RPD Fortress Fund’s commentary for the month ended August 31, 2025.

Read more hedge fund letters here

The estimated performance figures net of fees as of Aug 31, 2025

| Month | Year to Date | Inception to Date* | |

|---|---|---|---|

| RPD Fortress Fund | 1.10% | 7.26% | 29.29% |

| BarclayHedge Equity Long Short Index** | 0.38% | 7.42% | 22.80% |

| US High Yield Corporate Bond Index | 1.10% | 6.23% | 24.77% |

Performance Statistics

| Annualized Net Return | Volatility | Sharpe | Sortino | Positive Months |

|---|---|---|---|---|

| 10.45% | 1.78% | 3.55 | 6.78 | 97% |

*Inception date – February 1, 2023

**Based off reporting by 11 funds as of Sep 2, 2025

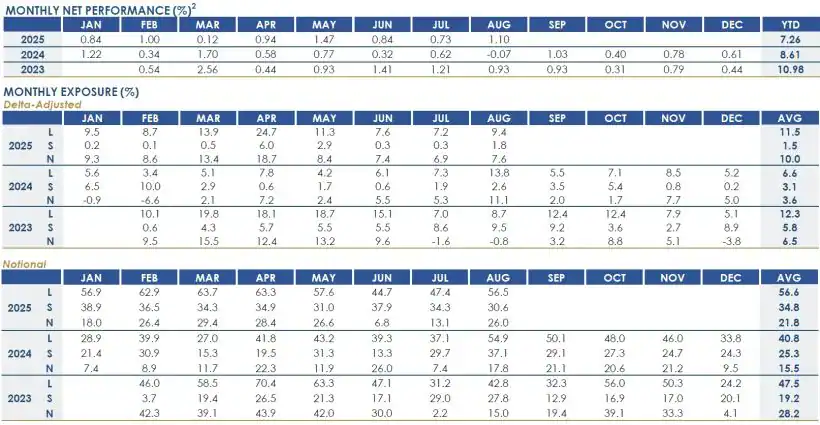

RPD Fortress Fund returned +1.10% net in August, bringing year-to-date net performance up to +7.26%. The Fund has now posted positive results in 30 of the past 31 months, underscoring consistency across diverse market environments. This consistency has been achieved with a strict policy of no leverage, including on a notional basis.

Performance in August was driven primarily by 15–30% out-of-the-money cash-secured put selling, supported by contributions from 25–50% out-of-the-money cash-secured call writing. While gains were spread across holdings, Appian (APPN) emerged as one of the more meaningful contributors. Appian develops low-code automation software, helping enterprises streamline workflow and digital transformation efforts. Ahead of earnings, option premiums were attractive, and we wrote puts accordingly at strike prices that represented very compelling valuation levels relative to Appian’s sticky product retention levels. The company went on to report solid results, and those options expired worthless. Throughout the year, we have opportunistically written puts on this name that has been thoroughly researched by our team, and the ability to repeatedly underwrite and re-enter positions at attractive strike levels highlights the robustness and repeatability of the strategy. TMT and consumer discretionary exposures were the leading sector contributors.

Average notional exposure in August was 56.5% long and 30.6% short, equating to gross exposure of 87.1% and net exposure of 25.9%. On a delta-adjusted basis, long exposure averaged 9.4% and short exposure averaged 1.8%, resulting in gross exposure of 11.2% and net exposure of 7.6%.

As of month-end, the portfolio included positions across a variety of sectors including software, retail and apparel, semiconductors, consumer products, cybersecurity, AI infrastructure, e-commerce, gaming, and digital media. All options sold were fully cash-covered.

The Fund ended the month lightly invested, as fewer opportunities met our strict underwriting standards amid a lower-VIX environment. That said, the strategy has historically demonstrated both the discipline and patience to wait when conditions are less favorable, and the agility to quickly redeploy capital when volatility rises or individual opportunities emerge, allowing us to act decisively at attractive strike levels.

August was characterized by continued expectations for Federal Reserve rate cuts, alongside signs of softening labor dynamics, particularly for younger workers entering the job market. Equity markets proved resilient, but underlying fragilities exist as participation breadth remains constrained. Consequently, discipline in strike selection and valuation are essential as we continue to prioritize strong downside buffers and robust risk management.

If you have any questions or require additional information, please contact Investor Relations at [email protected].

Best regards,

RPD Fund Management LLC

(212) 201-2650