Kernow Asset Management’s commentary for the month ended July 31, 2025.

Read more hedge fund letters here

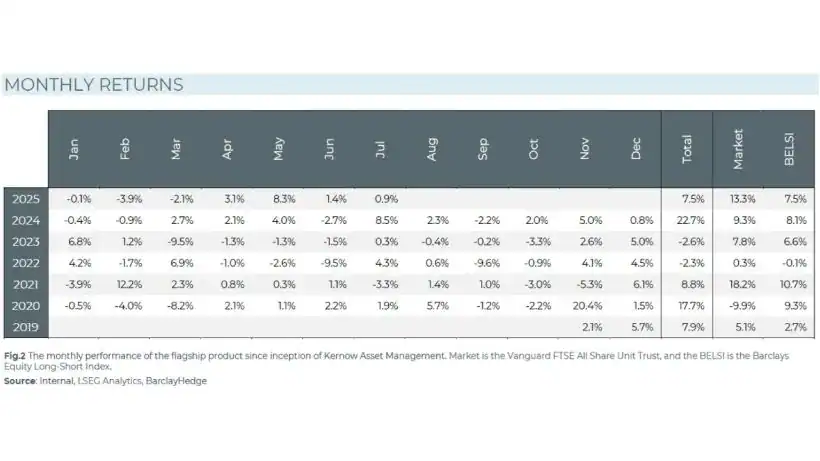

The strategy delivered 0.9% for July as our junk stocks gave us performance indigestion.

Faith in Fundamentals, Pain in Practice

We sleep well at night knowing we are long quality and short junk. The occasional nightmare? Junk rallies.

In June, we commented that our shorts were giving us a menacing look. Junk stocks, long considered financial compost, have suddenly become tulips. Last month, they soared. We did not.

What Is a Junk Rally?

This is when companies with weak balance sheets, little earnings, high debt, or even those near bankruptcy can see regular share price rises.

- A company cuts its earnings forecast, and the share price goes up.

- Another admits it’s out of cash and plans a dilutive raise. The share price goes up.

- A loss-making company with no product says it will present at a conference. Oh là là. Its market cap leaps by £30m.

- Number go up. Our IQ go down.

Of course, greed is good. It is practically a precondition for capitalism. Sure, it is fun to have chocolate cake for breakfast, lunch, and dinner. Eventually, the sugar rush fades, or you end up vomiting on the carpet.

The market works the same way. When the next sell-off comes, several of our shorts, which are near the end of their catalyst lives, will be covered. We have few worthy replacements right now.

Luxury on the Rebound

Alyx used to work opposite Burberry’s head office on Horseferry Road. The local pub had a coven of fashion designer girls. His friend dated one. He followed suit. Moths to a flame.

He started dressing better. It made him feel more confident. This led to a revelation that you can charge anything when you’re selling aspiration. Since that day, we have consistently sought to acquire luxury goods businesses during market downturns. To own Burberry today, at this price, in a fresh bull market, is nothing short of remarkable.

The business has officially turned the corner. It is profitable and might even have a march on Kering’s Gucci. Our hope is a five-year runway of growth from here. We now hold a full portfolio weight of 9%, supported by a substantial unrealised profit cushion to absorb any missteps along the way.

Card Factory Becomes the Second Largest Online Player

Card Factory acquired Funky Pigeon, the online cards and gifting business, from WH Smith for £24m. The seller was motivated, thanks to a change in ownership, and Card paid just eight times profit.

It gets better. Customers do not need a VPN to access the website, and management expects to extract an additional £6m a year in synergies. That implies a payback period of roughly three years.

Looking ahead, Card has serious work to do if it wants to turn the category into a true UK duopoly. Its main online competitor is the rudderless Moonpig, a larger machine with about eight times the revenue and a far superior website.

When Beating Expectations Becomes a Habit

We are starting to suspect that “Galliford Try” is a lost Latin phrase for “under promise and over deliver.” Once again, it is trading ahead of expectations.

Not to be outdone, Saga appears to have found some cash down the back of the sofa. Buried in an otherwise humdrum RNS was the news that it received £17m more than expected from the sale of its insurance underwriting business. The share price did not even flinch.

We would have bought more of both if we were not already full to the gills.

Hard Truths About Hard Liquor

It seems we struck a chord with our last factsheet. No one mentioned plastic forks or safety valves. Everyone had something to say about drinking. Young people told us they enjoy drinking too, when they can afford it.

It is not embarrassingly cheap to own yet, but a CEO transition is underway at Diageo. We are meeting with management soon to look for a clear catalyst. Selling off operations, such as Guinness and the East African business, is one path. Shifting toward a brand franchise model is another.

The incoming CEO will undoubtedly have their hands full. The company is not as high-quality as many think. The industry has a long history of overpaying for brands and unloading them at the lows. Inflation-adjusted profits peaked in 2013! Also, from what we can see, there is a four-year surplus of Scottish whisky stored in two warehouses.

So, drink up.

Since its inception in November 2019, the Kernow strategy is up 73%, compared with the UK equity market, which has increased 50% over the same period. The collective upside in the portfolio is worth more than 227%.