“Here we are doing something that almost seems like a suicide mission…

increasing the size of the deficit while we’re raising interest rates.”

– Jeffrey Gundlach, DoubleLine Capital

I’d add to that quote by saying that the administration is doing everything they can to piss off all of the buyers of our debt. Entering into a trade war with your major trading partners at the same time you are increasingly dependent on their capital must be calculated into the bet. Gundlach’s quote seemed spot on to me so let’s take a quick look at debt, who we are dependent on and see if we can’t get a sense for what rising interest rates might mean.

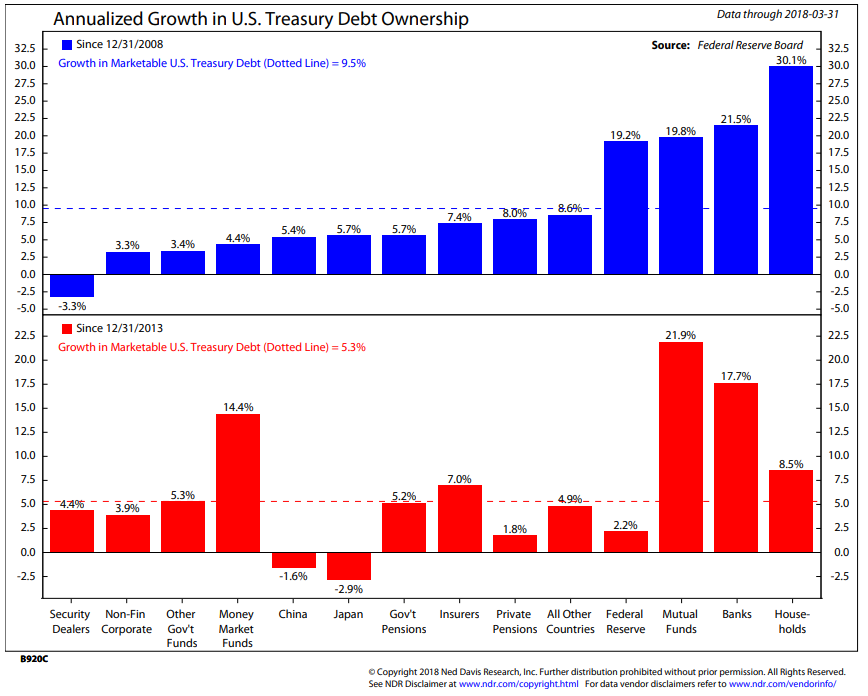

If we increase the size of the deficit, we have to finance it somehow and what we’ve been doing is issuing more debt to cover our expenses. In the following chart, take a look at the growth in Marketable U.S. Treasury Debt since 2008 (top section in blue)… and note the spike in the last few years. The bottom section (red) shows us who is buying the debt. Zero in on Japan and China.

Who owns U.S. debt? Thirty-seven present, or $6.2 Trillion, is owned by foreign investors. China is the largest foreign owner.

One of the problems is that much of U.S. debt is financed with shorter-term paper. So what happens when that debt needs to be refinanced? Gundlach sees interest rates rising to 6% by 2020 or 2021. That will pinch the pocket substantially. My friend, Dr. Lacy Hunt, sees interest rates moving lower. He believes that rising rates will quickly hurt the economy and drive us more quickly into recession. He sees lower rates in recession.

I’ve written about Gundlach and Hunt. Here and here:

- On My Radar: Mauldin Economics 2018 SIC (Part 3) – Jeffrey Gundlach, “Inflation is Inflationary” – 03-29-2018

- On My Radar: Mauldin Economics 2018 SIC (Part 2) – Dr. Lacy Hunt, “Economic Theory Matters, Especially So Now” – 03-23-2018

And as I looked back in the archives, I found this piece which pretty much hits to my point today – On My Radar: Stable and Unstable Financing Regimes — A Minsky Moment? You can find that link here. I add it because I think we are moving to that moment.

Anyway, I believe I can make a strong argument that both Gundlach and Hunt are right but really we just don’t yet know. Gundlach will tell you he gets about 70% or so of his calls right. Both are sharp and experienced managers. Dr. Hunt helps manage one of the best performing mutual funds of all time, the Wasatch Hoisington Treasury Bond Fund. The fund has essentially been invested in long-term treasury bonds for 25 years. Hunt remains long 100% treasury bonds with conviction that rates will move lower. Frankly, I’m not sure which of those two bets is right. That is why I prefer to let “price” tell me what is actually happening. More sellers than buyers or more buyers than sellers? Trend following can help.

My observation today is that if we piss off our investors, we’ll most certainly increase the number of sellers and decrease the number of buyers. That means higher interest rates. And if the Chinese want to retaliate by dumping their Treasury holdings on the market, rates will spike higher overnight. It is a risk and a hand the Chinese could play.

Right now, edge to Gundlach. I’m on record predicting higher rates in the short term, leading to recession and in recession we’ll see lower rates. But rates can rise even in recession. A problem we haven’t seen since the 1970s. For now, my trend signals, as you’ll see in the Trade Signals section below, point to higher interest rates. And the Fed remains motivated in that direction.

Rising interest rates and near record global debt are a toxic brew. Perhaps the biggest macro trend for us to keep site of is that we are at the end of a long-term debt super cycle. The last time we were in a similar position was in the mid to late 1930s. Income plus borrowing gives us more to spend. That’s good for an economy as it causes it to cycle higher. But too much debt means your brother has limited ability to borrow, less to spend. Deleveraging begins, especially if he is nearing retirement, and his economy slows. That’s what the end of a debt super cycle looks like. Rising interest rates make that debt more expensive and further stresses the system.

Debt’s the issue and debt dependency is pretty much everywhere. The next recession will prove more challenging than the last two. Those brought us 50+% equity market corrections. Rising rates draw that date forward. In recessions, all the bad stuff happens. I suspect the next one will bring us equal or greater decline in both U.S. and global equities and a record corporate default wave. I believe getting the recession timing right is critical. So we watch and remain on guard for recession.

I post my favorite recession watch charts about once a month. The good news is that they are signaling no sign of recession in the U.S. in the next six to nine months; however, the pressure is rising globally. One chart that caught my eye this week is the NDR Global Recession Probability Model I share with you next.

Here is how you read the chart:

- The current reading, as of June 26, 2018, is 59.32 (far right of chart). Circled yellow – note the rising trend in the model towards the upper red dotted line that marks the “High Recession Risk” zone

- The grey shaded areas show OECD-Defined Global Recession Periods

- The box in the lower right shows probability of global recession based on reading by zone

- The bottom dotted green line marks the “Low Recession Risk” zone

Bottom line: We are getting to the point where I’m beginning to get concerned. There is clearly a Rising Risk of Global Recession (call it a 51.55% probability today). Do note the 90.73% probability when the Model reading moves above 70. The temperature’s rising… Let’s keep watch.

“Here we are doing something that almost seems like a suicide mission…” Yes, and at a time when the market is late cycle, expensively priced, the economy is late cycle and the Fed is raising rates… more defense than offense until opportunity resets.

With all that said, I am seeing select opportunities that are really exciting and not dependent on the stock market to drive returns. I visited a company Thursday morning that a trusted mentor said may just be the single best investment opportunity he’s seen in his lifetime. I left excited… More on that front soon…

Next week we’ll take a look at what the latest month-end valuations are telling us about coming 7, 10 and 12-year equity market returns. I’ll also add a section showing my favorite recession watch indicators. The balance of the post is short. I received a number of kind notes following my piece last week about my great Coach Walter Bahr. Thank you. I was really worried that there was just too much of me in that piece. So sorry about that… Coach’s funeral service is today at 11 a.m. and being on time was mandatory. “It’s the little things boys,” he’d say. Can’t be late!

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

Included in this week’s On My Radar:

- Trade Signals — Risk of Global Recession Rising

- Personal Note — Walter Bahr

Trade Signals — Risk of Global Recession Rising

S&P 500 Index — 2,717 (06-27-2018)

Notable this week:

Notable this week: No significant changes since last week’s post. The overall weight of evidence continues to support a moderately bullish market outlook. The S&P 500 Index remains above its 200-day MA. Yet, keep in mind that the cyclical bull is aged and valuations are high. The shorter-term oriented CMG tactical equity trend models continue to signal caution with large exposures to Treasury Bills (information below). I find that particularly interesting and bears watching. The Zweig Bond Model remains in a sell as has been the case much of 2018. The short and intermediate term trend in gold remains down.

The next section walks you through all of the Trade Signals charts.

Click HERE for the latest Trade Signals.

Important note: Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Long-time readers know that I am a big fan of Ned Davis Research. I’ve been a client for years and value their service. If you’re interested in learning more about NDR, please call John P. Kornack Jr., Institutional Sales Manager, at 617-279-4876. John’s email address is jkornack@ndr.com. I am not compensated in any way by NDR. I’m just a fan of their work.

Personal Note —

As I finish today’s piece, it’s 10:30 a.m. and I’m rushing to Coach Bahr’s funeral service. “It’s the little things boys,” he’d say… meaning don’t mess up the little things. Being late was one of them. I remember an away trip where we’d head to Rec Hall, grab our uniforms and get on the bus. Coach would stand by the bus door. Late and you were left at the curb. No exceptions. The little things meant everything. Tie straight, sport jacket on, training focus… get all the little things right and the big things will take care of themselves he’d tell us. Amen Coach.

I arrived in State College last night and joined a dozen old teammates for a burger and beer. It was nice to see my friends again. The stories and poking fun was priceless. It feels like it was just yesterday.

My wedding anniversary is tomorrow. Number six and boy am I a lucky man. Susan and her youngest are in Boston for her son’s soccer tournament so I’m going to fly up tomorrow for the weekend. The weather forecast looks awesome. With no game on Sunday, our plan is to find a beach.

In mid-July, I’m taking the family to Maui. We are all excited but I have to tell you I’m getting a bit nervous. The last time I was there was in October 1987 with about 100 other Merrill Lynch brokers. If the market crashes again this time, we are going to have to create a new Trade Signal indicator – the Blumenthal in Maui indicator. You have to experience how people behave to believe it. It was insanity. Something you can’t read in a book. I’m really looking forward to some downtime.

I hope you have some vacation time in your near future. Hard to believe that the July 4 holiday is next week. Find a beach chair, a great book, hug your family and give yourself a hug too!

Wishing you and your family a wonderful 4th of July celebration.

♦ If you are not signed up to receive my weekly On My Radar e-newsletter, you can subscribe here. ♦

With kind regards,

Steve

Stephen B. Blumenthal

Executive Chairman & CIO

CMG Capital Management Group, Inc.

If you find the On My Radar weekly research letter helpful, please tell a friend … also note the social media links below. I often share articles and charts during the week via Twitter and LinkedIn that I feel may be worth your time. You can follow me on Twitter @SBlumenthalCMG and on LinkedIn.

I hope you find On My Radar helpful for you and your work with your clients. And please feel free to reach out to me if you have any questions.

Stephen Blumenthal founded CMG Capital Management Group in 1992 and serves today as its Executive Chairman and CIO. Steve authors a free weekly e-letter entitled, “On My Radar.” Steve shares his views on macroeconomic research, valuations, portfolio construction, asset allocation and risk management.

The objective of the letter is to provide our investment advisors clients and professional investment managers with unique and relevant information that can be incorporated into their investment process to enhance performance and client communication.

Click here to receive his free weekly e-letter.