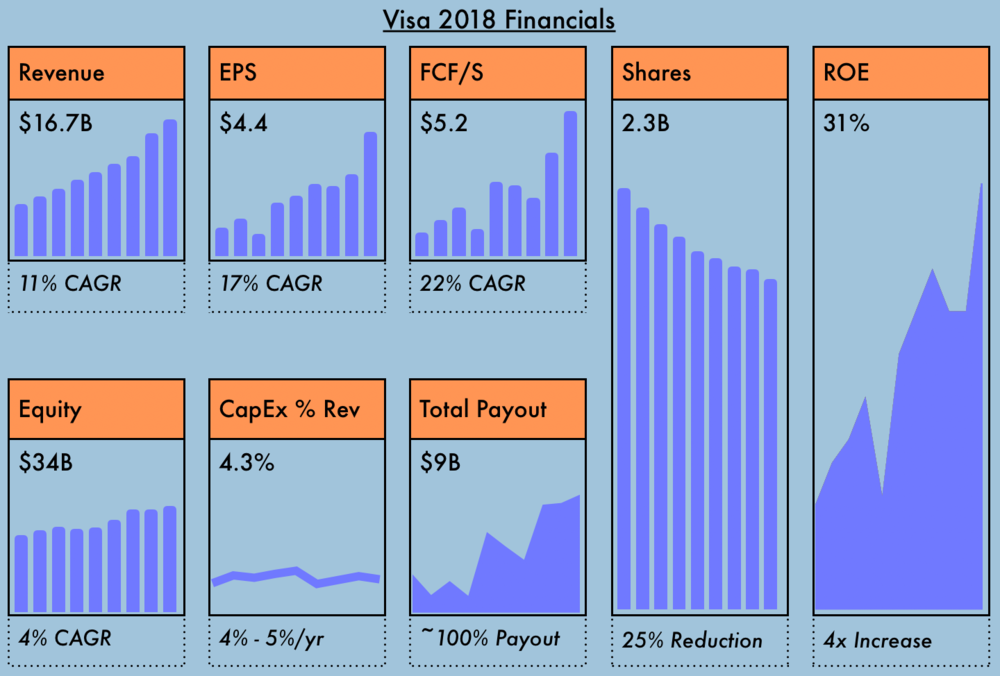

Visa is a financial giant that focuses on providing global payment technology. It works as a bridge between consumers, businesses, and governments. It ensures safe payment processing in over 200 countries and territories. Visa and its importance in the financial industry is a multilayered topic that requires a dive into payment processing and its aspects.

The first and the major input of Visa is that it allows billions of people to make and receive payments. It offers a payment solution for people who do not have access to traditional banking services. It works as an innovator with the implementation of improved technologies.

But since it doesn’t issue credit cards it is a frequent question of how it makes money. Data processing charges bring almost half of its income. Other revenues include international transaction revenues, licensing, and service revenues. Stay with us to understand the Visa, its operating model, and how Visa makes money.

Business Model of Visa: How Visa Makes Money

The beauty of Visa’s business model is that they get paid every time one of their cards are used—a flat fee of $.07, plus 0.11% of the transaction amount (and more for international transactions). So the more dollars that flow through Visa’s network, and the more transactions that they process, the more money they make.

Since Visa does not deal with credit card issuing, it has other sources of income. Its formula for success revolves around a three-sided marketplace model. The model connects cardholders, merchant partners, and financial institutions. Key elements of this model are:

-

Transaction Fees

Visa implements two types of transaction fees - interchange fees, and cross-border transaction fees. Transaction fees are paid by the merchant’s bank to the card-issuing bank for every Visa transaction. In this transaction, Visa is a facilitator and earns a small percentage of the fee.

In cross-border transactions, charges are higher due to the use of different currencies. Visa’s network provides seamless money transactions almost anywhere, and for it, it charges a fee.

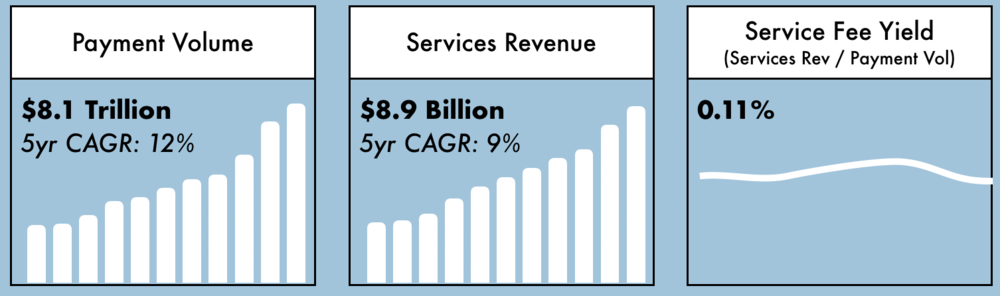

To participate in the Visa network (i.e., accept/issue Visa cards), banks pay Visa a small percentage of the total dollar amount of every transaction. So the more a product costs, the more money Visa makes. That makes payment volume—which is the total dollar amount spent on Visa’s network—the primary driver of this revenue source. What’s great about this type of revenue is that it’s a built-in hedge against inflation; if the cost of goods rises, Visa’s revenue automatically rises with it.

In 2018, Visa’s services revenue was $8.9 billion on $8.1 trillion of network spend. That means Visa pockets about 0.11% of every transaction, which is known as the service fee yield.

-

Value-added Services

Visa offers a Visa direct platform for advanced users. Through it, users can execute fast and secure real-time money transfers between banks and accounts. Visa earns from this platform through charging processing services.

As a part of their advanced service package Visa offers sophisticated fraud detection and prevention services for their digital payments. Through these support services, Visa makes additional capital from merchants and card issuers.

Also, Visa's business model includes using vast transaction data. With it, Visa can provide advisory services and valuable insights to clients for fees.

-

Network Expansion and Innovation

By expanding the business network, Visa is widening its reach, bringing new clients to Visa’s network of services. With each new client, Visa is increasing payment volume.

With the implementation of new technologies like contactless payments, virtual cards, and digital wallets, Visa is expanding its services. These digital solutions are guaranteeing steady income in the future.

Revenue Streams

Visa generates income through various streams connected to their services as a facilitator of electronic payments and transactions.

The main revenue streams are transaction and service fees that we already mentioned. Another major revenue for Visa is licensing rights. Visa is charging license fees to financial institutions, payment processors, and other entities.

Also, using ATMs also brings a safe and regular income to Visa. Visa charges every money transaction from the ATM with the use of Visa-branded cards.

Using digital technologies like mobile payments and digital wallets also brings solid chunks of profit to Visa. All partners and tech companies that are using Visa digital network for their services pay a fee.

Transaction Processing Fees

When talking about these fees, we already talked about types of fees. However, some factors can influence transaction processing fees.

Different card types come with different transaction fees. Premium cards like Visa Platinum or reward cards have higher interchange fees when compared to classic Visa cards.

The type of transaction also impacts what revenue Visa will receive. In-person purchases have lower fees than online or phone purchases.

There are different types of merchants, and every type has its transaction processing fees. Merchants are categorized under MCC categories, which can have variable processing fees.

Unrelated to cross-border transactions are regional differences and their impact on fees.

Geographical location often dictates the fees, and they can significantly vary. That means if you used your bank ATM to withdraw money in your country, it will probably be pricier to do it in another country.

Interchange Fees

Interchange fees represent a percentage of a transaction amount. It is paid by the merchant’s bank to the bank that is the card issuer. This fee is charged with every transaction that occurs, and Visa makes a small percentage.

The purpose of interchange fees is often disputed and controversial. Visa’s stance is that these fees are necessary. That Visa covers costs associated with car insurance, fraud prevention, client incentives, and reward programs.

Card issuers are incentivized to offer different cards and options when these fees are higher. This way the issuers are earning more, and through programs are offering clients benefits for utilizing cards.

Maintaining a complex infrastructure network also demands money. Some of the assets gathered through these fees are invested in the maintenance and development of payment services.

The negative aspects of these fees are higher prices. Merchants often add these fees to prices, so they do not lose on their profit margin. This overall lowers the quality of life.

Another issue is limited competition. High interchange fees discourage new companies from entering this arena. New players could develop advanced technologies and lower costs. This mainly inflicts the users who do not have the chance to benefit from a diverse payment services market.

Licensing and Processing Fees

Visa is charging licensing fees for its brand and technology to financial institutions and banks. Licensing fees between the Visa and the client differ based on the negotiations between the two sides.

- Visa brand licensing

All banks and financial institutions that issue cards with the Visa brand pay a licensing fee. The Visa is widely recognized and trusted and its brand resonates with confidence among its users.

- Visa technology licensing

Using Visa cards is only a part of the provided service. The users also have to acquire the right to use Visa’s global payment network and transaction processing systems. This includes all infrastructure needed for secure and efficient electronic payments.

- Negotiations

The licensing agreement between the user and the Visa comes as a result of negotiations. All the terms, including the fees are specified as a part of the agreement. The factors that can impact the agreement are the size and power of the institution and the sheer number of presumed transactions.

Cross-Border Fees

These fees are charged when making transactions with a Visa card in a currency that is different from the card’s currency. There are three basic types of these fees, and they impact both the merchant and the cardholder.

- Foreign transaction fee. This fee is charged by the card issuer when the user uses their visa card in foreign currency. The fee depends on the transaction amount. Visa earns a small percentage depending on the card issuer and the merchant

- Currency conversion fees. These fees are used to cover the cost of converting the transaction currency to credit card currency. This fee is usually flat and in the range between 1% and 2%

- International service fee. This is a part of the cross-border transaction processing fee. It is also a flat fee that falls in the range between 0.2% and 1.2%.

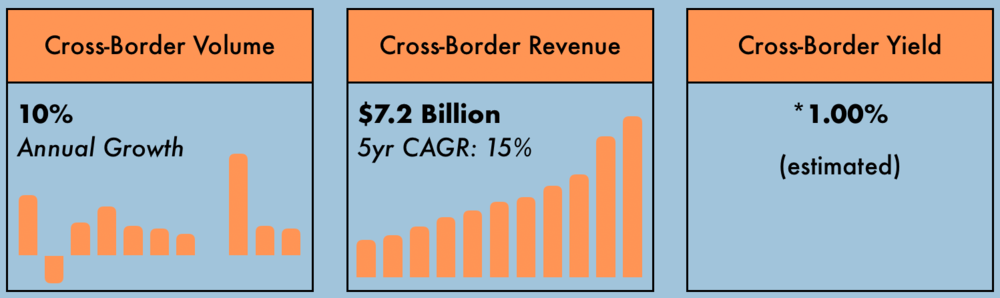

Visa earns additional revenue for processing cross-border transactions; that is when the merchant’s bank and cardholder’s bank are in different countries. Because these types of transactions are more complex, require currency conversion, and tend to have a higher rate of fraud, the fees are much higher than those on domestic transactions. The primary driver of this revenue source is the total cross-border dollar amount; however, Visa does not break this number out.

In 2018, Visa’s cross-border revenue was $7.2 billion. The yield is estimated to be around 1%, making it Visa’s highest-yielding and most profitable product—by far.

Other Revenue Sources

Besides fees and licensing which are the biggest income generators, there are also other sources of revenue. They amass around 7% of total Visa income and are crucial for Visa’s overall financial stability and expansion. These sources include:

- Intellectual property licensing. Visa makes money from licensing their intellectual property. This includes their payment processing platforms, security protocols, or data analytics tools

- Network access fees. Some major financial institutions and payment services need specialized access to specific parts of the Visa network. This falls into a tailored service that Visa charges

- Product enhancement charges. When introducing new or improved services, Visa may charge fees to existing users

- Account holder services. Depending on the region Visa offers services directly to cardholders. Those services can include ATM network access or travel insurance plans. If the users want to utilize these services they need to pay either a subscription or a transaction fee

- Consulting and training. Professionals from Visa provide expertise and training to financial institutions and merchants. Those include training for the use of their basic services, to advanced education to government entities and major corporations

- Interest income. Visa is not known as a major investor. But, some portion of their income comes from both short and long-term investments

- Other fees. Some fees cannot be categorized into any of the groups above. Those include income from penalties, late fees, or revenue from strategic partnerships.

Market Share and Competition

Visa is a giant in the global payment industry where it holds a global market share of 52.22%. Its primary competitor is MasterCard which holds 24.13%.

Besides MasterCard, there are other major regional players like UnionPay in China and RuPay in India. These are not a threat on a global scale but are worthy competitors on a regional scale.

The rise of fintech introduced a new breed of companies. These new players can prove to be fierce competition with the introduction of new technologies and approaches. The notable fintech competition includes PayPal, Stripe, and Square.

Challenges and Future Outlook

Evolving regulations are one of the crucial factors that harm Visa’s operations. Those regulations are aimed at data privacy and interchange fees and can have a major impact on Visa’s operations and income.

The introduction of new players with innovative business models is a big challenge. They are offering new commercial payment solutions that are tough to beat. This combined with the traditionally biggest competitor MasterCard, is a tough market game for Visa.

The key to overcoming these issues is choosing the right strategic partners and implementing beneficial new technologies.

Challenges for all traditional payment services are the development of blockchain and cryptocurrencies. These digital payment methods can disrupt the market. If Visa wants to prosper, it needs to adapt to new market conditions and work on applying new technologies.

FAQs

How Does Visa Make Money from Credit Card

Visa's business model focuses on offering services and infrastructure for their credit card products. They bring revenue in several ways:

- By collecting fees, and service revenue from issuers of credit cards

- By charging data processing fees and transaction interests from consumer payments.

Basically, Visa makes money by being the middleman in the transactions. They provide the technology, the infrastructure, and the processing services. Visa’s goal is to make a system that works seamlessly.

Does Visa Make Money on Every Transaction?

No, Visa makes money only on transactions made by their cards. Money movement through other payment networks doesn’t generate money for Visa. Cash-only transactions also do not include any fees connected with Visa. Specific peer-to-peer transfers do not depend on Visa services so they are not charged.

How Much Does Visa Make From a Transaction?

The earnings from individual transactions depend on several factors. Fees are variable depending on the type of transaction. Interchange fees are usually lower when compared to cross-border transaction fees.

How financial institutions negotiate cooperation with Visa will also have an impact on the transaction fee. Once agreed these fees are flat, and they vary between financial institutions. Depending on the case, interchange fees in Europe are in the range of 0.3% and 0.4% while in the United States, they rise to 2%.

Who is Visa's Biggest Competitor?

Visa's biggest competitor is MasterCard. Annually these companies combined process hundreds of billions of transactions. Visa is still the biggest player, but the gap is closing.

Final Thoughts

Visa’s business model focuses on providing payment services to financial institutions and merchants. Their revenue comes from transactions made by using Visa-licensed products like credit and debit cards, providing network services, and from their advanced services including fraud prevention.

For a long time, their only major competitor has been MasterCard. But, with the development of new payment methods, new service providers are storming the market. Since Visa was always a trendsetter their innovative approach and new products are allowing them to still be the undisputed number one in the financial transaction market.

You can model those assumptions here:

This article was originally published on MineSafetyDisclosures.com.

Article by Vintage Value Investing