“I will go to my grave believing that the financial crisis happened because of bubbles made by easy money.” – Stan Druckenmiller, Former Chairman and President, Duquesne Capital (Bloomberg Interview)

I’ve seen three outstanding buying opportunities in my nearly thirty years of trading the high-yield junk bond market. Today, the high-yield bond market is full of the “junkiest” junk (a technical term) ever. My excitement level is growing. Opportunity number four is building. Post-2008 Great Financial Crisis, the yields on high-yield junk bond funds and ETFs were north of 22%. That was also the case in 1990 and 2002. For us investors, such high yields are really kind of yummy. I could be wrong, but I believe that the coming opportunity will be the single best one since I first began trading the trends in high yield in 1990. In a word, epic. I’ll try my best today to explain why and how today.

It begins with the death of covenants. This week, I’ve got another story for you, a summary of an excellent article from Bloomberg entitled, “The Birth and Death of Covenants” by Sally Bakewell and Lisa Lee.

Back in 1982, a group of bankers from Drexel Burnham Lambert headed to an elegant restaurant in New York City. The reason for their meal: to celebrate a junk bond deal that hadn’t ended in their favor. They had spent months working on a bond offering for Sparkman Energy Corp. Sparkman determined that the investor-protection covenants that Drexel had proposed for the bond were too strict. The company picked another firm.

Vince Pisano, an attorney who had played a part in the Sparkman deal, said some of the dinner attendees had belt buckles emblazoned with Sparkman’s logo—a line running through it. Little did they know, those buckles foreshadowed what would eventually happen. Five years later, Sparkman’s chairman, Wallace Sparkman, would settle with the SEC regarding an alleged kickback scheme, which he neither confirmed nor denied participating in.

That wasn’t the only harbinger, though. The legal aspects of the deal, developed by Pisano et al. in the 1980s, would become a junk-bond and loan market totaling more than $2 trillion.

In the quote above, Stan Druckenmiller was referring to the 2008-09 Great Financial Crisis, which was made possible by “easy money.” He pointed to the maestro, Alan Greenspan, former Chair of the Federal Reserve, and his successor, Ben Bernanke. When the Fed lowers interest rates, they make it easy for borrowers—a little too easy. If rates are low, borrowers can borrow even more. Bad behavior creeps in.

Do you know anyone who owns certificates of deposit (CDs) today? I remember trying to grow my client base in the 1980s. Almost everyone I talked to owned an FDIC-insured, bank-issued certificate of deposit. At your holiday party this season, ask your friends if they know anyone who owns one now. The answer is likely no. Why? A low 1.25% to 2% yield is why. That’s a negative return after inflation is factored in. Low interest rate policy is starving retirees, insurance companies, and pension plans. So what do investors do?

They step out on the risk curve. Money has poured into bank lending funds and riskier high-yield bond funds. Seems safe, but all that money is enabling borrows to borrow in ways that give the investor little protection. Let’s go back to the story.

Bakewell and Lee write, “Private equity firms such as Apollo Global Management and KKR & Co. have fought to make it easier for the companies they own to take on more debt soon after borrowing, and for debtors to sell off assets and pay the proceeds to shareholders”— a.k.a. themselves and their clients. “For a decade, they had already chipped away at other provisions in loans known as ‘maintenance covenants’—requirements that a corporate borrower meet specific performance hurdles or else be forced to renegotiate terms or even repay debt.”

The authors continue: “Private equity firms ‘began to select their investment banks based in part on who could get them the loosest high-yield covenants,’ says Kirk Davenport, a former partner at law firm Latham & Watkins who also worked for Drexel on early junk-bond deals. ‘And once they figured that out, the race to the bottom was on.’”

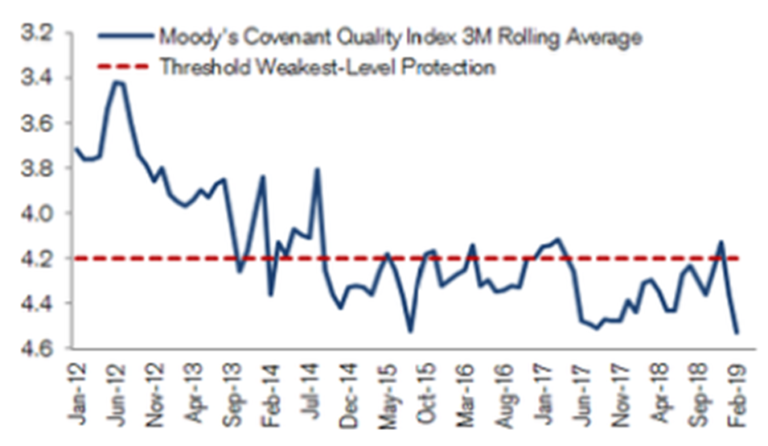

Moody’s is a rating firm that tracks covenant quality. Today, covenant protection has never been worse. Five is bad, one is good. This is the best chart I could find. While it’s a little blurry, the data is clear. A race to the bottom indeed.

I remember when the Moody’s Covenant Quality Index was at 2. Last February, it was at 4.5 out of 5. That means we should have our lights on.

In the past, if a high-yield borrower defaulted, the investor might get 75% of their money back. Bonds are senior to stocks in the capital stack. Stock holders might get wiped out if a company files for bankruptcy, but banks (which are first in line to get paid back) and bond holders generally have some assets pledged that enable them to recover their money. What might a lender expect to recover today? Strategists at UBS Group estimate that lenders might recover less than half of their money.

“According to S&P Global Market Intelligence’s LCD Unit, almost 80% of the outstanding loans in the market lack maintenance covenants in deals deemed ‘covenant lite.’” Bakewell and Lee explain that some companies use those weaker covenants to be able to “strip away collateral before a default to benefit equity investors at the expense of lenders.”

And who are those lenders today? Moms and pops invested in high-yield bond funds and leveraged loan funds, insurance companies, and pension plans. Those who sought higher yields due to the Fed’s zero interest rate policy. The trade of a lifetime is forming. Bubbles made by Easy Monetary Policy, Part II.

“The Birth and Death of Covenants” is available to you if you have a Bloomberg terminal. Click on over and give it a read.

Unfortunately, I can see the lawyers circling their wagons. Another class-action bonanza is on their horizon, made possible by lawyers, for lawyers. And some shrewd private equity investors. And our friendly central bankers. And investors. Who knew some people might behave badly… who knew? Here we go again.

You don’t want to be sitting on the tracks, all Champagne “bubbled up” in front of this oncoming train. Like the three times prior, a crash is coming. No, I can’t guarantee it—but boy, do I feel it in my bones. If you are invested in high yield like I am, there are a few indicators that can help you see when the train is coming, and how to easily and quickly step off the tracks. And, just as important, they can show you when to step back into the trade. I share them below. The other side of the next corporate bond market collapse, I believe, will be the next exceptional investment opportunity. 30% yields? Maybe. We just can’t get run over on the way to it.

Stan Druckenmiller and David Rosenberg

Bloomberg did an excellent interview with Stan Druckenmiller, in which he discusses his investment positioning and forward outlook. Druckenmiller no longer manages money for clients. A self-made billionaire, he earned his fortune as a global macro money manager and may go down in history as the greatest money manager of our day. Druckenmiller speaks critically of the Fed. He believes they are stuck and won’t be able to raise interest rates even when the need arises. And he gives us a peek into what he is doing with his own money.

I love his honest and blunt way. It’s worth the watch/listen. You can find it here. Put your walking shoes on, plug in and take a walk.

Good friend David Rosenberg was also interviewed by Bloomberg this week, and he warns of the spread between CCC and double-B rated debt, saying it is the “canary in the coal mine.” I mentioned in last week’s OMR post that we’d take a look at what is going on in the CCC-rated high-yield junk bond market today. What a gift from the writing gods in terms of the timing. Hat tip to good friend Kevin Malone for sharing David’s interview with me. Kevin said, and I believe he’s right, David’s interview might be the most concise summary of what is going on today.

You can view the five-minute interview here. Following are my short summary notes from the interview:

- It’s not just where the money has been borrowed, it’s where it has gone. This is the weakest capital spending cycle of all time in biggest boom in corporate bond issuance of all time. So where has the money gone? Two words: financial engineering (i.e., stock buybacks).

- That explains why earnings per share has been inflated and that is the biggest reason why we’ve had this ongoing powerful bull market in equities in the context of the weakest overall economic recovery of all time.

- It’s one thing to say you’ve had $4 trillion in corporate bond issuance to finance capital expenditure, you could say we are then going to have a productivity cycle that will lead to some internally generated rate of return that will then go to cover debt servicing costs. That hasn’t happened.

- You’ve got this symbiotic relationship where you’ve got this massive corporate bond issuance financing stock buybacks.

- It’s what I call smoke and mirrors. And you’re seeing it appear in the rate differential spread between CCC’s and BB bonds. That’s the canary in the coal mine.

Above we talked about counterparty risks and some of the covenant-lite shenanigans happening in the corporate funding markets. When you think about how the economic machine works, a strong capital markets structure is required to support and enable a country’s growth. The US has a strong capital markets structure: a broad and diverse number of players, banks, brokerage firms, venture capitalists, a Federal Reserve, Treasury, regulators, legal processes, and laws. Ours is not a perfect system. It needs improvement and it likely always will, but it is arguably the best system in the world. So put that in the good column.

“Follow the money trail,” my accountant father used to say. “Always look there first,” he’d tell me. And with an understanding of how the machine works, that’s what I’m trying to do with this missive on the high-yield junk bond market today. I hope I’ve made the boring interesting, but mostly, I hope I’ve turned a few lights on. I was young when I experienced the first dislocation and the second, and well, I’m not as young anymore. I see misbehavior and while I expect to be as nervous as I was entering the prior three trades, this next one looks to be the best one yet. The opportunity ahead will be anything but boring.

Some humans do bad things, but I think most people are really good inside, seek to do right, and find purpose and joy in serving and lifting others. Perhaps I’m naïve, but that is the world I wish to see, and the people I wish to be and create with. “Shine that light bright,” Mom would always say… and she’s right.

I do believe the key to getting the timing right is embedded in the trend in the high-yield market and the ability for borrowers to find money (lending conditions). Below you’ll find my favorite high-yield bond market signal indicators, along with my two cents on what I’m seeing today. Hint: Prices continue to trend higher, so I’m ending the year very happy. You’ll also find the link to the latest Trade Signals post along with a wish from me to you. Thanks for reading. I appreciate the time you give me. Happy holidays and happy new year to you and yours!

There will be no On My Radar post next week. Daddy needs to drink some fine red wine. Trade Signals will be updated next Thursday.

Find your favorite chair and, with coffee in hand, read on…

If a friend forwarded this email to you and you’d like to be on the weekly list, you can sign up to receive my free On My Radar letter here.

Follow me on Twitter @SBlumenthalCMG

Included in this week’s On My Radar:

- My Favorite High-Yield Market Indicators

- Trade Signals – An Eye on Inflation

- Personal Note – Ain’t No Shortcuts to Greatness

My Favorite High-Yield Market Indicators

Long-time readers know I’ve traded the intermediate-term trends in the high-yield junk bond market since the early 1990’s. From experience I can share that down trends in HY lead to down trends in the stock market, which lead to down trends in the economy. The really big investment mistakes come during economic recessions, so it’s important from a money management perspective to avoid the big dislocations that recessions tend to bring.

Two of the most important charts on my watch list follow.

This first chart plots the price trend of a large and popular high-yield mutual fund. The solid green line is a simple 50-day moving average price line. Signals occur when the price moves above or below the smoothed moving average trend line. The idea is to invest when the price trend is up (above the green line) and move to Treasury bills (BIL, for example) or cash when the price trend is down (below the green line). In particular, focus in on 2000-2001 and 2007-2009.

Source: stockcharts.com

While not all signals work, but in my experience the end result is worth the effort. You could use a 100-day moving average trend line or something shorter. The longer the smoothing you select, the fewer false signals, but the larger the accepted drawdown before moving to Treasury bills. When risk is highest (the yields low and the spread between high-yield bonds and safer Treasury bonds is low), you may wish to use a tighter stop-loss moving average signal line (i.e., something like a 50-day MA). After a major sell-off, risk is lowest and yields highest, you may wish to use a longer stop-loss moving average line (i.e., something like a 200-day MA). Please note: NOT A RECOMMENDATION FOR YOU TO BUY OR SELL ANY SECURITY. This is not personalized investment advice. Please consult your financial or investment adviser.

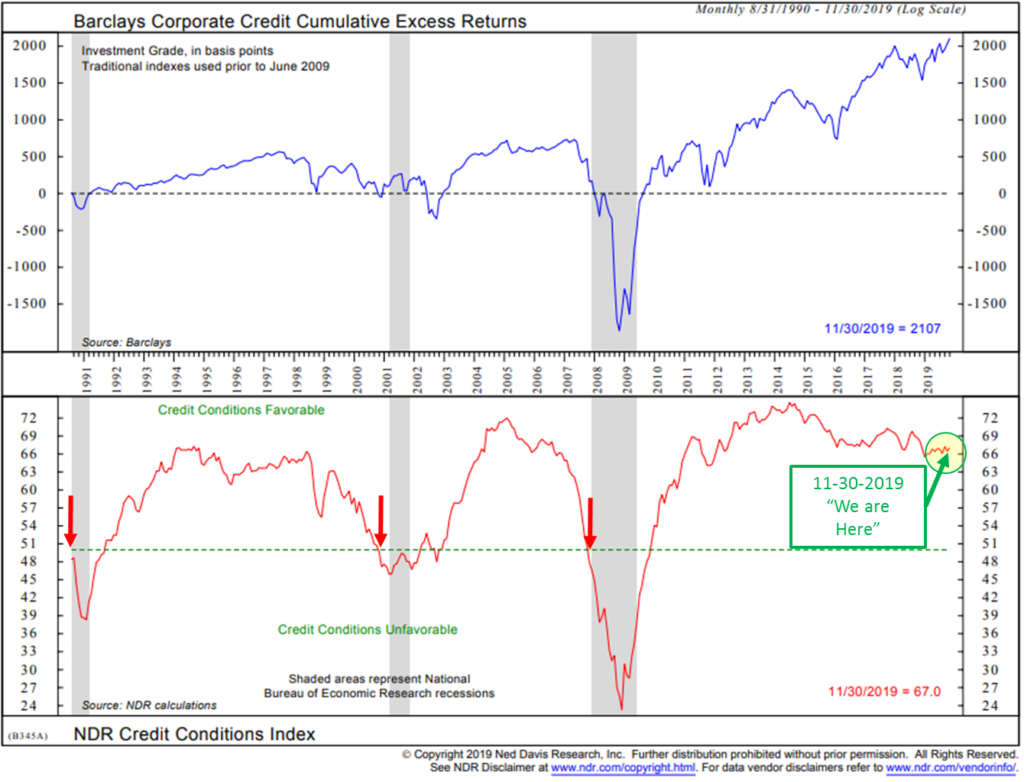

Now, where I think we can really zero in on timing of what I believe will be an epic wave in corporate defaults, combine what price is telling us (above data) with lending conditions. When the lending conditions turn from “Favorable” to “Unfavorable,” that’s when high-risk borrowers lose access to funding and default. Or as Warren Buffett says, when the tide goes out we’ll see who’s swimming naked. And this time around, a lot of swimmers will be left with their swimsuits on the beach.

Here is how you read the chart:

- Note the three red down arrows. They mark the times when the NDR Credit Conditions Index dropped below a reading of 50 (horizontal green dotted line in the lower section of the chart) signaling recession. The gray bars indicate periods of recession.

- The “We are Here” arrow shows the current credit conditions are favorable.

- Bottom line: Nothing to worry about at this moment. But do keep watch…

Source: Ned Davis Research; CMG Investment Research

With both HY in an uptrend and lending conditions “Favorable” grab a drink, love life and celebrate the holiday season in good cheer.

Take comfort in knowing there are things you can do to cover your backside.

Trade Signals – An Eye on Inflation

December 18, 2019

S&P 500 Index — 3,138

Notable this week:

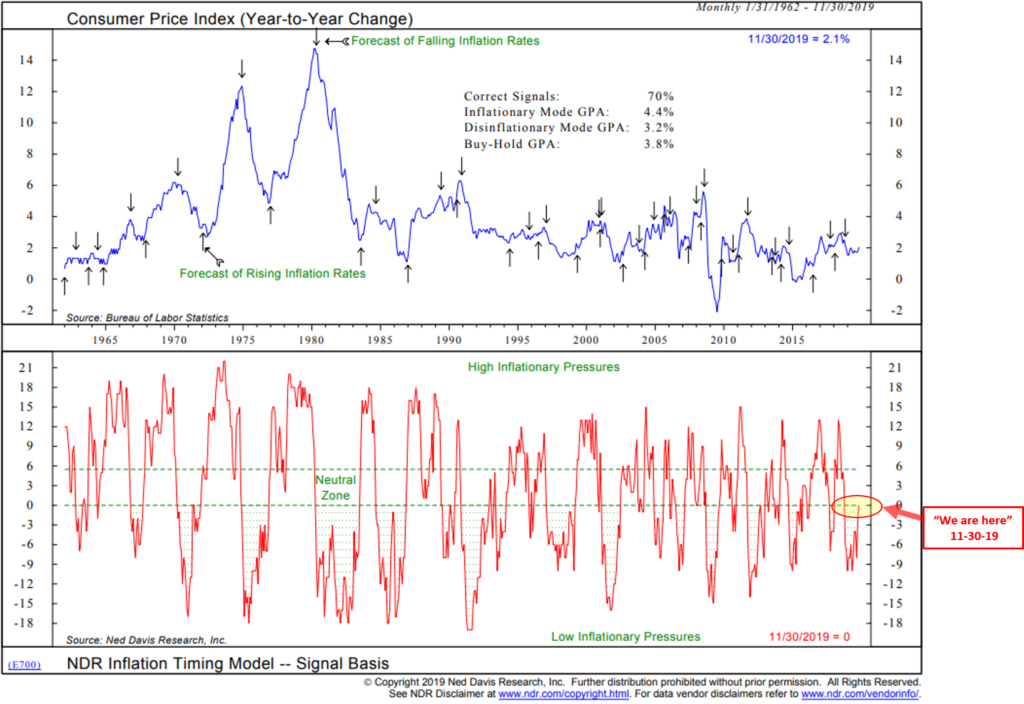

The trend for the equity market remains favorable. No signal changes since last week’s post. However, I am keeping an eye on inflation. The following chart is the Ned Davis Research Inflation Timing Model. My go-to inflation indicator. The model consists of 22 indicators that primarily measure the various rates of change of such indicators as commodity prices, consumer prices, producer prices, and industrial production. The model totals all the indicator readings and provides a score ranging from +22 (strong inflationary pressures) to -22 (strong dis-inflationary pressures). High inflationary pressures are signaled when the model rises to +6 or above. Low inflationary pressures are indicated when the model falls to zero or less. I focus on the bottom section of the chart. Higher inflation may prove to be a problem for the Fed at some point. Rates will rise and that won’t be good for the massive amount of debt that exists in the system. I’ll be touching on this in Friday’s On My Radar. The NDR Inflation Timing Model moved out of the “Low Inflationary Pressures” zone at November month-end and is in the “Neutral Zone.” Bottom line: No immediate concern but bears watching. (No pun intended.)

Not a recommendation for you to buy or sell any security. For information purposes only. Please talk with your advisor about needs, goals, time horizon and risk tolerances.

Click here for this week’s Trade Signals.

Personal Note – Ain’t No Shortcuts to Greatness

Merry Christmas, Joyous Chanukah, Happy Holidays and a Wonderful New Year to You and Yours

“Your vision and purpose are greater than your circumstances. Don’t look at where you are. See where you’re going and remember why you’re going there.”

“Your mindset causes the lens in which you view the world to narrow or open.

Negativity narrows your perspective and causes you to focus on problems.

Positivity broadens your perspective and allows you to see the big picture and find solutions.

Positivity sees possibilities!”

“No matter what anyone says, just show up and do the work.

If they praise you, show up and do the work. If they criticize you, show up and do the work.

If no one even notices you, just show up and do the work.

Just keep showing up, doing the work, and leading the way.”

Lead with passion.

Fuel up with optimism.

Have faith.

Power up with love.

Maintain hope.

Be stubborn.

Fight the good fight. Refuse to give up.

Ignore the critics.

Believe in the impossible.

Show up.

Do the work.

– Jon Gordon

“Ain’t no shortcuts to greatness, man.”

– Reggie Bush

Share the above with your kids. And also share this clip from Reggie Bush talking about Drew Brees entitled, “Work Hard in Silence.” It is absolutely awesome.

Again, happy holidays to you and yours. Thank you for reading.

Warm regards,

Stephen B. Blumenthal

Executive Chairman & CIO