A new report out this week from the Deloitte Center for Financial Services forecasts that private equity could be poised for “formidable” growth over the next five years, with assets under management possibly increasing 28% to $5.8 trillion by the end of 2025. That’s the base forecast, which the report’s authors mark as having a 55% likelihood of occurring. Meanwhile, the bear case scenario has AUM growing to $5.3 trillion (from the $4.5 trillion set at the end of 2019) and the bull case is that the industry hits $6 trillion in 2025. You can see the three scenarios unfold, stacked side by side, here.

Q3 2020 hedge fund letters, conferences and more

Whatever scenario is correct, each forecast reveals the opportunities private equity funds have to grow AUM. As the report notes, “firms that exceed the expectations of three key stakeholders—their employees, portfolio companies, and limited partners—will likely benefit the most … How PE firms managed the crisis will likely influence their returns for years to come. The pandemic may turn out to be a pivotal point in the history of PE firms, widening the gap between winners and losers.”

This paper also explores how firms can deliver on that, supported by insights from a survey of 200 portfolio companies. From the findings:

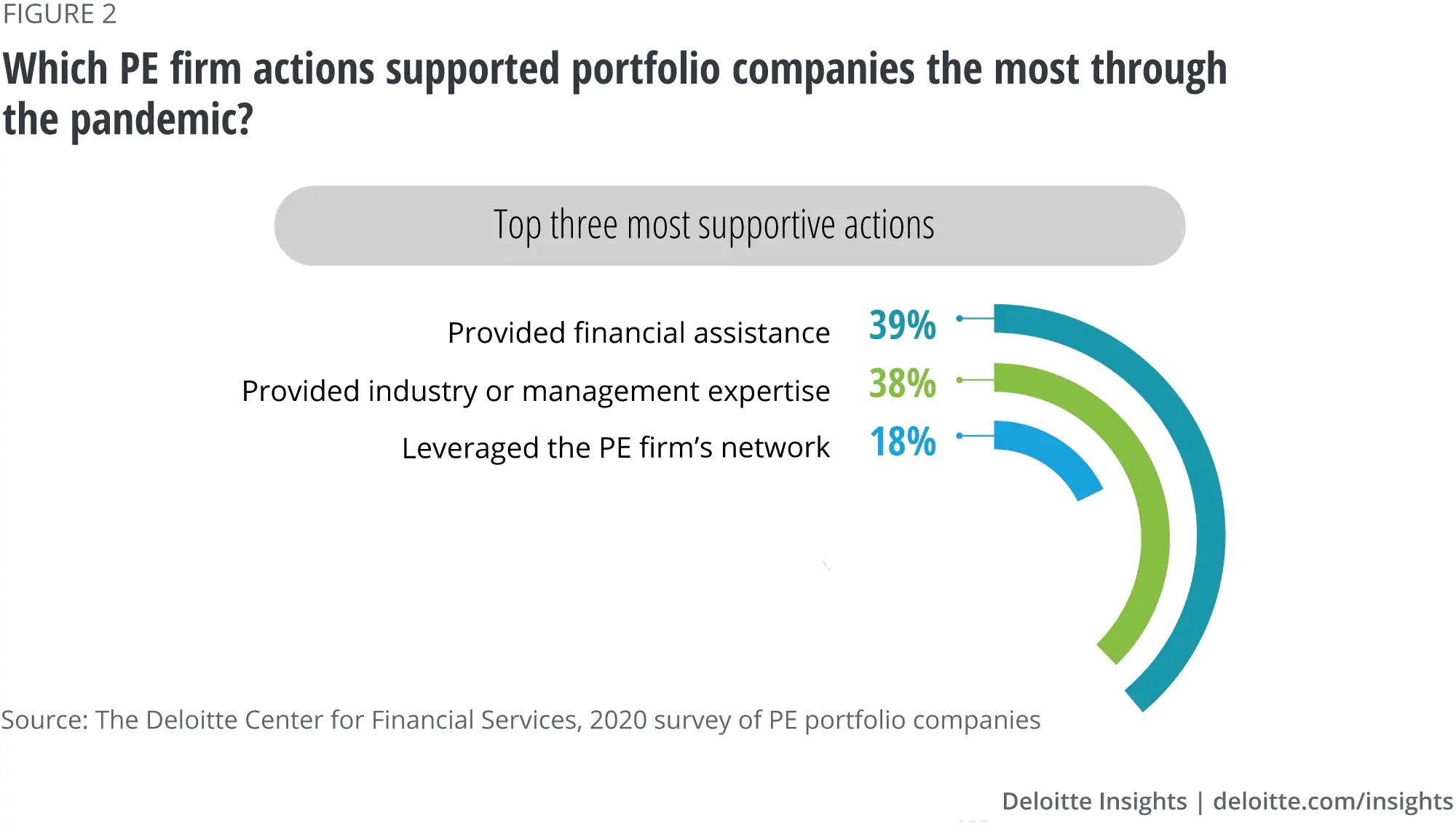

- 47% of respondents in Deloitte’s survey either received or expected fresh investments from their PE investor during the pandemic. Another 15% received assistance with debt refinancing.

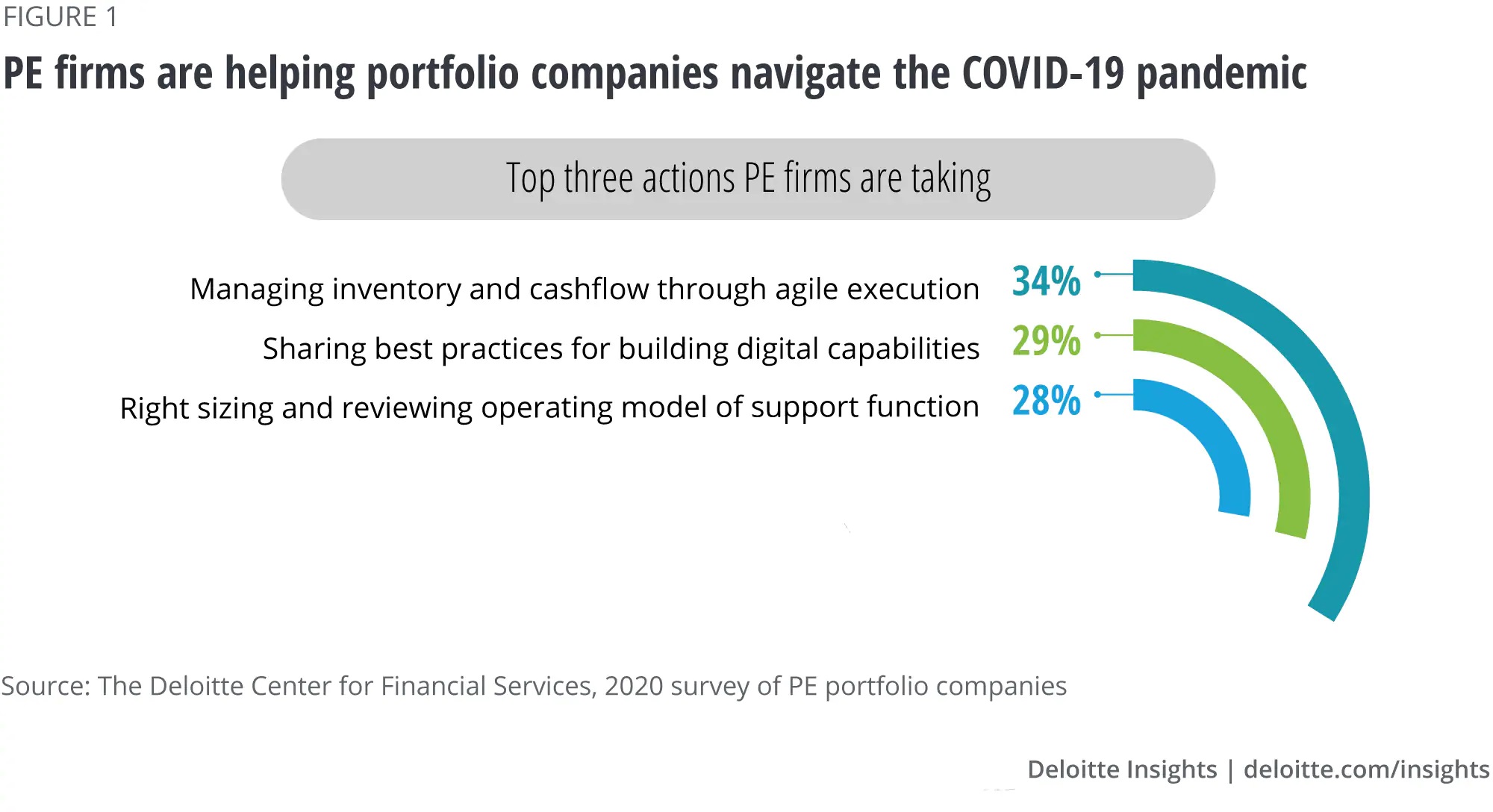

- Private equity firms also helped portfolio companies manage their supply chains, build digital capabilities, maintain business continuity and secure financing. According to the survey, the most common action included helping companies manage inventory and cash flow by reviewing bottlenecks, monitoring cash balances daily and revisiting payment terms.

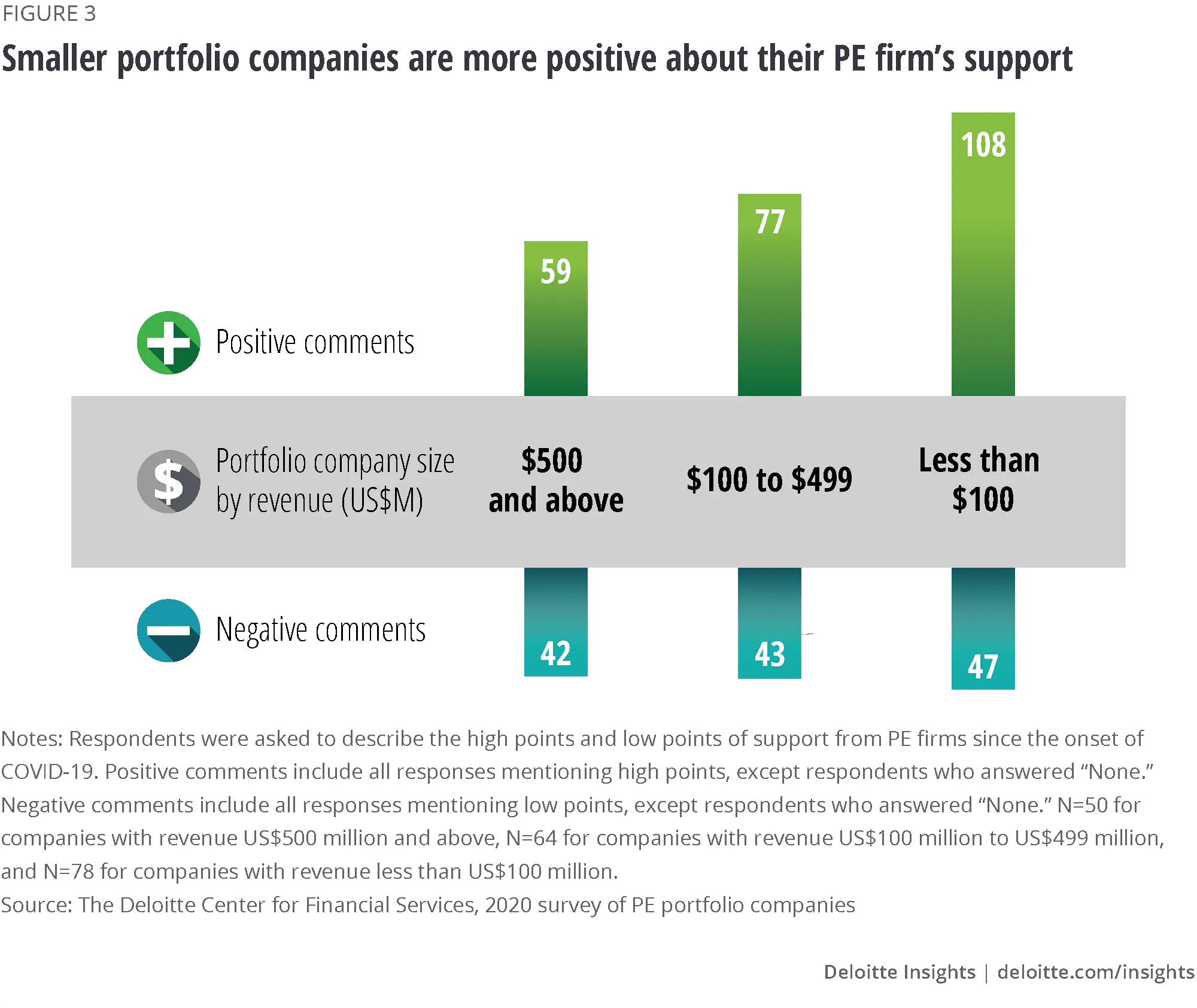

- Unsurprisingly, not all portfolio company leaders appreciated the actions their private equity investors are taking to support their companies through the pandemic. Some portfolio companies—mostly from companies expecting a decline in revenues—expressed concerns. The #1 area cited on this front was around financial controls, such as those placed on investments and expenses as well as a lack of capital infusion. It was followed by tighter talent policies, such as headcount reduction and reduced compensation, while excessive operational scrutiny ranked third.

- Satisfaction levels of surveyed portfolio companies varied with size. Companies with less than US$100 million in revenues spoke most favorably, while those with more than US$500 million in revenues seemed the least satisfied.

The report is online here.