The crazy ride in the stock market over the past week, losing nearly 140 points in the S&P 500 average in a few days and then gaining back almost 85 points from Friday’s low to mid-afternoon Tuesday at the highs was a roller coaster ride for the ages. But what was most interesting perhaps was how correlated markets reacted. With markets seemingly responding to a host of stimuli, from trade wars to the withdrawal of quantitative stimulus, Bank of America Merrill Lynch offers a strategy on “how to play a dot plot surprise to the upside.” What they got after releasing the March 20 report was a surprise, that’s for sure, as volatility exploded. But what appears to be playing out now is a questioning of market message validity as the S&P 500, after substantial gains Tuesday morning, mean reverted to go contrary, down over 30 points in the S&P 500, with less than an hour left in the trading day.

It was after the release of Federal Open Market Committee minutes when newly minted Fed Chair Jay Powell held his first press conference, which equity markets started to see a decline. In the early afternoon, with the S&P 500 near 2727, talk of raising interest rates began to permeate the air as Powell said: “the economic outlook has strengthened in recent months.”

The Fed hiked rates by a quarter point, moving from a minuscule 1.5% to an equally tiny 1.75%, the sixth such interest rate hike since the Fed began pulling rates off the floor near zero in December 2015.

The FOMC’s inflation target changed little while their projections for employment moved lower as the central bank expressed confidence in the Phillips Curve, which pins a correlation to low unemployment and inflation.

Market participants took the aggressive talk as a signal, as bears are worried that engineering both a reduction in the balance sheet and raising interest rates simultaneously is akin to walking a tightrope made of thin test fishing line.

BAML thinks the risk to the Fed’s dot plot is to the upside.

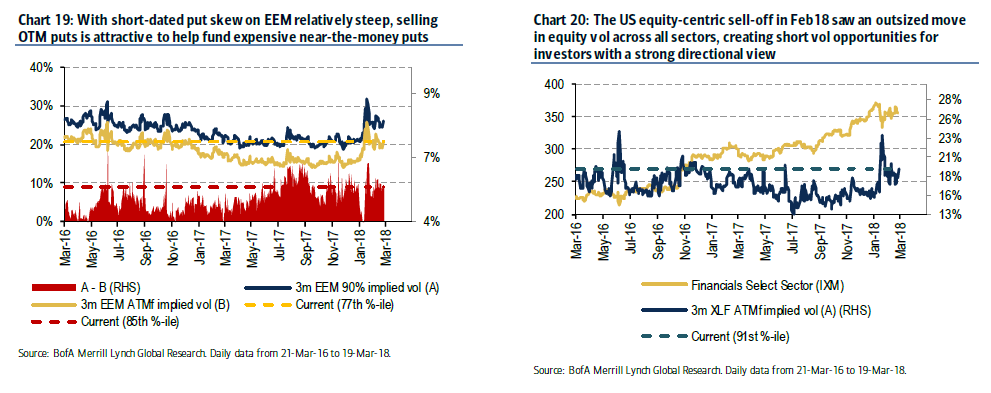

“Higher real rates and higher USD will not be kind to risky assets like emerging markets,” they wrote, pointing to potential benefits to financials as rates rise.

To hedge the risk of higher rates/USD on emerging markets, BAML favors “levering relatively steep skew” to sell out of the money puts that would “help fund near-the-money puts,” the report said. “To position for upside in Financials, we like taking a short vega-bias and favor monetizing short-dated implied vol near 2yr highs via long call spread collars (long ATM calls, short OTM calls/puts).”

Trading volatility is often a two-sided affair. There is preparing for the volatility spike and then the receding volatility that follows. While short volatility trading has become an anathema in 2018, among professional traders volatility selling is an acceptable risk – when the pricing moves out of line, and the term structure inverts with a reasonable expectation for mean reversion.

The February spike in volatility, a US-centric sell-off, created short volatility opportunity “for investors with a strong directional view.” When volatility spikes, the best way to buy the dip might be low vol.

But oddly, on the most recent dip, that didn’t appear to be the case.

As stocks sold off 140 points last week, the VIX spiked from 16.43 on the morning of the 21st to 25.65 on Friday. But on Monday, as stocks were experiencing one of their most significant gains in history – the best day since 2015 – the rally took place on low volume. The VIX, for its part, was only able to move just below 21 – not anywhere close to its starting point before the sell-off, violating its traditional correlation ratio with the S&P 500.

But it wasn’t just a notable lack of confirmation fundamentally linked markets that mattered, but in other correlated markets as well. Corporate bond markets, for instance, didn’t appear to be buying the stock market rally.

“We do think that the relief rally in the equity market is purely due to the heavy sell-off,” Naeem Aslam, the chief market analyst at TF Global Markets in London, was quoted as saying in a Bloomberg report. “It is more of a dead cat bounce than anything else; if the underlying fundamentals aren’t addressed, we could see the sell triggered again.”

Despite the all clear sign in the markets from Monday’s rally, correlated markets are telling a different story.