Muddy Waters is short Manulife Financial Corp. (“MFC”). MFC’s life insurance subsidiary, The Manufacturers Life Insurance Company (“Manulife”), just concluded a trial that could significantly damage its earnings, capital, creditworthiness, business, and solvency – per its own expert’s sworn affidavit. We believe a verdict is likely by the end of this year. There are therefore material risks to the financial wellbeing of MFC. We do not believe investors are aware of these risks, nor do we believe they have been priced into MFC shares.

[activistinvseting]

Q3 hedge fund letters, conference, scoops etc

Manulife: An Insurance Company on Trial for its Life

Introduction

We all have things from the 90s we’d take back if we could. For some, it was wearing Zubaz (see below); for others, it was paying to see Ace of Base in concert. Right now, some senior Canadian insurance executives are ruing a particular type of insurance contract from that era.

Muddy Waters is short Manulife Financial Corp. (“MFC”). MFC’s life insurance subsidiary, The Manufacturers Life Insurance Company (“Manulife”), just concluded a trial that could significantly damage its earnings, capital, creditworthiness, business, and solvency – per its own expert’s sworn affidavit. We believe a verdict is likely by the end of this year. There are therefore material risks to the financial wellbeing of MFC. We do not believe investors are aware of these risks, nor do we believe they have been priced into MFC shares.

At issue is one of Manulife’s insurance contracts, which was purchased by a hedge fund called Mosten Investment LP.1 Should Mosten prevail, it could lead to billions of dollars of losses at Manulife, which could greatly impair its future earnings and affect its capital adequacy ratios. The trial judge is expected to render his decision by the end of 2018. The crux of the litigation is not about a particular claim. Rather, the issue is whether Mosten (or other owners of similar policies) can force Manulife to provide it with what would likely be one of the highest yielding short-term investment grade products in the developed world.

Per Manulife’s own expert witness, Manulife is effectively on trial for its life.

Mosten owns a specific insurance contract from 1997, the Architect IIe universal life insurance policy. Mosten argues it can deposit an unlimited amount of money with Manulife and receive an annualized guaranteed return of at least 4.00% (and possibly a good deal higher) with one-month liquidity according to its reading of the contract. If Mosten prevails, it could sell an unlimited amount of limited partnership interests backed by the Manulife insurance contract, and likely become the most lucrative money market fund in the developed world!2

These terms alone could financially cripple Manulife, which would take losses (a) on a cash basis, quarter after quarter, on the negative carry: i.e., the difference between the amount paid to Mosten and Manulife’s own rate of return, and (b) immediately on an accrual basis, since upon each inflow, Manulife would need to record a loss equal to the present value of the projected negative carry plus other administrative expenses

(e.g., trading costs and credit-related losses). The accrual of these losses will affect capital ratios. Assuming a CAD 1M LIBOR of 1.052% would mean a negative 2.948% spread on potentially billions!3 Based on examples presented by Manulife’s own expert witness (see Quantifying the Damage (in the words of Manulife’s own expert witness) below), we believe these losses could reach the billions if Mosten receives billions of inflows.4

However, it could get even worse for Manulife. Mosten argues that it is entitled to receive an 0.85% bonus each year on the policy anniversary. Based on an aggressive reading of the Mosten’s reading of the contract, a) Mosten may deposit this money the day before the policy anniversary, b) withdraw the money 30 days after the anniversary, and c) there is no limit on how much money Mosten may deposit for the bonus. Moreover, we believe Mosten has multiple such insurance contracts, meaning that if it prevails, it could slosh money among these policies in order to collect multiple 0.85% bonuses in the same year.

What does this mean for Manulife? If Mosten wins outright at trial and raises institutional money, this could negatively impact earnings, affect Manulife’s capital adequacy ratio and potentially threaten Manulife’s current and future life insurance business, as customers question Manulife’s financial strength. If Manulife’s capital adequacy ratio fell to a low enough level, the Canadian insurance regulator could prevent Manulife from paying dividends to MFC, which in turn would affect MFC’s ability to pay dividends to its shareholders.

Warren Buffett has said, “There are a lot of ways to lose money in insurance, and the industry is resourceful in creating new ones” (emphasis added) and “The unpredictability of our legal system makes it impossible for even the most conscientious insurer to come close to judging the eventual cost of long-tail claims.”

Based on our review of the affidavits, briefs of law, and discussions with Canadian counsel, Muddy Waters believes Manulife has found one of those ways to lose money, and it is impossible for anyone to predict the billions of Canadian dollars that Manulife could lose if Mosten is victorious. We believe that if Mosten wins and raises billions for its fund, Manulife’s annual losses from this contract could also number in the billions. The market appears to be unaware of this risk, and therefore, has not priced it in.

Summary

The Manulife Trial is about the Architect IIe universal life insurance policy issued by Aetna Life Insurance Company of Canada (“Aetna Canada”), which MFC acquired in 2004.5 Aetna Canada sold one of these universal life insurance policies to a Canadian doctor in 1997. The Canadian doctor held onto the policy until 2010, when Mosten bought the policy from the doctor, knowing full well the potential for “investment” in a low interest rate environment. That’s where our story begins, and only a court ruling or a settlement will tell us where it ends.

Mosten is the plaintiff and is seeking a declaratory judgment that its interpretation of its rights under the contract is correct, and therefore Manulife is bound to allow unlimited inflows from Mosten. If Mosten prevails, Mosten (and other owners of identical policies) will have the ability to deposit unlimited amounts of capital with Manulife and earn at least 4.00% per annum (and possibly a good deal higher). In other words, Manulife’s potential losses would be unlimited, particularly if it continues to be unable to invest Mosten’s money at the rate it is paying. The amount that Mosten may deposit would not be capped at $100 million, $1 billion, or even $100 billion. Moreover, if Mosten is successful in another of its claims, it could take advantage of an additional 0.85% policy anniversary bonus multiple times per year. In theory, Mosten could acquire several contracts with identical terms, except for different policy anniversaries. That would allow Mosten to potentially recycle its capital over and over again to receive the 0.85% multiple times a year. If Mosten wins, it could bleed Manulife into multiple credit downgrades or even insolvency (albeit unlikely, since Mosten’s investors would not benefit if this occurred), assuming a persistently low interest rate environment. Additionally, even without a credit downgrade, a Mosten victory followed by a large capital raise could severely impact Manulife’s capital adequacy ratio, and the Canadian insurance regulator has the power to limit Manulife’s ability to pay dividends to MFC, which could in turn impact MFC’s ability to pay dividends to its shareholders.

This would likely have a damaging spillover effect to Manulife’s insurance business. Potential life

insurance customers in their 30s who expect to live into their 80s would be taking credit risk if they buy a policy from Manulife. Another problematic scenario could be whole life insurance policyholders in their 50s. Due to the credit risk, they could be tempted to redeem their Manulife policies for cash value and buy policies from other insurers. In effect, if Mosten wins at trial, there could be a “run on a bank” in the form of a chain of redemptions in Manulife’s life insurance business. The speed of that exodus would depend on a number of factors, including the timing of appeals and press coverage. We believe the impact to Manulife’s life insurance business could be significant and severe.

Even if Manulife’s customer base is completely unaffected, but Mosten raises a large amount of capital to deploy into the Manulife contract, Manulife would be less cash-profitable: i.e., Manulife would realize immediate reportable losses equal to the difference between the 4.00% or higher rate of guaranteed return per annum and Manulife’s own, lower return on its investments, multiplied by the capital raised by Mosten.

Manulife’s capital adequacy ratios would also be significantly impacted, as Manulife will need to reserve capital against the net present value of its liabilities to Mosten. A favorable ruling on the 0.85% policy anniversary bonus would obviously exacerbate the problem. Therefore, Manulife would seemingly be at risk of credit rating downgrades. If Manulife were downgraded, more customers would likely leave, and the cycle would repeat.

In an absolute worst-case scenario, a Mosten trial victory becomes a death spiral for Manulife. If Mosten wins the trial, future customers might buy insurance elsewhere and existing customers might cash out their policies. If Manulife loses future customers or existing customers leave, profitability would suffer, and the capital base would shrink. At the same time, Manulife’s profitability would immediately shrink because of the negative spread between the guaranteed return paid to Mosten and the amount earned on its investments, while Manulife would also be required to hold more capital to offset the Mosten liabilities. If Manulife’s available capital shrinks as a result of the negative spread and capital requirements, and especially if Mosten raises a significant funds, Manulife might suffer a credit downgrade, barring equity injections from MFC. Equity raises would, of course, dilute MFC shareholders.

To summarize, in Muddy Waters’s view, an outright Mosten trial victory could severely impact Manulife’s profitability, wreak havoc on its capital adequacy ratios, cause MFC equity dilution, and potentially lead to credit downgrades. These events could have a significant impact on the debt, preferred and equity of Manulife’s holding company, Manulife Financial Corporation (MFC US and MFC CN).

Do Not Take Our Word for It; Listen to Manulife’s Own Expert

In a June 2017 affidavit filed by Manulife6, Leslie P. Rehbeli, an actuarial partner from Oliver Wyman, a well recognized management consultancy, said the following:

- “Life insurers with significant minimum interest rate guarantees [such as Manulife] would not be able to invest in sufficiently high yielding assets, in today’s interest rate environment, in order to honor these high interest commitments;

- Life insurers would therefore be required to establish significant additional provisions on their balance sheet, in respect of the additional deposits that would be expended to be made, to provide for the shortfall in investment income between what they earn on their invested assets and what they credit in the form of the minimum interest rate guarantees; [. . .]

- The increase in provisions that insurers would be required to establish would materially reduce the net worth of those life insurers, which in turn would reduce the financial strength of those companies relative to minimum regulatory capital requirements;

- This reduction in financial strength would eventually cause rating agencies to lower credit ratings of these life insurers, which in turn would trigger a reduction in confidence of investors, customers and agents of the life insurer. This could ultimately result in reductions in sales, increases in customers terminating their contracts, increase pressure on the liquidity of the company and reduce ability to raise capital;

- This cascading sequence of events ultimately has the potential to cause the insurer to become insolvent . . .”

Will Manulife lose at trial? We honestly don’t know, and it is extremely difficult to handicap a trial. However, based on our review of the affidavits, briefs of law, and discussions with Canadian counsel, Muddy Waters believes there is real potential for Mosten to prevail on at least some of its claims at trial. We believe Manulife has some potentially powerful arguments involving Canadian precedent for interpreting contracts – specifically looking beyond the plain language of the contract to the “factual matrix” and other factors – but on a plain language reading of the contract, we believe Mosten should prevail.

Summary of Key Contractual Terms and Summary of Mosten and Manulife’s Primary Arguments

Below, we have attempted to summarize the plain English terms of the Mosten-Manulife contract and each party’s key legal arguments. Investors should read the rest of this report and the publicly filed briefs and affidavits in their entirety. The following tables and this report itself are an attempt to summarize thousands of pages of material filed by Mosten and Manulife, and both these tables and this report itself are based on our views, which could be influenced by our short position in MFC. We are not Canadian lawyers, and nothing in this report should be construed as legal advice.

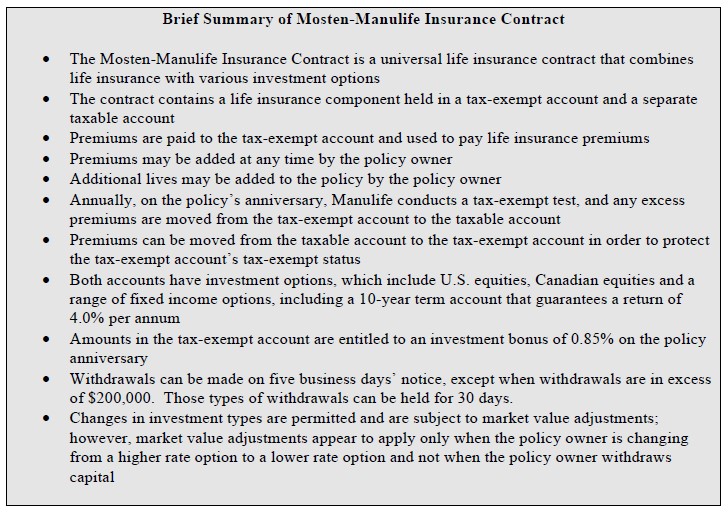

The following table is a brief summary of the Mosten-Manulife Insurance Contract:

Brief Summary of Mosten-Manulife Insurance Contract

Insurance contracts are particularly complex and contain multiple defined terms. The summary above is only an overview the material terms we believe are needed to understand the arguments made by Mosten and Manulife. It does not include all of the key terms of the contract.

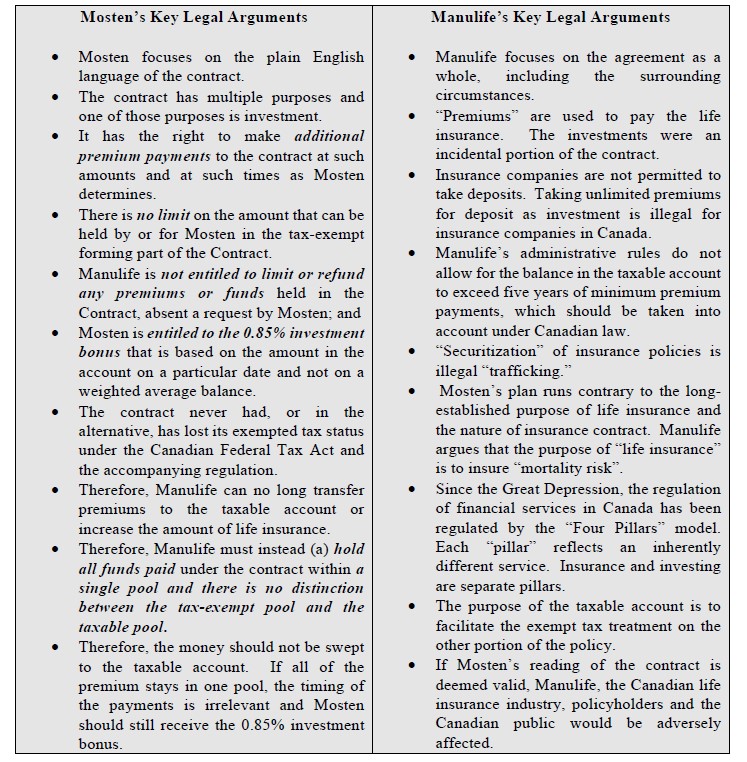

Below is a brief summary of Mosten’s and Manulife’s legal arguments:

We note that both Mosten and Manulife have other arguments set forth in their briefs and affidavits. The foregoing is just a brief summary of a much larger litigation. We include a more detailed summary of these later in this report. We encourage you to review the public filings made to the court and draw your own conclusions.

See the full report here by Muddy Waters