Longboard’s original research proves that over the long term, a small minority of stocks drive returns for the overall market.

Q3 hedge fund letters, conference, scoops etc

If you’ve heard of the Pareto Principle before, this might not surprise you.

What does this mean for investors? It may be more efficient to navigate this reality by getting defensive, and strategically avoiding the majority in this equation: the underperforming investments.

Be aware of disproportionate rewards

Here’s a closer look at our research on this competition gap in action in the U.S. stock market.

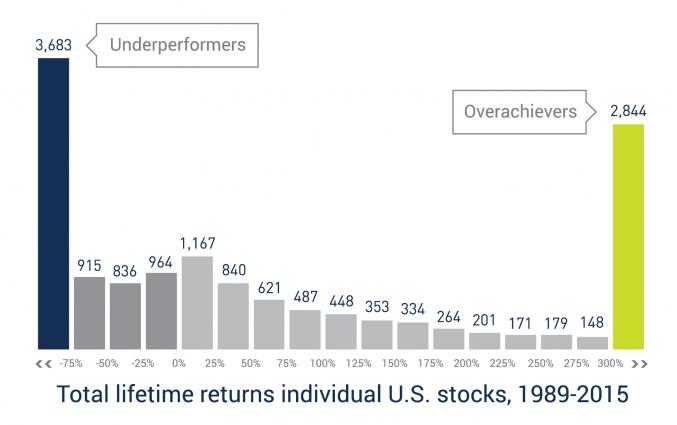

We analyzed 14,455 active stocks between 1989 and 2015, identifying the best performing stocks on both an annualized return and total return basis.

Looking at total returns of individual stocks, 1,120 stocks (7.7% of all active stocks) outperformed the S&P 500 Index by at least 500% during their lifetimes. Likewise, 976 stocks (6.8% of all active stocks) lagged the S&P 500 by at least 500%. The remaining 12,404 stocks performed above, at or below the same level as the S&P 500.

The principle of the competition gap remains true in practice: The minority accumulates a disproportionate amount of the total rewards, creating a “fat tail” distribution of extreme outperformers and underperformers with a large gap between the two.

What’s more, the left tail in the stock market’s competition gap (or distribution) is significant. 3,431 stocks (23.7% of all) dramatically underperformed the S&P 500 by 200% or more during their lifetimes.

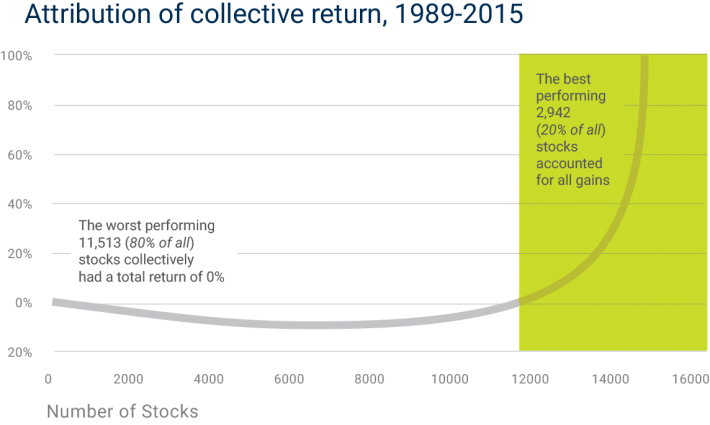

So, let’s say an investor’s portfolio missed the 20% most profitable stocks between 1989 and 2015. Instead, he invested in only the other 80%. His total gain would have been 0%.

So, let’s say an investor’s portfolio missed the 20% most profitable stocks between 1989 and 2015. Instead, he invested in only the other 80%. His total gain would have been 0%.

Once again, the principle holds true: Over the long term, the more efficient approach is to strategically avoid the many underperformers.

Seek alternative long-term returns

To get more benefits from alternative allocations, investors can seek long-term trend following strategies that proactively trim investments that don’t perform over time. These more defensive strategies are better positioned to avoid sustained downtrends — and a diversified portfolio with fewer strategies trapped in sustained downtrends can recover more quickly.

What’s more, some of the same strategies that can deliver this downside protection can add further diversification, potentially delivering results that are uncorrelated to the market and to other alternatives.

Disclosure

The information set forth herein has been obtained or derived from sources believed by Longboard Asset Management to be reliable. However, Longboard does not make any representation or warranty, express or implied, as to the information’s accuracy or completeness, nor does Longboard recommend that the attached information serve as the basis of any investment decision. This document is approved for public use. This document has been provided to you for information purposes and does not constitute an offer or solicitation of an offer, or any advice or recommendation, to purchase any securities or other financial instruments, and may not be construed as such.

Longboard hereby disclaims any duty to provide any updates or changes to the analysis contained in this spreadsheet. Market analysis, returns, estimates and similar information, including statements of opinion/belief contained herein are subject to a number of assumptions and inherent uncertainties. There can be no assurance that targets, projects or estimates of future performance will be realized.

There is a risk of substantial loss associated with trading commodities, futures, options, derivatives and other financial instruments. Before trading, investors should carefully consider their financial position and risk tolerance to determine if the proposed trading style is appropriate. Investors should realize that when trading futures, commodities, options, derivatives and other financial instruments could lose the full balance of their account. It is also possible to lose more than the initial deposit when trading derivatives or using leverage. All funds committed to such a trading strategy should be purely risk capital.

Index performance in this document was sourced from third-party sources deemed to be accurate, but is not guaranteed. All index performance is gross of fees and would be lower if presented net of fees. Indices referenced are not representative of the entire futures or trading universe. Investors cannot invest directly in the indices referenced in this document.

Diversification does not eliminate the risk of experiencing investment losses. Past performance is not an indication of future performance.

Methodology

This research was originally published by Cole Wilcox and Eric Crittenden of Blackstar Funds in 2006. Since then, Blackstar Funds has become Longboard Asset Management, and the organization updated its research in 2016 to focus on data from 1989–2015.

Our database covers all common stocks traded on the NYSE, AMEX and NASDAQ since 1989, including delisted stocks. Stock and index returns were calculated on a total return basis (dividends reinvested). Dynamic point-in-time liquidity filters were used to limit our universe to the approximately 4,000 most liquid stocks each year, representing approximately 99% of the investable U.S. equity market. In total, 14,455 stocks were evaluated (due to index reconstitution, delisting, mergers, etc.).

Article by The Longboard Funds