This article is a guest post by Rich Howe, CFA, of Stock Spin-off Investing. This write up was originally published in November 2019 exclusively for subscribers of the Stock Spin-off Investing Newsletter. For the next week (offer expires 1/31), sign up with code VW to get 20% off an annual subscription. If you have any questions, email Rich at Rich@stockspinoffinvesting.com.

Q4 2019 hedge fund letters, conferences and more

Summary

In November 2019, Recro Pharma (REPH) spun off its money losing Acute Care Drug business, in a taxable transaction. This business has historically masked the strong fundamentals of REPH’s remaining CDMO business. The remaining CDMO business is defensive, on pace to grow revenue 34% in 2019, and generates a 39% EBITDA margin. Despite robust fundamentals, REPH trades at 8.3x 2020 EBITDA and 14.5x 2020 EPS, a massive discount to peers. The CDMO industry has been consolidating, driven by interest from strategic and financial sponsors. Recent acquisitions have closed at 16.5x EBITDA. The Chairman of REPH’s Board is the Managing Partner of Engine Capital, an activist hedge fund, focused on maximizing its portfolio returns. We believe a sale of REPH in 2020 is likely, but even if that doesn’t materialize, Recro Pharma is a high quality business that we would want to own for many years.

Investment Case

- The spin off of Acute Care Drug business allows the Contracted Manufacturing and Development Organization (CMDO) business to shine and gain greater investor interest.

In November 2019, REPH spun off its Acute Care Drug business (Baudax, Ticker: BXDX). For years. REPH has spent millions of dollars trying to get its acute care drug (IV Meloxicam) approved. This heavy spend has obscured the value of the company’s CDMO business. That is no longer the case. The remaining company is a pure play CDMO business.

- CMDO industry is an attractive, recession resistant business.

Revenue is sticky due to 5-6 year manufacturing contracts and high switching costs. Further, the secular trend of pharmaceutical companies outsourcing manufacturing in order to cut costs and to focus on their core competencies is driving continued growth for CDMO companies.

The industry is fragmented and M&A activity has been very strong, driven by strategic and financial sponsors.

- REPH’s CMDO business is exceeding expectations and is likely to continue to do so going forward. Consensus expectations are too low.

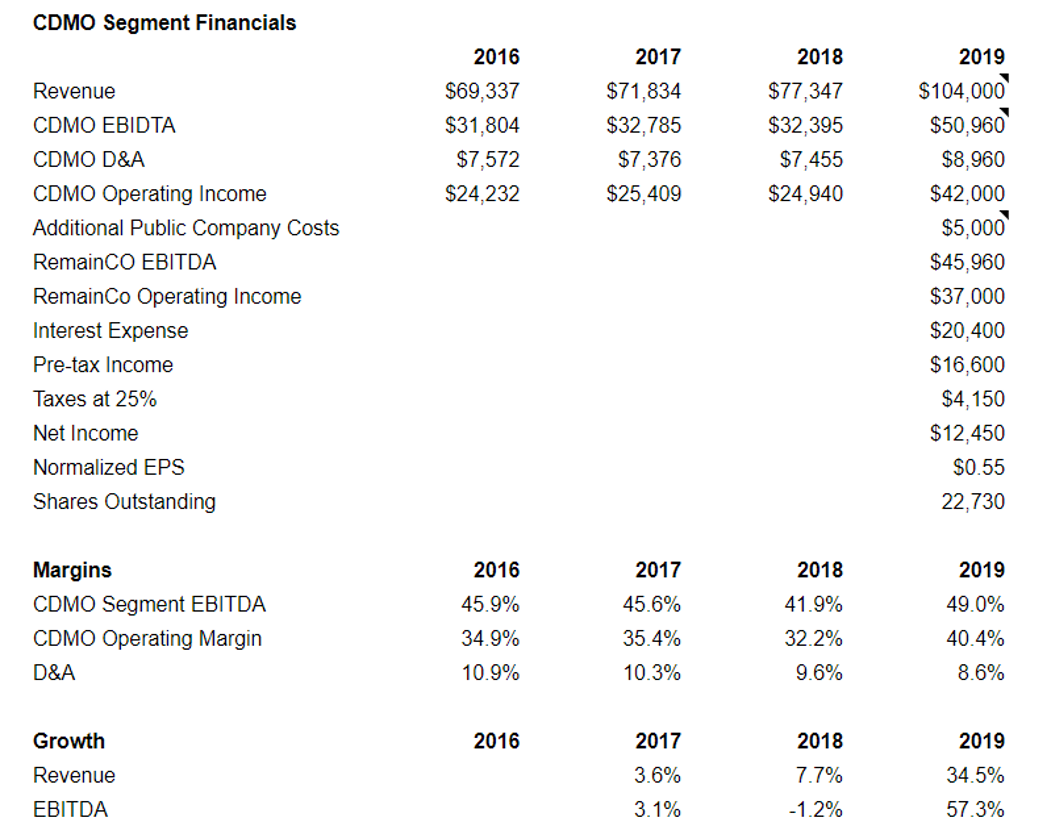

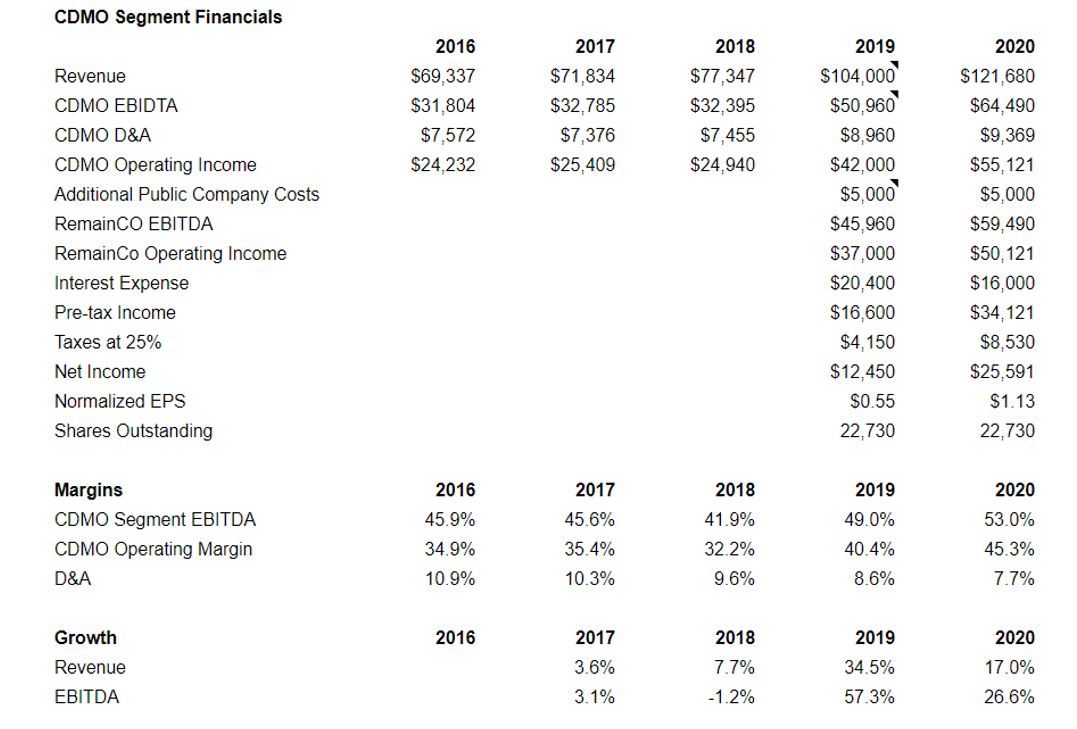

In 2019, revenue is on track to increase 35% while EBITDA is on track for 57% growth. In two consecutive quarters, management has beaten expectations and raised guidance. Despite this strong performance, 2020 revenue, EBITDA, and EPS estimates remain too low.

Using reasonable estimates (assumptions detailed below), We estimate REPH will generate revenue of $122MM (vs. consensus of $119MM), EBITDA of $59MM (vs. consensus of $43MM) and EPS of $0.94 (vs. consensus of $0.58).

Here is commentary from REPH’s CFO on the Q3 2019 conference call regarding the growth of the CDMO business.

“So we’re really excited about the anticipated revenue growth in the trajectory really of around 30% this year. And with the long range forecast that we have from our customers, the current market conditions, and the prospects of the new business growth, we expect to continue to see that growth in 2020 and beyond.”

We think part of the reason that estimates are so low is because the analysts who covered REPH mainly focus on biotech/pharma stocks, not healthcare services. In fact, several analysts dropped coverage of the REPH after the spin-off.

- Unique Spin-off Dynamics suggest the company may be sold in 2020.

Consolidation by health care and financial sponsors in the CDMO industry has been remarkable (see valuation section for additional analysis). 5 out of the 7 competitors that REPH lists in its 10-K have recently been acquired.

The spin-off of Baudax is a taxable transaction which means that there are no restrictions on a potential sale of Baudax or Recro Pharma.

Also, the current CEO/CFO will assume CEO/CFO responsibilities for both the CDMO business (Remainco) and the spin-off (Baudax). However, the current CEO (Gerri Henwood) is more interested in drug development and commercialization and has indicated that her involvement with the CDMO business will be limited to 12 months. In our mind, this also suggests a company sale could happen sooner rather than later.

Finally, in March 2019, Arnaud Ajdler, Managing Partner at Engine Capital, an activist hedge fund, was named Chairman of the Board. Engine Capital owns ~5% of REPH/BXDX. We are quite sure that Engine Capital is well aware of M&A activity in the CDMO space and will explore strategic alternatives in an effort to maximize its return

- Valuation is compelling on an absolute and relative basis.

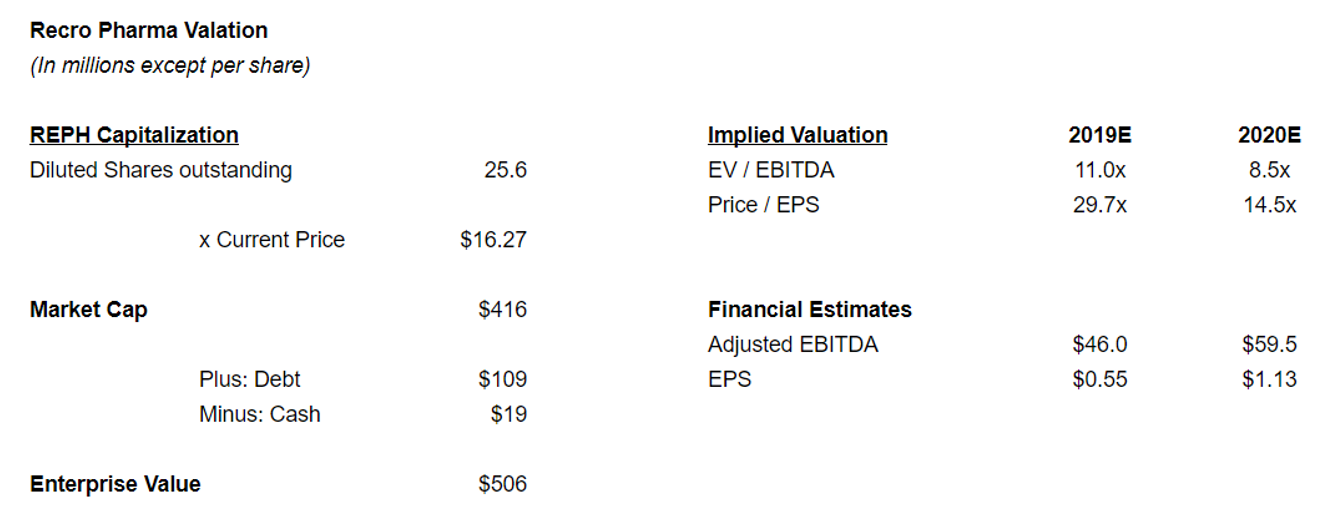

REPH trades at 8.3x our 2020 EBITDA estimate and 14.5x our 2020 EPS estimate. This is compelling for a company in an attractive, defensive industry with strong growth and 50% EBITDA margins.

Further, publicly traded CDMO companies trade at 15.3x forward EBITDA.

Finally, there has been tremendous interest from strategic and financial sponsors. Recently, CDMO companies have been acquired at 16.5x EBITDA.

Background

On Friday, November 21, 2019, Recro Pharma (REPH) spun off its Acute Care Drug business. The business is called Baudax Bio and trades under the ticker BXRX.

The company is a clinical-stage biopharmaceutical company focused on developing and commercializing innovative products for hospitals and related acute care settings. Currently, the Company’s largest bet is on its IV Meloxicam drug. This drug is an intravenously injected pain-reliever that possesses anti-inflammatory, analgesic, and antipyretic activities, which are believed to be related to the inhibition of cyclooxygenase (COX) and subsequent reduction in prostaglandin biosynthesis. The oral form of this drug is already in use, called Mobic and marketed by Boehringer Ingelheim Pharmaceuticals. However, the oral form of the drug takes 5-6 hours to begin to treat the symptoms, while the IV version would begin to work much quicker.

Baudax’s initial application for IV Meloxicam was rejected, but the company appealed the FDA’s decision, and the FDA approved the appeal. The FDA is in the process of reviewing the drug’s application and deciding what label the drug should have (which markets its approved for).

The spin-off was capitalized with $19MM which will provide financial runway for one year of operations. Management expects that the drug will ultimately be fully approved and at that time, Baudax will raise additional equity capital or partner with a larger pharma company to launch the drug. A denial of the drug to be marketed and sold might be a death sentence for Baudax.

The spin-off is difficult to analyze. It could be a billion dollar company, but it also could be a zero. It’s hard to get an edge on the company.

However, the transaction is more interesting because of what it leaves behind.

The RemainCo

For years, the excessive costs to develop IV Meloxicam have masked Recro Pharma’s wonderful CDMO business.

Business Overview

CDMO stands for “Contract Development and Manufacturing Organization”.

As the name implies, CDMO companies serve other companies in the pharmaceutical industry on contract basis to provide drug development and drug manufacturing.

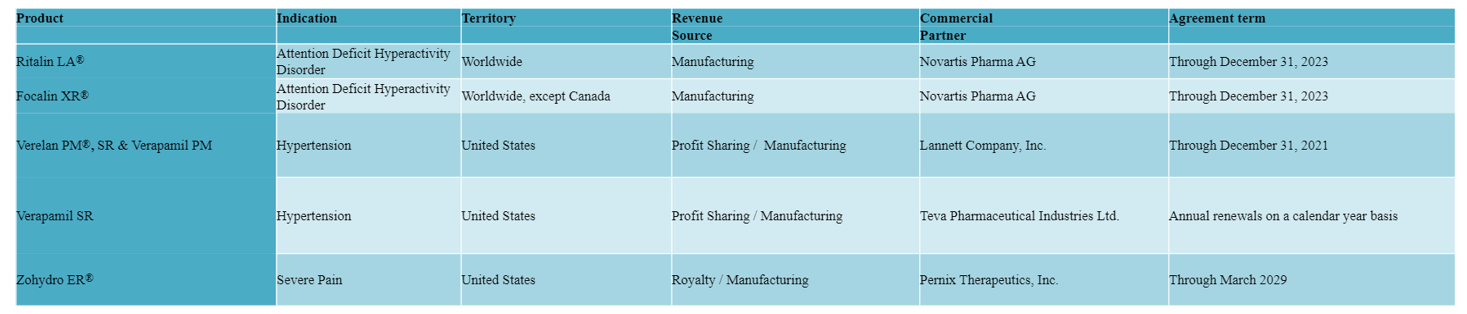

The below table details key products that REPH developed and/or manufactures for key commercial partners.

In addition to the key products listed above, the company also develops and manufactures other development stage products.

The company owns and operates a 97,000 square foot property in Gainesville, Georgia. It also leases a 24,000 square foot property which is also in Gainesville.

Remainco generates revenue by leveraging its formulation expertise to develop and manufacture pharmaceutical products using proprietary delivery technologies and know-how for partners who plan to develop and commercialize these products. These collaborations result in revenue streams including manufacturing, royalties, profit sharing, and research and development.

If you look at REPH’s latest 10-K, you can see that the CMDO business historically has not been a priority. 6 out of 7 strategic priorities relate to the Acute Care Drug Business.

However, that changed in Q2 2018 when the company hired Heather Sugrue to lead business development (BD) efforts. Previously, Heather spent five years leading the West Coast BD team at Patheon, another CDMO, which was acquired for 17x EBITDA in 2017. Increased focus on the CDMO business is paying off as revenue and EBITDA has accelerated dramatically in 2018 and 2019.

Growth is being driven by a couple of factors.

- BD effort is paying off as the company hopes to exit 2019 with new products representing 10% of revenue in 2019.

- REPH is benefitting from its customer (Teva) gaining share with REPH’s largest product (Verapamil SR). In 2018, this drug represented 48% of REPH’s revenue. Mylan was manufacturing a competitive product but closed its plant due to quality control issues. Teva has capitalized by locking-in customers to multi-year contracts.

- A customer has been raising pricing on a product that REPH manufactures. REPH benefits through a profit sharing agreement.

Here’s what CFO, Ryan Lake, said about the CDMO growth on the Q3 2019 conference call.

“Yeah. I mean through the first half of the year, we really saw our partners’ marketing and distribution strategies really being successful and our new business efforts continuing to increase. One of our customers had implemented a new pricing strategy, which benefits us directly as a result of our profit sharing relationship. And they also deepened their distribution strategy with what we believe was some stocking at one of the largest generic sources in the U.S.

We also saw capsule volumes to one of our customers in the first half of 2019 exceed all of their 2018 capsule volume. So we’re really excited about the anticipated revenue growth in the trajectory really of around 30% this year. And with the long range forecast that we have from our customers, the current market conditions, and the prospects of the new business growth, we expect this continue to see that growth in 2020 and beyond.

The business is really strong. It is doing great. You saw earlier this year, we are able to walk into five and six year agreements with our major core commercial customers. We’re also able to expand economically one of our agreements with another customer, because these are very important relationships with them, very sticky and I have to say that our new business development team, and the team down in Gainesville is doing a tremendous job.

The culture and the atmosphere of every one really pulling together to achieve the new direction and diversify our historic revenue streams, toward these new business where we’re seeing a lot of progress there. So it’s really an exciting time for Recro, Esther.”

Based on the recent results and comments from management, the outlook is very strong for this business.

Over the past year, the CDMO business has beaten expectations and raised guidance.

Original guidance for the CDMO business in 2019 was revenue of $85MM to $87MM and EBITDA of $38MM to $40MM.

When REPH reported second quarter results, it increased revenue guidance to $91MM to $94MM and EBITDA guidance to $44MM to $46MM.

When REPH reported third quarter results, it increased revenue guidance to $98MM to $100MM and EBITDA guidance to $48MM to $50MM.

To us, this guidance still feels conservative and we’re expecting the division to generate annual revenue of $104MM and EBITDA of $51MM.

Factoring our estimate of $5MM of additional public company costs (guidance from company). Adjusted 2019 EBITDA should be $41MM.

In 2020, we expect strong growth to continue based on recent performance and the CFO’s comments.

As such, we’re expecting 17% revenue growth in 2020 and segment EBITDA margins expanding from 49% to 53%. The CDMO business is using less than half of its capacity at its main plant and has additional capacity at its other plant. As such, margins should continue to expand as revenue ramps up.

**We have assumed REPH pays taxes (25% tax rate). However, the company has generated cumulative losses of $122.6MM since inception in 2007. These tax losses can most likely be used to offset income for the foreseeable future. Management has not publicly quantified its tax loss carry forwards.**

One final point to highlight is that Recro’s business is not economically cyclical. From our view, this is a significant positive given we are in the later innings of the current economic expansion.

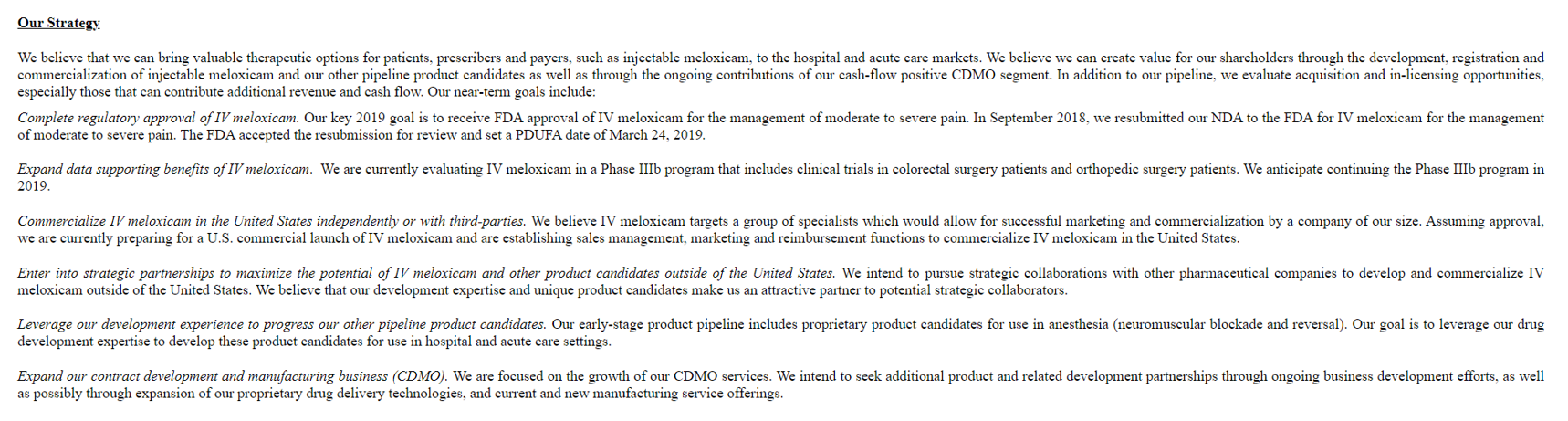

Company Strategy

In 2018, 48% of revenue came from Teva and 38% of revenue came from Novartis. These revenue sources are extremely stable as REPH recently signed long term agreements (5 year contract extension with Novartis and 6 year contract extension with Teva). Further, revenue is sticky. CDMO’s are written into drug applications so pharma companies must resubmit their application to the FDA if they want to switch manufacturers.

Besides the base business with Teva and Novartis, REPH recently increased its focus on growing its CDMO business through business development efforts. The effort has paid off as the company expects to exit 2019 with ~10% of revenue coming from new business.

Business development entails reaching out to smaller pharma and biotech companies to win business providing services that help them formulate and ultimately manufacture drugs for clinical trials. The goal is that these relationships may start small, but will hopefully grow once new drugs are approved and manufacturing ramp up to meet demand.

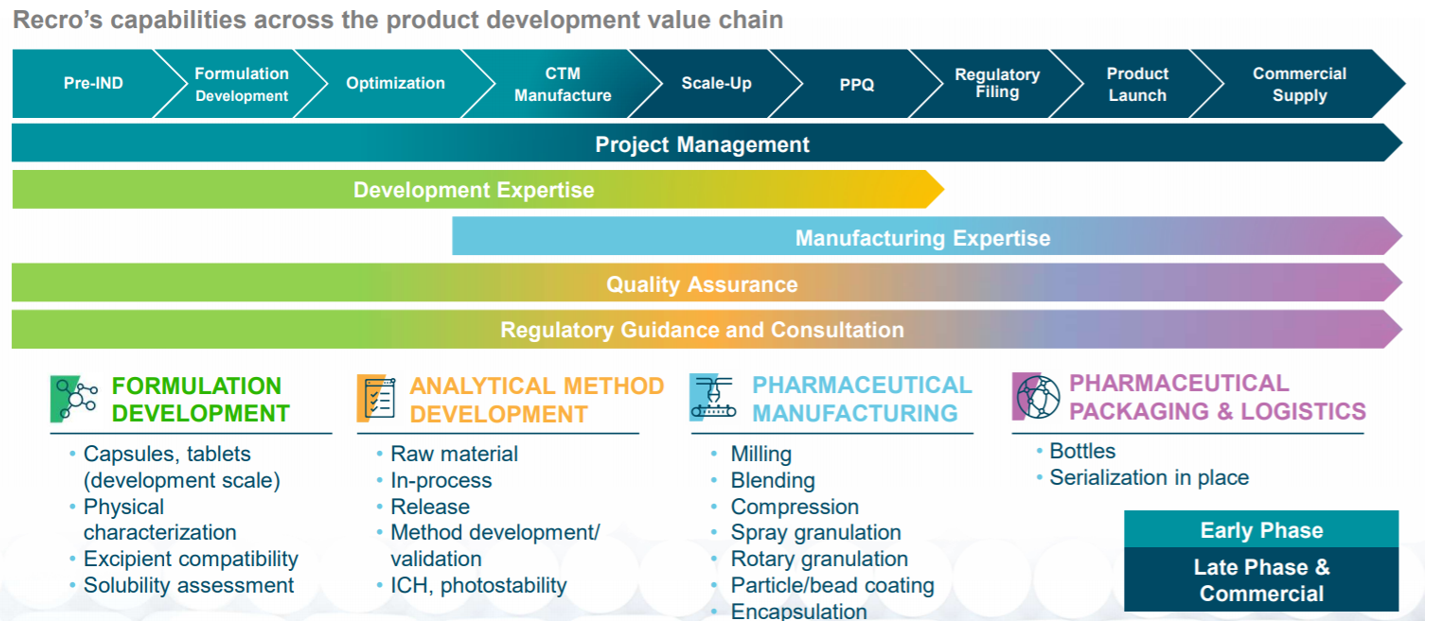

REPH provides a large number of services and capabilities (see slide below) related to formating, developing, and ultimately manufacturing to help small pharma companies progress through clinical trials to commercialization.

Industry

The CDMO industry is a great industry with a rosy outlook. This 2017 report from E&Y from 2017 is very good.

Key positives of the industry:

- Secular trend of pharma outsourcing manufacturing

a) From the EY report: “In the past, pharmaceutical companies often installed dedicated manufacturing capacities for innovative drugs in development, only to see them fail during phase III of clinical research trials. Thus, the additional manufacturing capacity for the specific drugs was no longer needed. To reduce the risk of expensive overcapacities, the demand for outsourced manufacturing has been rising continually. Constituting a US$62b market in 2016, the CDMO industry’s annual growth rate of 6% to 7% is slightly outpacing the growth of the pharmaceutical sector as a whole (5% to 6% compound annual growth rate (CAGR)), reflecting the ongoing shift toward increased outsourcing”

b) “At a time when pharmaceutical companies face increasing price pressures around the globe from key players, including public and government insurance systems, reducing operational expenses is a major driver of outsourcing pharmaceutical manufacturing to CDMOs.”

c) “Also, an increasing number of pharmaceutical companies are refocusing on their core capabilities and strengths, leading to divestments of in-house manufacturing capacities in some areas and to a growing reliance on CDMOs in other areas.” - Sticky revenue streams

a) CDMOs typically have 5-6 year contracts with pharma companies. - High switching costs

a) It is costly and time intensive to switch CDMOs once a manufacturing process has been established. - High margins

a) Due to points 2 and 3, CDMO’s generate high margins. - Industry consolidation

a) The industry is very fragmented and there has been significant M&A activity both by healthcare companies but also by private equity.

Competition

REPH has many competitors as the industry is very fragmented, but high switching costs and long term contracts limit the intensity of that competition.

REPH lists the following CDMO competitors in its 10K.

- Alcami Corporation

- Acquired by Madison Dearborn Partners for an undisclosed price in Q3 2018.

- Cambrex Corporation

- Acquired by Permira Funds for 4.3x revenue and 15.5x EBITDA in Q4 2019.

- Catalent, Inc.,

- Publicly traded. Trades at 3.9x revenue and 15.5x forward EBITDA.

- Mikart

- Acquired by Nautic Partners in 2018 for undisclosed price in Q3 2018.

- Mylan N.V.

- Not a great comp as primarily a generic pharma company not a CDMO.

- Patheon

- Acquired by Thermo Fisher in 2017 for 3.7x revenue and 20.5x EBITDA in Q3 2017.

- Quotient Sciences

- Acquired by Permira Partners in Q3 2019 for an undisclosed price. Including Permira, the last three owners of this business have all been private equity.

Customers

REPH is dependent on a small number of commercial partners, with its four largest customers (Novartis Pharma AG, Teva Pharmaceutical Industries, Inc., Pernix Therapeutics, Inc., and Lannett Company, Inc.) having generated 99% of the company’s revenues in 2018. Teva Pharmaceutical Industries, Inc. generated 48% of revenue under one customer agreement, and Novartis Pharma AG, generated 38% of revenue combined under two separate customer agreements.

REPH manufactures Verapamil/Verelan (high blood pressure drug) which is marketed by Teva and Lannett. REPH recently announced a six-year contract extension through 2024.

REPH manufactures Ritalin LA, a once daily ADHD treatment, and Focalin XR, an extended release ADHD treatment marketed by Novartis. REPH recently announced a 5-year contract extension through 2023.

REPH manufactures Zohydro ER (extended release hydrocodone) marketed by Currax (previously Pernix).

Quality of Business

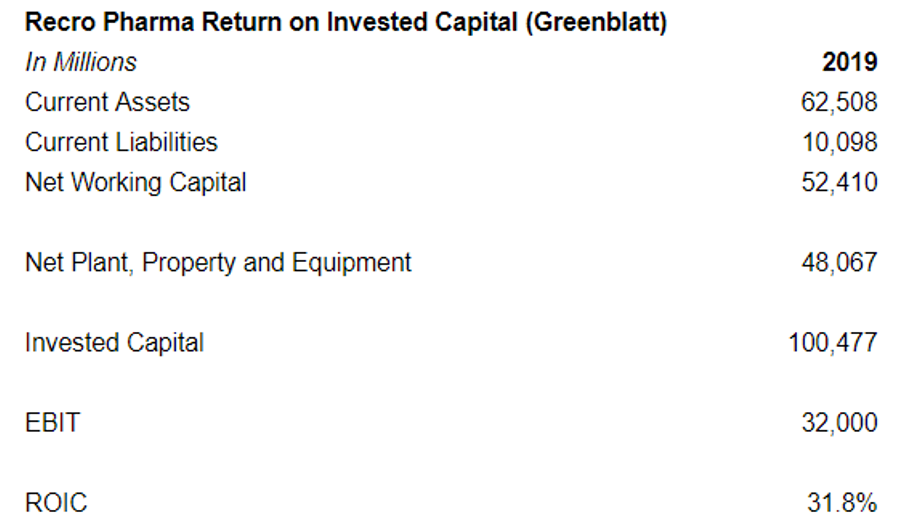

The quality of Recro Pharma’s business (CDMO business) is excellent as capital intensity is low, barriers to entry are high, and the business generates high margins. In 2019, Recro Pharma (CDMO business) is on track to generate a return on invested capital of 31.8% (Greenblatt method) as shown below. Importantly, Recro’s main manufacturing plant is operating at ⅔ capacity with one shift. Management has indicated that it could add two additional per shifts if needed to meet demand. Thus, Recro could more than double revenue with limited capital investment.

Capital Structure

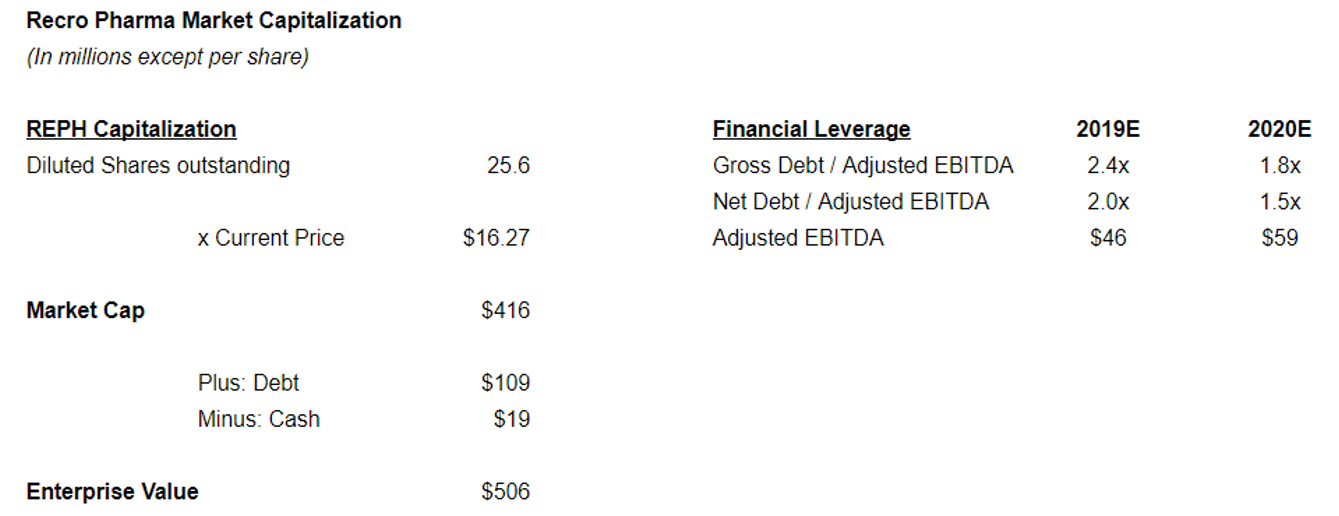

Using diluted shares outstanding, REPH has an enterprise value of $506MM.

REPH has net debt of $90MM and a net debt to adjusted 2019 EBITDA multiple of 2.0x.

Valuation

Recro Pharma looks attractive on both a relative and absolute basis.

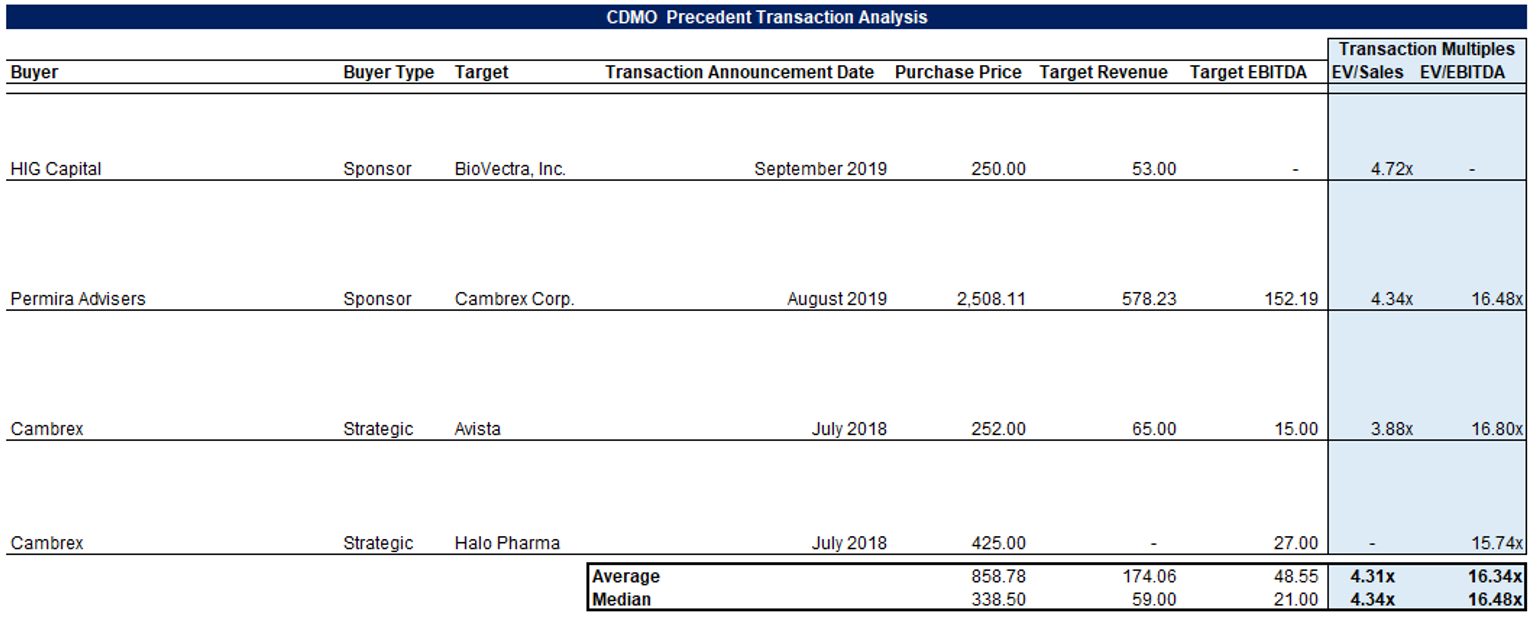

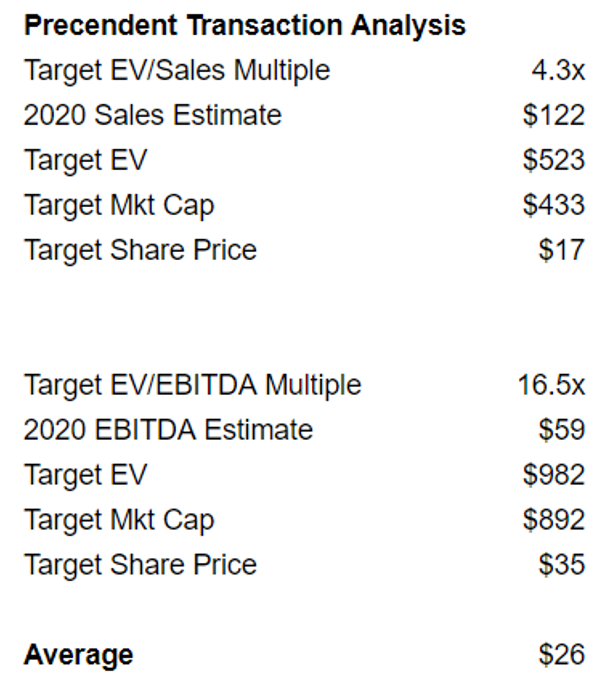

Precedent Transactions

As shown below, there has been significant M&A activity in the CDMO space recently.

On a median basis, CDMOs have been acquired recently for an EV/EBITDA multiple of 16.5x and an EV/Sales multiple of 4.3x.

If REPH were to be acquired at similar multiples, the stock would be worth $26 per share.

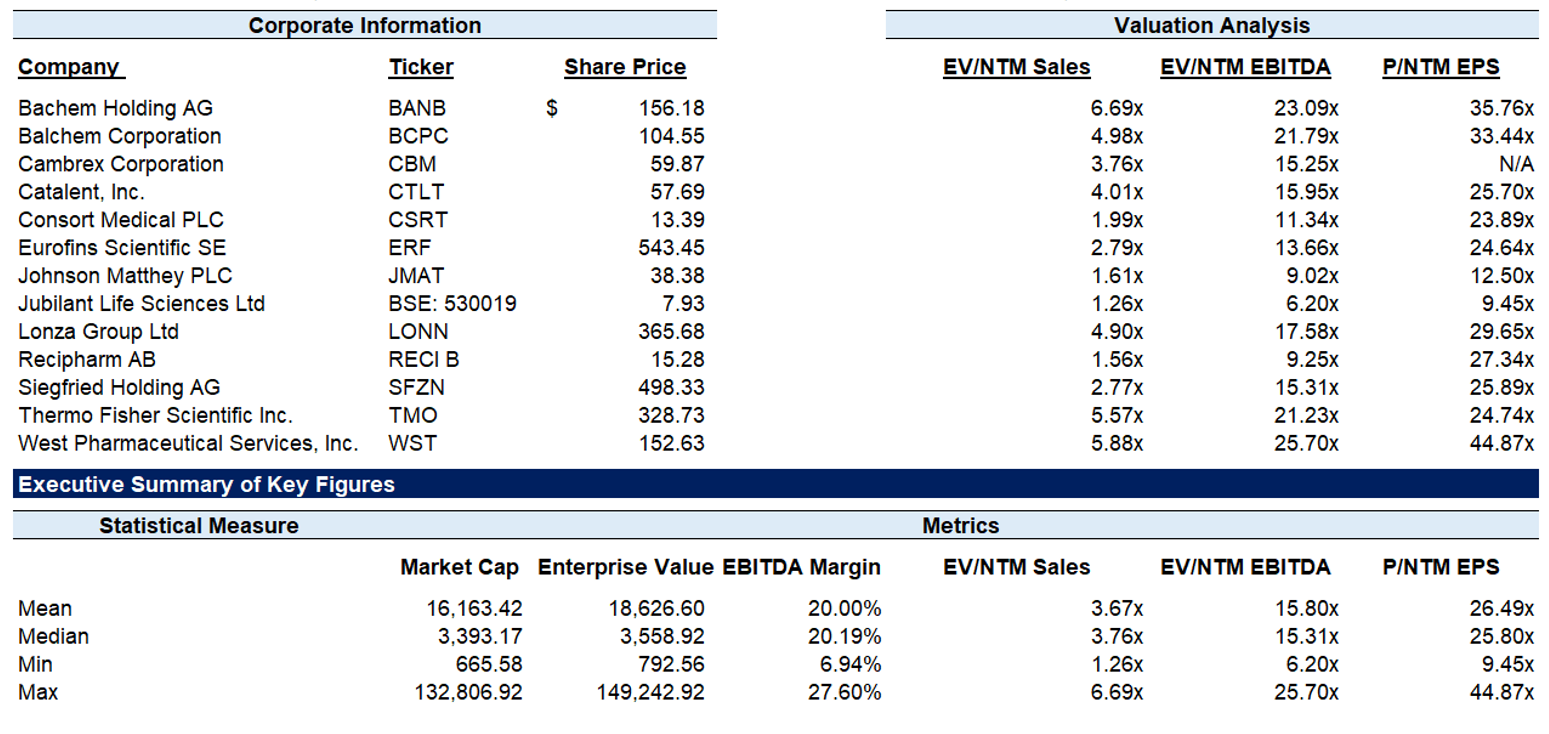

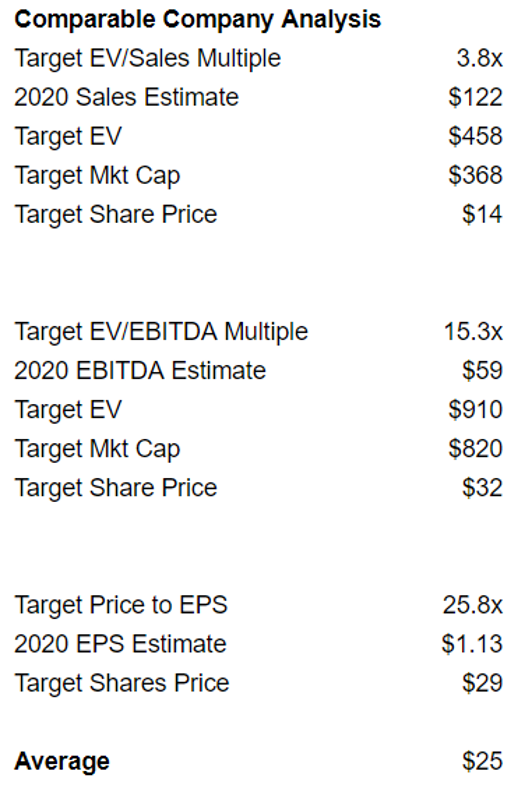

Public Comps

CDMO public comparable companies trade at 3.8x forward sales, 15.3x forward EBITDA, and 25.8x forward EPS.

If REPH were to trade at a similar valuation, it would trade at $25.

Assigning a 50% probability to comparable company analysis ($25 target) and 50% probability to precedent transaction analysis ($26), we arrive at our $25.50 price target.

Conclusion

REPH is an unusually attractive investment as it trades at a low valuation despite:

- Strong expected growth of revenue and earnings

- Secular tailwinds in the CDMO industry

- The potential to be acquired

Our price target of $25.50 implies 55% upside.

Want Other Special Situation Ideas?

For the next week (offer expires 1/24), sign up with code “VW”to get 20% off an annual subscription to the Stock Spin-off Investing Newsletter. If you have any questions, email Rich at Rich@stockspinoffinvesting.com.

Disclosure

Rich Howe, owner of Stock Spin-off Investing (“SSOI”), is long REPH. All expressions of opinion are subject to change without notice. This article is provided for informational purposes. Please do your own due diligence and consult with an investment adviser before buying or selling any stock mentioned on www.stockspinoffinvesting.com.