Dan Loeb’s letter to Third Point investors for the second quarter ended June 30, 2024. Read the full letter here.

Dear Investor:

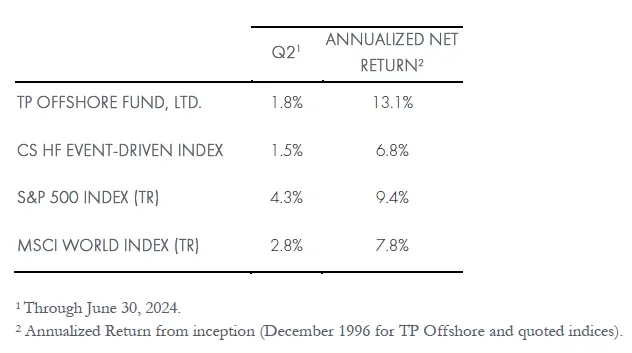

During the Second Quarter, Third Point returned 1.8% in the flagship Offshore Fund.

The top five winners for the quarter were Taiwan Semiconductor Mfg. Co. Ltd. (NYSE:TSM), Alphabet Inc (NASDAQ:GOOGL), Amazon.com Inc (NASDAQ:AMZN), Vistra Corp (NYSE:VST), and Apple Inc (NASDAQ:AAPL). The top five losers for the quarter, excluding hedges, were Bath & Body Works Inc (NYSE:BBWI), Advance Auto Parts, Inc. (NYSE:AAP), Ferguson Enterprises Inc (NYSE:FERG), Airbus SE (EPA:AIR), and Corpay Inc (NYSE:CPAY).

During the first half of 2024, the Offshore Fund generated profits across all strategies, posting a 9.8% net return. For the previous 12 months, the fund returned 17.0% net. While returns over this period were largely driven by technology companies, much of the portfolio is invested in a range of sectors including utilities, industrials, consumer, and healthcare that provide diversification and balance to the portfolio. Single name short equities were an important source of alpha during the first half of the year, and corporate and structured credit have contributed steady gains with a fraction of the volatility and risk of equities.

Our investments in the digital world including hyperscalers, consumer AI distribution platforms, and semiconductors have a key place in the portfolio, as we have discussed in previous letters. However, we are finding many investments in the “physical world” to be equally attractive. In a market consumed with technological disruption, we are focused on finding companies that are difficult to disrupt due to competitive moats, consolidated industry structures, unique products, or capital intensity that deter competitive investment. Examples include aggregates, nuclear power, life science tools, specialty alloy manufacturers, and commercial aerospace manufacturers. It is understandable that in a market whose narrative is dominated by the “Magnificent 7”, these businesses receive less attention, but that is giving us even more reason to add these types of names to the portfolio when we can find them.

All investors know that early August brought tremendous volatility in equity markets. While indices have largely recovered, we expect that volatility will persist into year-end with a number of macro events – from Federal Reserve interest rate decisions; to the US elections; to the possibility of escalating conflict in the Middle East, to name just a few – contributing to a choppy environment. We modified certain exposures with this scenario in mind and worked quickly to mitigate losses during the downdraft. We are eager buyers of dislocated securities, particularly in credit, should we see further turmoil.

Equities Updates

Apple Inc. (AAPL)

In April, we took a position in Apple, the world’s leading consumer technology franchise, with an ecosystem of 2.2 billion devices spanning a broad array of form factors including smartphones, tablets, laptops, watches, earphones, and smart home devices. Apple excels in most of these device categories, with revenue share of 50-60% in several key markets.

Despite Apple’s dominance as a business, its stock had become increasingly “under-owned” by institutional investors and its relative multiple had compressed toward a multi-year low. We believe that this was due to several years of stagnant earnings growth, exacerbated by more recent fears that Apple may turn out to be an AI loser. Our research led us to a different conclusion: we believe AI-related demand could drive a step change improvement in Apple’s revenue and earnings over the next few years.

Corpay (CPAY)

This quarter we added to Corpay (formerly FLEETCOR), a position we initiated in the Fourth Quarter of 2023. Corpay is a collection of network assets in the payments space, most notably a fuel card business, where the company processes fuel purchases by commercial vehicle operators, and a B2B payments business where Corpay facilitates vendor payments for midmarket clients. These two segments together make up >70% of Corpay revenues. The company is run by CEO of 24 years, Ron Clarke, who in our view has delivered an impressive track record for shareholders of 20% compounded EPS growth since going public in 2010, including 15% over the last 10 years, through a combination of revenue growth, margin expansion, and accretive capital allocation in M&A and share repurchases.

Over the last five years, CPAY has seen its P/E multiple significantly de-rate from the mid-20s to ~13x as market sentiment toward the company's core fuel card business soured. Firstly, growth in the segment has slowed as the market has matured. Secondly, the rise in popularity of electric vehicles (EVs) as a theme has made investors question the terminal value of a business whose main function is to process gasoline and diesel payments. Corpay has proactively prepared for an EV transition by making acquisitions in EV charging payments and adding mixed/EV fleets to its customer base, wherein CPAY earns higher unit economics on mixed fleets than it does on pure internal combustion engine fleets. Finally, the last year has demonstrated that a transition to an electric fleet is more easily said than done. With EV sales declining for industry bellwether Tesla, European EV sales declining overall, and flattening in the US, it is becoming clear that the journey of automotive electrification will be a long one.

Intercontinental Exchange (ICE)

During Q2, we added to our position in Intercontinental Exchange (ICE). We originally invested in ICE in April 2023 when the FTC’s challenge to the company’s proposed acquisition of Black Knight impacted the share price. While the deal overhang has lifted, we believe a re-rating opportunity from a structural and cyclical acceleration of growth is still ahead. Importantly, we expect that AI will drive new growth opportunities across most of ICE’s businesses, extending the runway for value creation.

ICE is a collection of dominant information services and exchange assets that automate diverse and large asset classes (Energy, Mortgages, Fixed Income, Rates and Equities) while producing vast amounts of proprietary data. CEO Jeff Sprecher has led ICE for over 20 years. Under his visionary leadership, the company has compounded organic revenue and EPS at ~5% and ~15%, respectively, and adopted new modalities through organic investment and strategic acquisitions, most notably creating the flagship clusters of Energy and Mortgage, franchises we believe are of very high business quality. On the horizon, we expect an acceleration of growth to a consistent low double digit organic algorithm in these businesses, and a re-rating of the stock as price follows value creation.

Credit Updates

Corporate Credit

Third Point corporate credit returned 4.4% gross (3.6% net) through the first half of 2024, outperforming the J.P. Morgan High Yield Index, which returned 2.6%. We suffered no material losses and our small position in GSE preferreds was up over 50%. Our relatively muted overall performance was due to a slower-than expected realization of the events that we expect will drive our positions higher, and continued weakness in the cable sector. We have both long and short positions in cable that we expect will perform well later this year as the winners and losers from changes in the competitive landscape become clear.

Structured Credit

We believe structured credit remains one of the last untapped markets for many institutional clients. We are seeing more insurance companies and private credit firms enter asset classes that we have been invested in for as long as seven years and welcome them to the table. Since the liquidity crisis some banks faced in March 2023, many credit funds have emerged to buy consumer loans, a trade we have executed with strategic venture partnerships since 2017 in our main funds and the dedicated structured credit funds. Today, private credit funds are driving up prices for sizeable loan trades from banks happy to sell and then provide expensive senior financing.

Sincerely,

Daniel S. Loeb

CEO

Third Point Management

Read the full letter here.