Kernow Asset Management’s commentary for the month ended September 30, 2025.

Read more hedge fund letters here

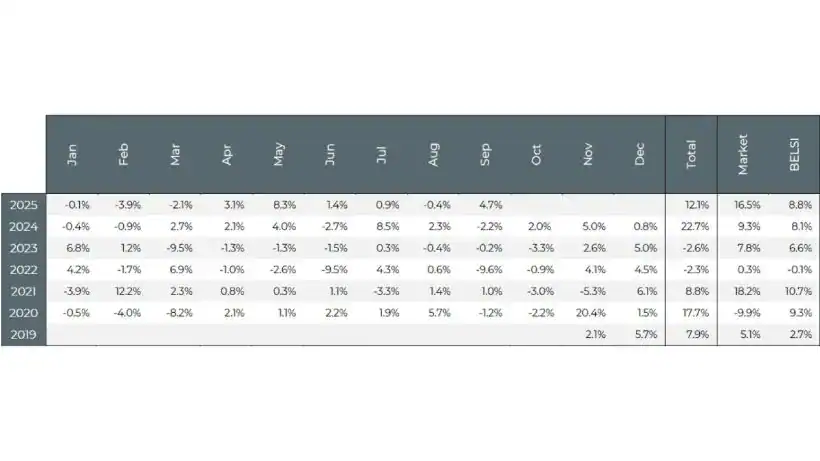

In September, the strategy delivered 4.7% as the UK stock market had its best summer since 2016.

The market has a confident spring in its step. It hit home when a sharp lawyer friend recently said he’s started trading shares!

Optimism spreads fast. That’s why Alyx spent the train ride home dishing out legal advice to strangers. Frankly, it’s a relief his friend isn’t a plastic surgeon.

The Makings of a Classic 10-bagger

Saga took centre stage as its interim results beat expectations. The new management team is proving it can steer this towards becoming a £100m free cash flow machine. The rise of the wealthy 50+ silver pound demographic may be the most potent and persistent force shaping Western economies today. It is more predictable than AI and one heck of a long-term tailwind.

A business in that space growing with solid metrics deserves a premium rating. Yet, its market cap sits at just £400m. For context, the founding family sold Saga in 2004 for more than £2bn in today’s money. That was before private equity got hold of it and bled it dry.

Wise Up on Underpriced Financials

Wise appears meaningfully undervalued when compared to Revolut’s latest US$75bn valuation round. That comparison implies a fair value for Wise closer to US$35bn. Today, it trades at just US$14bn. The company’s US expansion is gaining real traction. If execution continues, a re-rating over the next 18 months looks well within reach.

Don’t You Know, Pump It Up. You’ve Got To Pump It Up

Kistos is pumping. Part one of our thesis has played out. Impressively for a resources company, execution has also been on schedule. The H1 2025 results reported production of 6,200 boepd, keeping the company on track to reach an average 8,000–9,000 boepd for FY 2025 now that the Jotun FPSO is online in the Norwegian Balder field.

We added to our position as liquidity allowed, taking advantage of the subdued share price. Upcoming milestones include additional 2C-to-2P conversion on the Balder asset and then a refinancing.

Resource companies often carry a poor reputation, yet their simplicity is appealing to us. With no marketing, everything produced can be sold with virtually no effect on pricing. What matters is efficiency, discipline, and production rates.

Burning Questions at Drax

Speaking of energy, Drax has executed a herculean shift, moving from fossil fuels to become the UK’s largest renewable energy provider. It now supplies around 5% of the nation’s power. Our Kernow valuation framework indicates a value of £5bn. The market says £2.5bn. That gap made us take a closer look.

The crux is whether new favourable contracts will be agreed for its assets. Currently, these are disliked by all parties. Shipping Canadian forests across the ocean just to set them on fire in Yorkshire upsets everyone. Environmentalists call them a crime, fossil fuel loyalists call them a joke, and the trees are not particularly keen on it either.

Even so, power is life. Policy will change, and Drax has demonstrated its ability to adapt. We are drawn to this puzzle of uncertainty and have yet to figure it out. It could take more than a year.

Investigations into Pets at Home, Warpaint and Wizz Air

At first glance, Pets at Home appears to have the trappings of a quality business. Everyone likes animals, right? And a vet business must have huge pricing power. Then it just gets progressively disappointing the more work you do. As it stands, exceptionals riddle the operating model. Pass.

Warpaint, a cosmetics company, has flashes of quality. Our view matched the consensus to the letter. That’s another way of saying we had nothing new to add. Pass.

The amusingly named Wizz Air is an airline that has a questionable business model and a debt-laden balance sheet. It should eventually go out of business. Still, there is a small chance it might work. And strangely, this time does feel different for aviation. Yes, the most dangerous phrase in investing! We can already hear our future selves shouting.

Short Copper, Long Regret

We have been betting against a copper miner. The market didn’t care. It went straight up. Our thesis was based on a cost issue that led to a production miss. That was the trigger. Pull, nothing happened.

The green metal narrative was too loud, the trade bus was crowded, and we stepped in front of it. Bang. Copper stocks are up 55% in 2025 against an 18% rise in the metal, the widest differential in just shy of a decade. A lesson paid for in full, as our gold and silver longs were both taken over too soon to shield us.

Woman Wears Expensive Coat

In other top news, the wife of the most powerful man on the planet decided to wear a Burberry coat during the recent US state visit to the UK. The result? A £200m bump in its market capitalisation and fresh proof that the Burberry trench remains a timeless luxury staple. Hooray.

Since its inception in November 2019, the Kernow strategy is up 81%. This compares to the UK equity market, which has increased 54% over the same period. The collective upside in the portfolio is worth more than 216%.

- Book of the month: The Little Book of Mick by Michael O’Leary

- Good month for: Goodwin PLC, +41% on new client orders likely to develop to over US$200m

- Bad month for: Ocado PLC, -32% after its largest US customer announced a viability review

Sohn Conference Invite

Kernow has been invited to speak at the London Sohn Conference, the premier hedge fund conference in the UK. Interesting speakers pitching their best ideas. All for charity.

Tickets are priced at £600, and we have a limited number of complimentary tickets available for clients. First-come, first-served.

All the best

Alyx Wood

Chief Investment Officer

Kernow Asset Management

M: +44 (0)75 5458 3030 | kernowam.com