Singapore Airlines is proposing to offer S$500 million of five-year fixed-rate bonds to both institutional and retail investors with a chance of it being upsized to $750 million if the response is overwhelming.

Q4 hedge fund letters, conference, scoops etc

SIA’s S$500m 5-year bonds will pay 3.03% interest and mature in 2024.

Below are my own personal opinions on the issue but the short summary is that I am not enthusiastic about the offering.

There are several main points that underpin it:

- Airline industry is fiercely competitive, and it is not going to get any easier anytime soon

The airline industry is notoriously competitive. It is notoriously capital intensive and low margin.

As Richard Branson put it best – “If you want to be a millionaire, start with a billion dollars and launch a new airline.”.

Just several headlines from the last few years from my time following the industry:

Fund injection into Malaysia Airlines continues: Khazanah – The Sun Daily

Shut down or sell off Malaysia Airlines, aviation analysts say – Today Online

At least 5 medium-size EU airlines to go bankrupt in 2018-2019 – Aerotime News Hub

And for those who remember the brief budget route between Singapore and London with Norwegian Airlines:

Norwegian Air Shares Plunge During Bid to Raise Cash – Bloomberg

And of course, the privatization of Tiger Airways by SIA in 2015 at 1/3 its IPO price.

Singapore Airlines to delist and privatise Tiger Airways – Business Times

The short of it is just that running an airline is one of the toughest businesses in the world.

As Buffett put it best, “When a management with a reputation for brilliance tackles a business with a reputation for bad economics, it is the reputation of the business that remains intact.”

- Huge CAPEX requirements and increased debt levels mean a weakened balance sheet

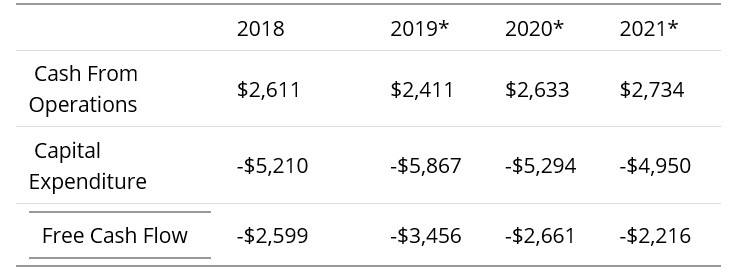

* estimates from Capital IQ

I think the numbers speak for themselves. SIA had a pretty strong balance sheet going into 2018 but that balance sheet is set to weaken dramatically as CAPEX requirements increase.

Not upgrading their fleet is not an option in the face of increased competition throughout the region. These cash expenditures will have to be funded either via debt or equity which is what is happening now.

- Assessment of what the next 5 years will look like

One of the most important things I stress even when it comes to bonds are that you still need to think about what the business will look like 5 years from now.

In this case, my job is to think about whether the money raised used to fund the aircraft purchases have a high chance of working out.

In this case, I can only describe my view as being… foggy.

As stressed earlier, the airline industry is notoriously competitive and we’ve seen a spate of airlines undergoing massive distress even with record low interest rates and a fairly benign operating environment.

I can only imagine the situation to be far worst in the case of a recession and find it hard to be optimistic given that other airlines are also expanding and upgrading their fleets throughout the region.

- Am I being compensated for the risk?

At the end of the day, it is all about the risk/reward ratio.

The Singapore Savings Bonds will yield about 2% if you take a 5 year maturity whereas the SIA 5 year bonds will yield 3%.

My own personal opinion is that I really can’t see the point of taking on this extra credit risk for an extra 1% of interest a year.

Ending Thoughts:

Given the stature of Singapore Airlines as our national airline and the pedigree of its largest shareholder (Temasek Holdings), I highly doubt that SIA will have problem refinancing its debt down the road.

Let me however, articulate a simple though experiment – if I showed you the financials above and didn’t let you know which company it was, would you be willing to lend it money at 3% for five years?

My answer is a solid no and hence I will be avoiding this issue this time round.

Additional Reading from Warren Buffett on Airlines:

“When Richard Branson, the wealthy owner of Virgin Atlantic Airways, was asked how to become a millionaire, he had a quick answer: ‘There’s really nothing to it. Start as a billionaire and then buy an airline.’

Unwilling to accept Branson’s proposition on faith, your Chairman decided in 1989 to test it by investing $358 million in a 9.25% preferred stock of USAir.

I liked and admired Ed Colodny, the company’s then-CEO, and I still do. But my analysis of USAir’s business was both superficial and wrong.

I was so beguiled by the company’s long history of profitable operations, and by the protection that ownership of a senior security seemingly offered me, that I overlooked the crucial point: USAir’s revenues would increasingly feel the effects of an unregulated, fiercely-competitive market whereas its cost structure was a holdover from the days when regulation protected profits.

These costs, if left unchecked, portended disaster, however reassuring the airline’s past record might be.

The reason why airlines have been such disastrous investments is their “insatiable” demand for capital, according to Buffett, who wrote the following in 2007:

“The airline industry’s demand for capital ever since that first flight has been insatiable. Investors have poured money into a bottomless pit, attracted by growth when they should have been repelled by it.

And I, to my shame, participated in this foolishness when I had Berkshire buy U.S. Air preferred stock in 1989. As the ink was drying on our check, the company went into a tailspin, and before long our preferred dividend was no longer being paid.

But we then got very lucky. In one of the recurrent, but always misguided, bursts of optimism for airlines, we were actually able to sell our shares in 1998 for a hefty gain.

In the decade following our sale, the company went bankrupt. Twice.

To sum up, think of three types of ‘savings accounts.’ The great one pays an extraordinarily high interest rate that will rise as the years pass. The good one pays an attractive rate of interest that will be earned also on deposits that are added. Finally, the gruesome account both pays an inadequate interest rate and requires you to keep adding money at those disappointing returns.”

Article by Jun Hao, The Asia Report