Can Value Investors Capture Factor Returns via Smart Beta?

Q3 hedge fund letters, conference, scoops etc

SUMMARY

- Smart beta Value ETFs are relatively homogenous

- Some show high exposures to other equity factors, which may represent risk

- Excess returns from smart beta are significantly lower than long-short factor returns

INTRODUCTION

The last ten years can be viewed as a lost decade for Value investors as excess returns were almost consistently negative. Although ETF investors have allocated more capital to the Growth factor as of the end of 2018, the top five smart beta ETFs by assets under management still contain two products focused on Value (VTV & IWD).

ETF issuers have launched Value-focused products for various sectors and indices, offering investors choice but also increasing the complexity in asset allocation. In this short research note, we will analyze the spectrum of smart beta Value ETFs available in the U.S. and reconcile smart beta to factor investing returns.

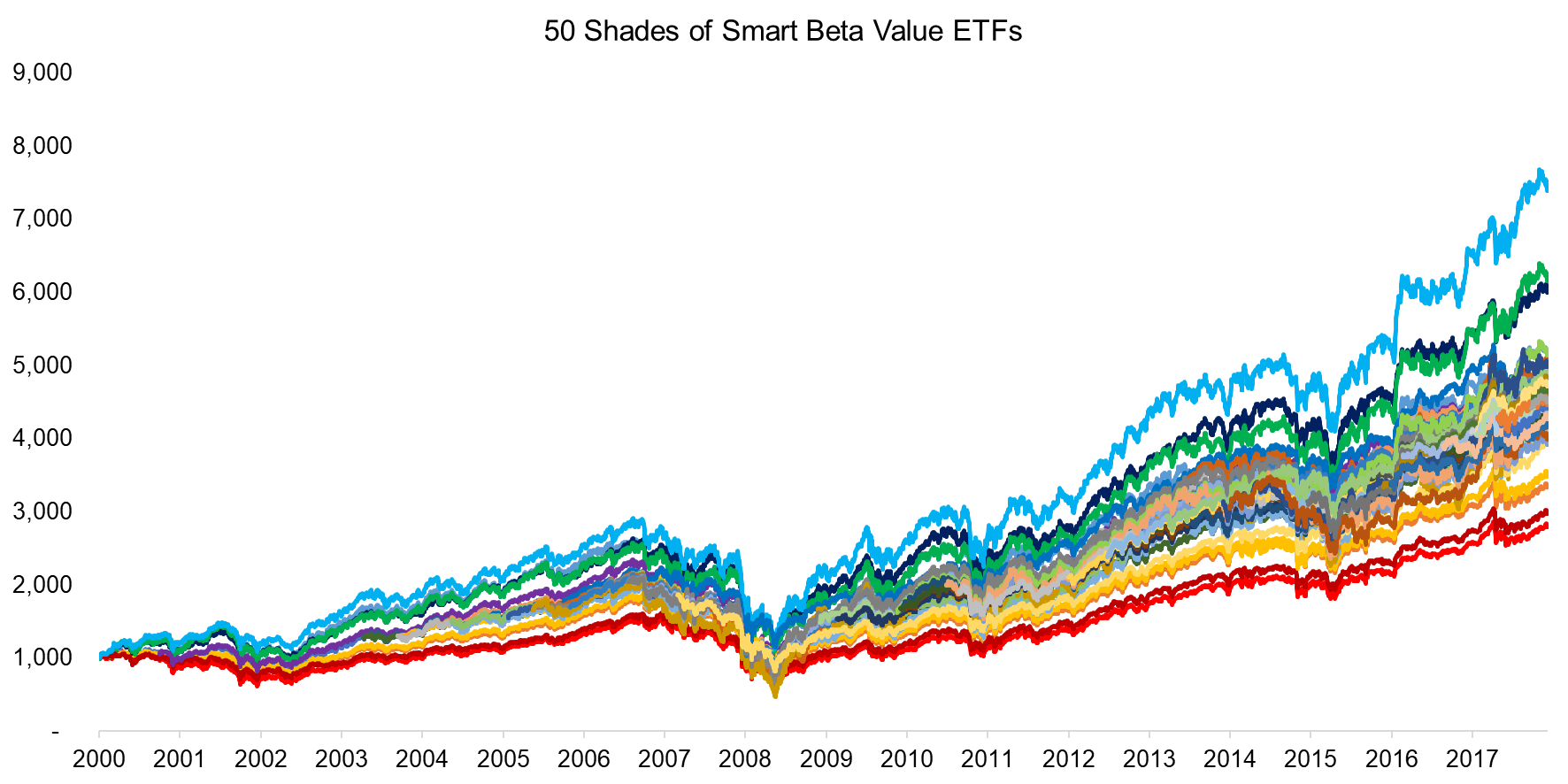

50 SHADES OF SMART BETA VALUE ETFS

We focus on smart beta ETFs traded in the U.S. stock market that provide exposure to the Value factor. A few of these were launched in 2000, providing investors will almost two decades of data for performance analysis. Some of the ETFs are sector-focused, which explains the outliers in chart below. However, the majority of smart beta Value ETFs generate relatively homogenous returns.

Source: FactorResearch

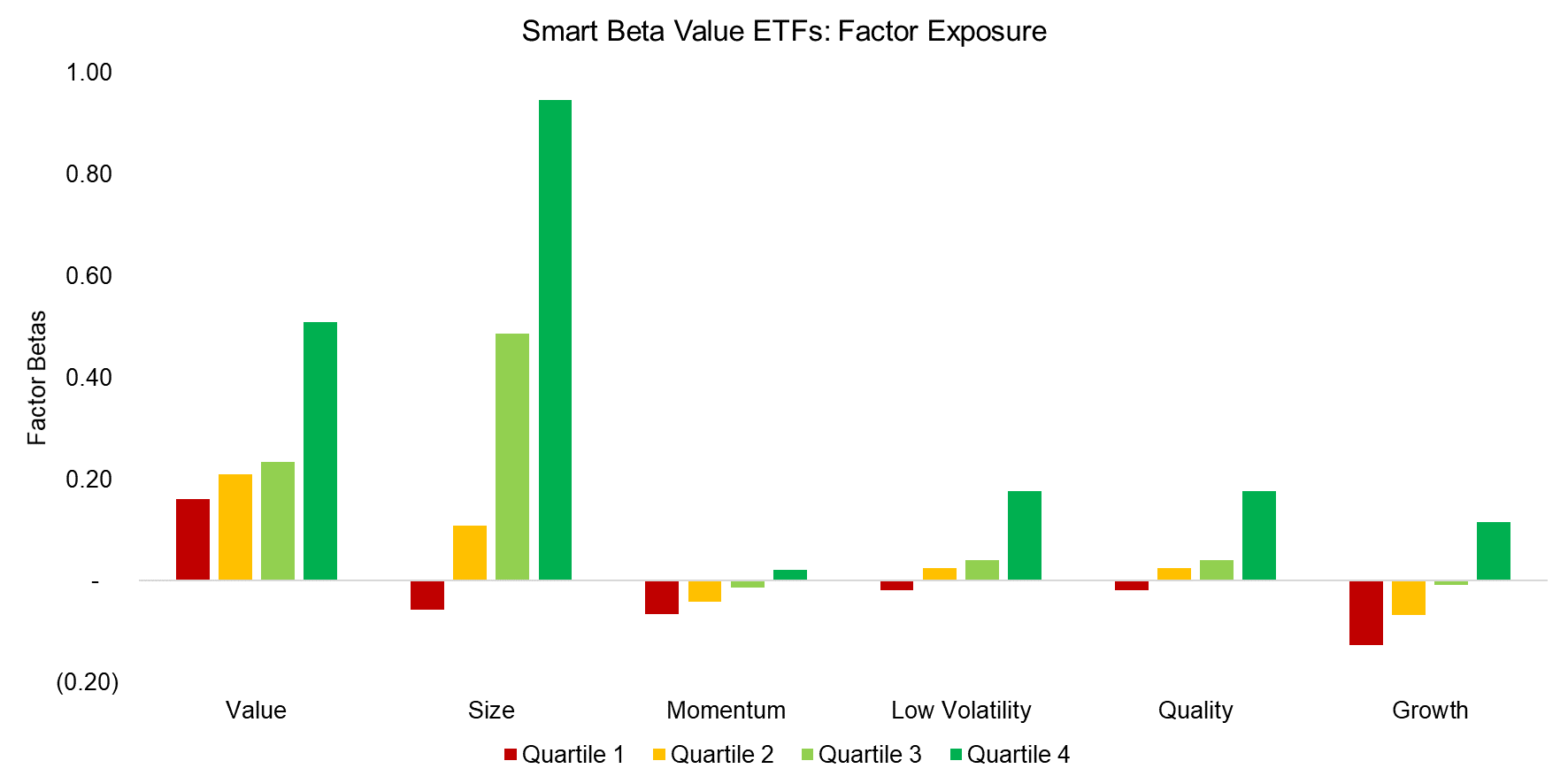

FACTOR EXPOSURE OF SMART BETA VALUE ETFS

Given that smart beta Value ETFs focus on the Value factor, investors might expect all of these to show high exposure to the Value factor. However, the Value factor can be defined in many ways, which results in some ETFs showing relatively low exposure to our Value factor definition, which is a combination of price-to-book and price-to-earnings multiples. The factor exposure represents factor betas derived from a regression analysis with a one-year lookback. The universe of smart beta ETFs is split into quartiles to highlight the diversity of products.

We also observe that most smart beta Value ETFs show high exposure to the Size factor, which is explained by many products focusing on Value in small cap indices like the Russell 2000. The exposure to other factors is low on average, but some ETF feature strong exposure to Low Volatility, Quality, and Growth, which may represent undesired risks for investors.

Source: FactorResearch

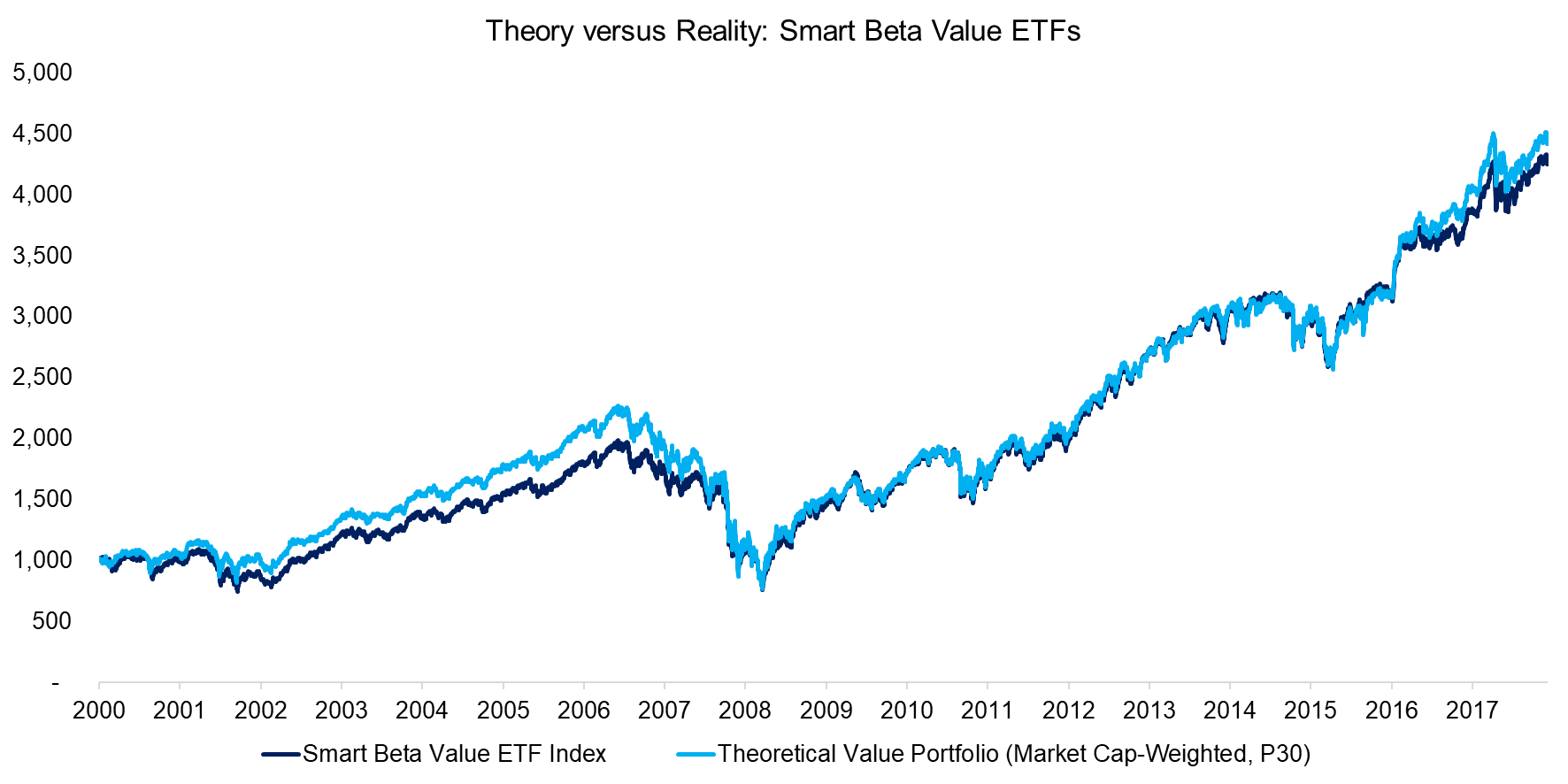

THEORY VERSUS REALITY

Next, we create an index for smart beta Value ETFs by equally weighting all ETFs in our universe. We also construct a theoretical long-only benchmark by selecting the cheapest 30% of all stocks in the U.S. with a market capitalization larger than $1 billion ranked by a combination of price-to-book and price-to-earnings multiples. The analysis highlights that the Smart Beta Value ETF Index tracks the theoretical Value portfolio relatively close, which is likely explained by most product providers using similar factor definitions.

Source: FactorResearch

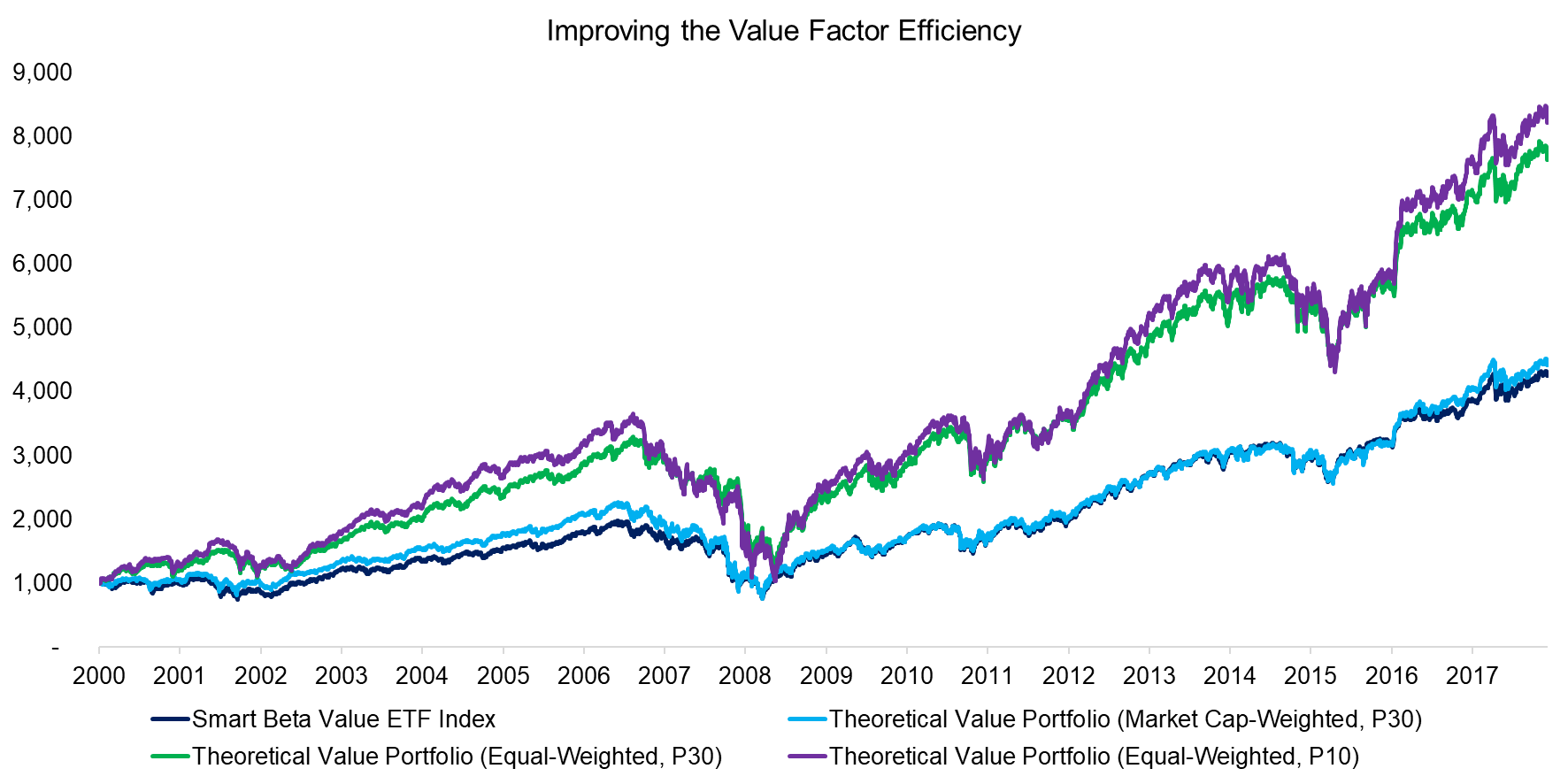

IMPROVING THE VALUE FACTOR EFFICIENCY

Investors allocating to smart beta ETFs likely base their investment decisions on academic research on factor investing. There are some key differences between investible products and theoretical portfolios, which includes the weighting methodology. Smart beta ETFs typically weight by market capitalization while researchers tend to allocate equally to stocks. Investors need to be aware that a market capitalization-weighting is equivalent to shorting the Size factor. If the Size factor generates positive performance, as it did between 2000 and 2018, then this may penalize smart beta ETFs that weight stocks by market capitalization.

The analysis below highlights that since 2000 a Value portfolio that equally allocates to stocks would have significantly outperformed the Smart Beta Value ETF Index, whose ETFs mostly weight by market capitalization. We also show results for a more concentrated Value portfolio that selects the cheapest 10% of stocks (P10), but that does not improve performance much further.

Source: FactorResearch

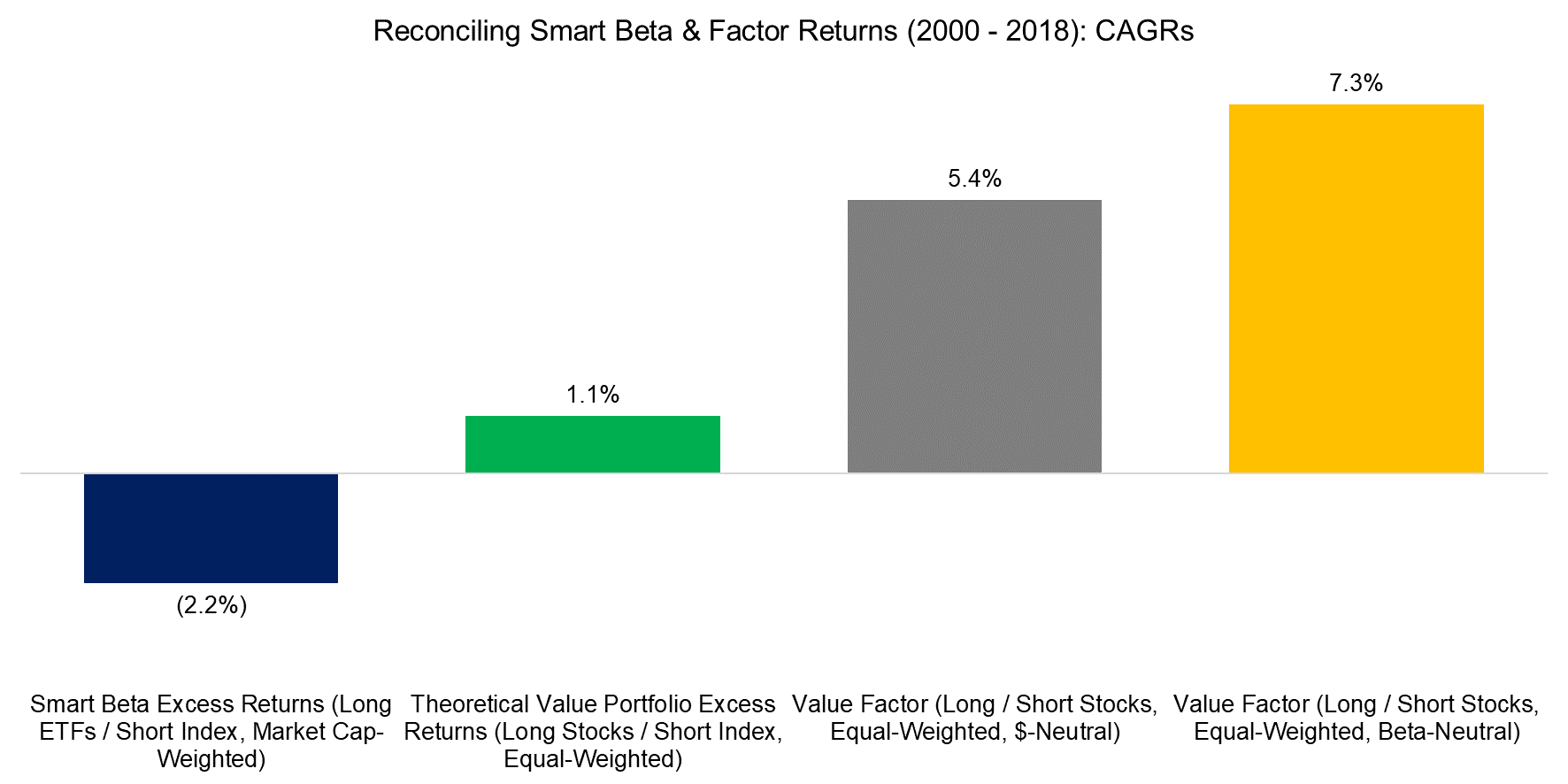

RECONCILING SMART BETA AND FACTOR RETURNS

Given that some of the smart beta Value ETFs have been launched in 2000, investors can analyze the excess returns by subtracting the market performance. Unfortunate, this analysis reveals that allocating to Value via smart beta ETFs generated negative excess returns. In contrast, a long-short Value portfolio as featured in academic research would have generated positive returns. We can reconcile these results via the following steps:

- Change weighting from market capitalization to equal allocations

- Replace the index short with short stock positions, which are additional profit centers

- Remove any beta exposure by allocating beta-neutral to the long and short portfolios

The reconciliation can be challenged by that costs are not correctly reflected. We assume 10 basis points of cost for each stock transaction, but additionally would need to reflect management fees, fund operating expenses, and stock loan fees for the theoretical Value portfolios. Although this would reduce the returns per annum, the factor returns would still be significantly above the excess returns from smart beta ETFs.

Source: FactorResearch

FURTHER THOUGHTS

Investors have allocated more than $1 trillion to smart beta ETFs, which is approximately 20% of all ETF assets under management. Unfortunately, smart beta ETFs may not be such a smart choice given that they do not capture returns shown in academic research and are more expensive than plain-vanilla ETFs. Although the number of ETFs already exceeds 5,000, more innovation is needed to better capture factor returns.

RELATED RESEARCH

Smart Beta or Smart Marketing?

Smart Beta & Factor Correlations to the S&P 500

Smart Beta vs Factors in Portfolio Construction

ABOUT THE AUTHOR

Nicolas Rabener is the Managing Director of FactorResearch, which provides quantitative solutions for factor investing. Previously he founded Jackdaw Capital, an award-winning quantitative investment manager focused on equity market neutral strategies. Before that Nicolas worked at GIC (Government of Singapore Investment Corporation) in London focused on real estate investments across the capital structure. He started his career working in investment banking at Citigroup in London and New York. Nicolas holds a Master of Finance from HHL Leipzig Graduate School of Management, is a CAIA charter holder, and enjoys endurance sports (100km Ultramarathon, Mont Blanc, Mount Kilimanjaro).

Article by Factor Research