Moerus Capital Management commentary for the month ended August 31, 2025.

Read more hedge fund letters here

Always Running Towards the Fire

At Moerus, we often invest in companies with “hair” – be it corporate complexity, a weak outlook for the business, macro headwinds, industries in crisis, recent bankruptcies, technological obsolescence, etc. While most of our competitors seem to want to completely avoid these types of companies, seeking to only buy businesses that they deem “high quality” and that trade at a discount in their minds, we believe that the real bargains are found when a company is widely perceived to not be “high quality” – when the consensus outlook for the business is poor for a variety of reasons and most investors just sell without thinking about it further. In other words, to us, Trouble is Opportunity. Many investors have opted to avoid the career risk and extra work entailed in going out on a limb to invest in the opportunities that trouble sometimes provides. Why would they, as owning the same market darlings that everyone owns has been a winning strategy over the past decade? While we understand this approach, we believe, however, that it is precisely in these instances that real mis-pricings occur and great investment opportunities are found. In short, we believe that it is often profitable to run “towards the fire” to find investment opportunities, in stark contrast to the majority of other investors who are just trying to avoid trouble – or even just short-term discomfort. Many investors prefer not to take this approach – be it for comfort of their daily life or, more likely, career risk – but that significant value can be found by looking where others don’t.

In practice, this means that we are quite often looking for investments in areas shunned and disliked by the broader market. Often, this is a result of a consensus view that a business has a challenging mid-term outlook. The perceived safety in numbers results in most investors steering well clear. However, when everyone is running away from a sector, geography, or company, we have found that it is often times a fertile hunting ground for attractive investments. Despite decades of evidence to the contrary, most market participants believe that they can predict the future and can profitably invest with that superior insight as to what the future will hold. We continue to be stubbornly doubtful of our, or anyone’s, ability to do this in a consistent fashion and instead seek to invest in situations where the consensus view is so negative and expectations so muted for a business that there is a discount to the “here and now” value of the company.

To Fear Is Human

Humans long ago evolved to avoid danger. Be it tigers, crocodiles, natural disasters, or just the daily search for sustenance, humans have developed a keen sense for avoiding danger – eyes that better detect distance and movement to spot predators, the anxiety still present for many of us in daily life, and the safe feeling of being part of the herd are just some examples. This innate fear of danger carries over to investing, with investors being influenced by the ever-present desire to over-diversify, the perceived safety of the herd – be it through passive investing or just not looking too different from others – and the simplicity of extrapolating the current environment well into the future and not considering drastic changes.

Behavioral biases in investing and the human emotions underlying them have been written about extensively and we don’t have anything novel to add. Rather, consistent with many of the things we do at Moerus, we view the topic from a different perspective and try to add value by doing so. The general consensus in investing is that risk is simplistically the volatility of price – statistically the standard deviation of prices – and more volatility is near-universally viewed as bad. As such, investors long ago learned that successful investment strategies should only be viewed through a risk-adjusted context. Achieving high returns by taking inordinate amounts of risk is not impressive, it’s just lucky. Most investors seek to minimize risk and maximize potential return.

The result, to us, is that everyone’s investments look more and more the same as investors seem to only be seeking to buy companies that have been deemed by the market to be “high quality,” as there is perceived safety in doing so. This is viewed generally to be less risky. We at Moerus are not different in wanting to manage and avoid risk to the extent possible; where we differ, however, is the way we define risk. We believe that a more thoughtful definition and understanding of risk can allow us to seize opportunities that others miss.

Take a Risk

We believe the term “risk” is incomplete without an adjective. To most investors, risk seems to be a generic term representing the chance a stock price will decline. From an investing perspective, risk is widely perceived to be one form or another of a statistical measure of volatility, generally derived from looking at the historic price movement of a stock. We view risk as significantly more complex than just a backwards-looking statistical measure of price movements and, as such, always use a qualifier to specify the type of risk we are talking about:

- Market Risk: The forward-looking expected potential variability (up and down) of stock price.

- Price Risk: A risk that results when the market’s optimistic expectations for the future are priced in, creating downside risk if reality doesn’t live up to lofty consensus expectations.

- Business Risk: The forward-looking risk that the net asset value of the business underlying the stock may be fundamentally impaired in a permanent way.

At Moerus, we seek to avoid Business Risk and Price Risk as much as possible, but we in fact embrace Market Risk as a positive since we believe it often creates opportunity. Simplistically, we want to buy stocks that are perceived to have high Market Risk, as this results in discounted prices and upside potential. In looking for these stocks, though, we seek out companies that we think have limited Business Risk (limited risk of a significant impairment of capital). Separating the Market Risk of the stock from the Business Risk of the company is key. For a more in-depth analysis of risk, we suggest looking at our Investor Memo Perspectives on Risk: How You Can Lose Money – Let’s Count the Ways! At Moerus, the focus is – and always will be – primarily on trying to avoid losing money.

Additionally, we also strive to avoid companies that we believe have Price Risk, where expectations priced into the stock by the market may reflect overly optimistic scenarios. To do this, we seek to buy stocks that trade at significant discounts to our estimate of their intrinsic value in the “here and now” – not at discounts to an expected future. This is most easily done by avoiding stocks with optimistic outlooks that are currently in vogue with investors and tend to represent a significant portion of both indices and active investors’ portfolios. In our opinion, these “market darlings” may be perceived to have high upside potential in the market’s view, but we worry that they also come with high downside potential if reality falls short of the blue-sky expectations underpinning the stock price.

A Ship in Harbor Is Safe, but That’s Not What Ships Are Built For

As noted, most investors want to minimize volatility at all costs. In our opinion, this is an understandable yet overly simplistic approach, as volatility begets opportunity. The more volatility a stock price experiences, the more there is a chance of significant mispricing, and thus a greater chance for potentially outsized returns. When a stock is well-followed and liked by the market, there are many more eyes on it and the potential for mispricing is likely lower. While it is understandable that most investors say they look to maximize returns and minimize risk, they are likely doing it with the selfish ulterior motive of trying to avoid losing their jobs. Sticking one’s neck out and buying companies that are not as widely understood, covered, “high quality,” or liked may increase career risk. We believe that this is one of the reasons why the investment approach we use works – because the majority of others are afraid to do it! At its base, the relationship between supply and demand determines price. So, it is not surprising that stocks that have less demand (fewer potential buyers) and more supply (more potential sellers) will provide bargain purchases. A key factor in success here, though, is to sift through all of these bargains to find companies that have some lasting underlying value and do not have Business Risk. Most other investors are scared to follow this approach because if it doesn’t work out in a short enough timeframe, they may not be able to last long enough in their job to see it to fruition. At Moerus, we have built the firm around this approach, so sticking it out for the long term is deliberate, rather than a function of the time it takes for the market to come around.

At Moerus, our patience with investments and our willingness to look completely different than the index and others is a benefit that we seek to take full advantage of: we don’t focus on short-term performance, rather seeking to judge success over a full market cycle, and we are willing to have significant “tracking error” versus the index. We build our portfolio from the ground up, identifying attractive opportunities on a company-by-company basis, not seeking to build out a portfolio with targeted macro exposures. Lastly, we also have the luxury of having intelligent, thoughtful, and mindful investors. We spend a significant amount of time writing about our investments and educating our investors as to what we are doing. Consequently, we have investors who understand what they have purchased with our Strategy and its place within their overall allocation. Unlike others, we are not beholden to bureaucratic, annual reviews that can significantly diminish one’s propensity to take on risk. Quite the opposite, we seek to exploit the differences between price and value that are in part a direct result of others’ inability or unwillingness to capture this benefit – even if this may be uncomfortable while we are waiting for the investments to mature. While others may seek to outright limit their Market Risk, we look to maximize it (ideally on the upside), while seeking to avoid Business Risk and Price Risk at all costs. It should be understood by investors and prospects alike that, while we feel confident that this investment approach will work over a full market cycle, its return profile can be quite lumpy in nature, and it can look extremely different on a year-by-year basis than one might expect. While it is more uncomfortable, we at Moerus are willing to take the “career risk” inherent in investing away from the crowds, as we believe that this can result in attractive returns.

Simple, but Not Easy

While following the philosophy of investing when others are extremely fearful is simple, it is not easy. In fact, even though we write openly and in depth about our individual investments, it is not often that we see people copying these ideas. In principle, this approach is straightforward, as it does not require higher quality or more timely knowledge in order to gain an edge; but it does demand a level of conviction in thinking and willingness to stomach volatility that some investors cannot bear – be it for fear reasons or for career risk reasons. Specifically, this approach requires that we have:

- A willingness to look where others can’t or won’t, and comfort with sticking far out from the herd. In our view, well-known and well-understood securities are less likely to be significantly mispriced most of the time. Further, even well-known businesses sometimes offer bargains when they run into trouble, and we have either a non-consensus view and/or a longer time horizon. Hence a willingness to look while others are turning away is important, too.

- A deeper knowledge of the businesses that we are investing in, including a detailed understanding of a business’ drivers, as well as its various risks – both internal and external to the company.

- Patience to stick to a long-term time horizon and willingness to have flexibility on timing. Each investment has a life cycle of its own, with the holding period ultimately a result of a range of factors both market-related (investor interest and multiples) and market-independent (resource conversions). We have little to no control over the timing of these events.

- An opportunistic mandate across geographies, industries, and cash holdings. We need to be able to take advantage of opportunities where and when they arise and a willingness to hold cash if they don’t.

While this all seems pretty simple, in practice, it does not appear to be something that many other investors are striving to do. On the contrary, following more than 15 years of ultra-low interest rates and easy money and the supremacy of growth, not only are there fewer people following this approach each year, but these investors who do follow this approach will tend to underperform indices in consistently rising markets. As a result, even the managers who follow this approach that don’t go out of business face significant headwinds.

So, What Does It All Mean?

We have long believed that forecasting near-term economic variables is not a particularly productive use of our time, given our view that such forecasts rarely prove accurate enough – or consistent enough – to merit basing investment decisions on them. The last few years have done nothing but reinforce our long-standing view, as forecasts of many economic and financial market pundits have once again been off the mark on various topics, such as recession or no recession, the short-term path of inflation and interest rates, etc. Our crystal ball is no clearer than anybody else’s, and thus forecasting is hardly of any interest to us as a long-term investor, except to the extent that the fallout from volatility in near-term market expectations provides attractive investment opportunities from a longer-term perspective. This is where “Trouble Is Opportunity” is put into action. The on-again, off-again, ever-changing landscape surrounding tariffs is a current example. Forecasting the evolution and outcome of the tariff drama might be fun for some, but in our view, efforts to profitably invest capital based on the accuracy of these forecasts may well prove ill-advised. It remains unclear whether the administration’s ultimate goal is to gain concessions within the existing system or to seek a new system altogether. One thing that is clear, however, is that all of this uncertainty creates a lot of “trouble.” Needless to say, we are not confident of anybody’s ability (including our own) to accurately predict what the outcome will be, and we certainly don’t want to base investment decisions on any such predictions.

Fortunately, we do not have to. Instead, we maintain our long-term focus and seek to take advantage of the opportunities made available by heightened volatility that may very well continue. In recent years, we had already seen a healthy, increasing number of attractive long-term investment opportunities become available amid the short-term volatility in financial markets’ expectations and notoriously fickle macroeconomic forecasts (interest rates, inflation, etc.). That was before the recent tariff-induced surge in volatility. Although times like these are never pleasant to live through, we believe such volatility is more friend than foe to the long-term investor. We believe that our long-term perspective is one of the most significant advantages that we have during highly unpredictable, volatile periods. For the many other investors who are more focused on the short-term – either by choice, mandate, or financial necessity (e.g., those who invest on margin) – extreme volatility is their enemy, as it could result in forced or motivated selling at discounted prices that may not appropriately reflect longer-term, fundamental values. This often creates opportunities for the patient, long-term, price-conscious investor who is willing and able to tolerate day-to-day volatility in order to obtain compelling bargains over the long run.

Over the years, previous periods of extreme market turmoil – the Asian Financial Crisis, Global Financial Crisis, European Sovereign Debt Crisis, and the COVID-19 pandemic are some that come to mind – ultimately proved to have provided exceptional long-term buying opportunities for those who were able to be patient and stay focused on valuation, fundamentals, and the mitigation of the risk of permanent capital impairments (the latter not to be confused with day-to-day volatility). We believe that it is during such times that the seeds of attractive long-term capital appreciation are planted and that we are currently in one of these periods. Those able to zoom out from the wild swings in sentiment on intra-day tariff-related headlines and focus instead on long-term, fundamental business values will likely find some very interesting – and profitable – long-term investment opportunities. To use the well-worn cliché, today’s tariff-induced volatility is likely another of those moments where “babies might have been thrown out with the bathwater,” and our goal is to take advantage of the fleeting opportunities that such volatility provides (and maybe save some babies in the process).

Indeed, it is worth noting that three of the largest contributors to the Strategy’s second quarter performance are companies that were added to the Strategy just this year. Furthermore, relative to our past years of experience, we believe that there is currently less competition for the deep value, out-of-favor opportunities that we seek – perhaps as a result of both attrition among the ranks of value investors in recent years, style drift towards Growth among those Value managers who have modified their approach to fit the market zeitgeist, and a persistently long period of outperformance by Growth strategies that makes Value Investors look like dinosaurs. We believe this combination of factors bodes well for the Strategy and for our investment approach looking forward. While the fashionable approach may be to follow the flavor of the day (or the flavor of the past decade and a half), we at Moerus continue to be resolute in the belief that our investment approach will deliver attractive returns to investors over the long-term. While others may be running away, we run towards the proverbial fire, seeking the opportunity that is contained within the trouble.

When everyone looks more and more alike, we think it’s even more important to have differentiated portfolio allocations. We believe all portfolios should have exposure to strategies akin to what we do at Moerus and even more so in concentrated markets like today. While investors may think they are minimizing volatility buying the same securities as everyone else, this may have the undesirable result of actually increasing correlations within their portfolio and thus increasing overall risk. Put succinctly, while many investors feel that they have to own the Magnificent 7 (the There Is No Alternative or TINA argument to avoid career risk), we feel that a portfolio like ours provides an essential counterweight to this allocation – delivering respectable performance despite not owning the Magnificent 7 while providing a return profile that has proven to be – and will likely remain – less correlated with markets in general.

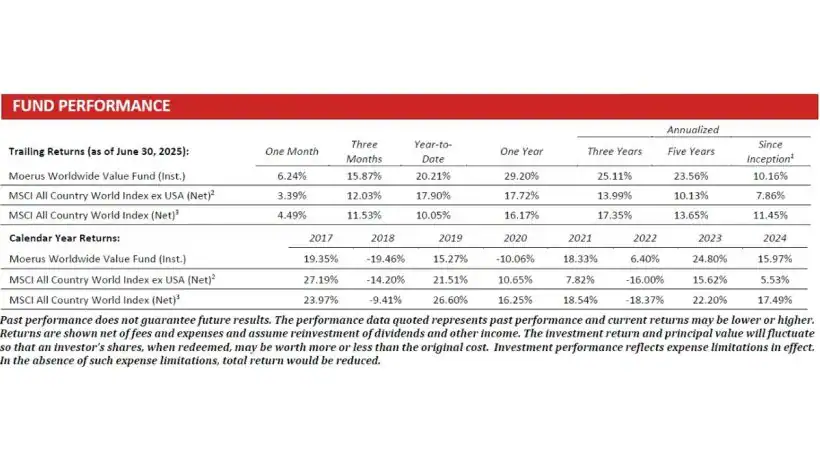

See the full factsheet here.

About Moerus Capital Management

Moerus Capital Management was founded in 2015 and is a 100% employee-owned organization. We run one global, deep value investment strategy that utilizes an opportunistic approach that results in a concentrated portfolio of securities in developed, emerging, or frontier markets where we are seeing the most attractive long-term opportunities. The investment team led by Amit Wadhwaney, Portfolio Manager and Co-Founder, has worked together for more than 15 years and has experience investing in most countries around the world.